Moody’s Downgrades Kenya

Weaker demand for domestic government securities drives downgrade

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover Moody’s downgrade of Kenya, Safaricom’s third consecutive profit decline, and the persistent dollar issues in Kenya.First off, enjoy a dose of our weekly business news in memes:

Moody’s Downgrades Kenya

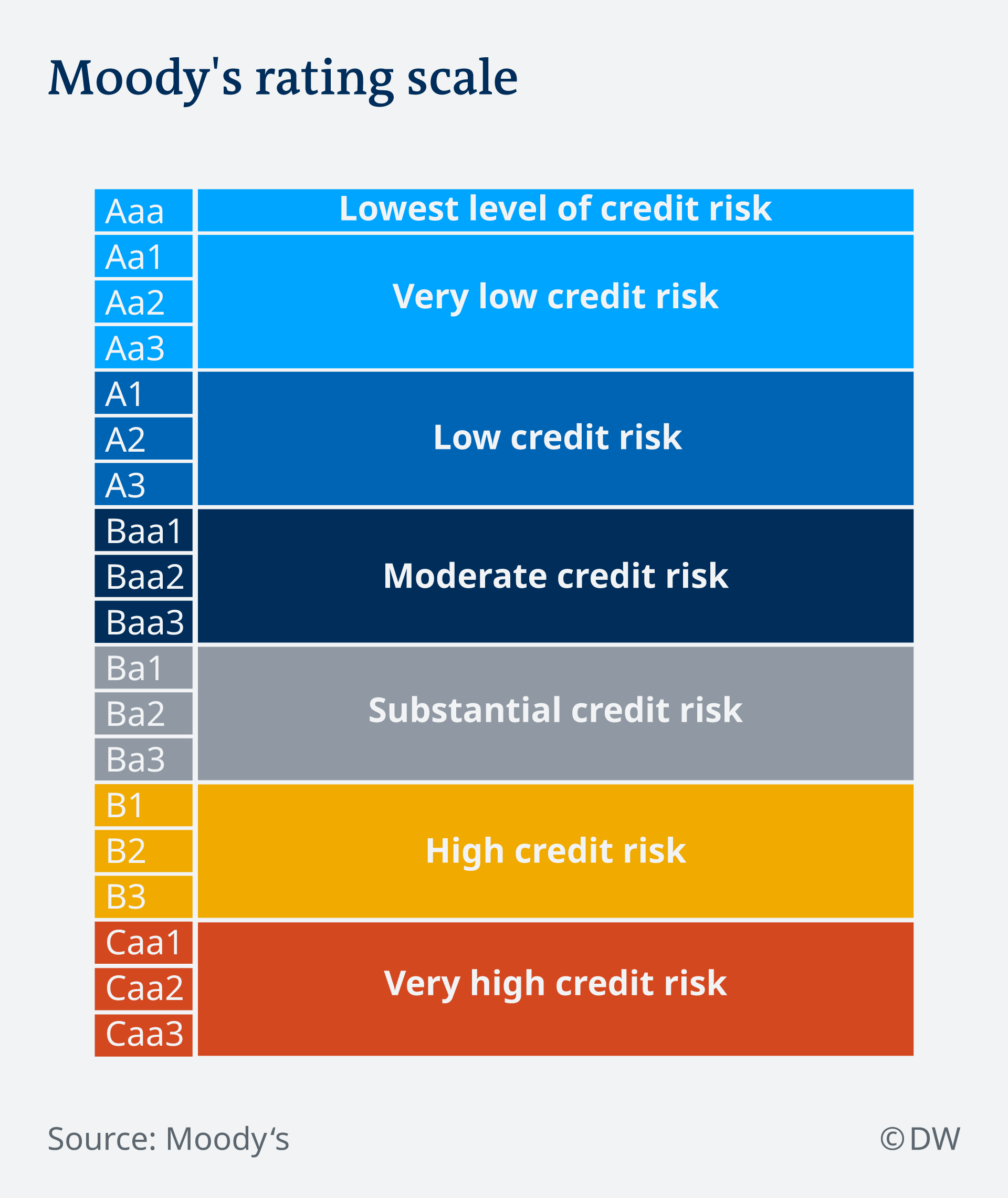

From B2 to B3: Global rating agency Moody’s Investors Service downgraded Kenya’s long-term foreign currency and local currency issuer ratings and senior unsecured debt ratings from B2 to B3. The downgrade is due to weaker demand for domestic government securities which has resulted in shortfalls in domestic financing amid significant external debt redemption in 2024. B3 is just one notch above the very high credit risk rating of Caa1. The ratings have also been placed on review for downgrade.

“The rating downgrade is driven by an increase in government liquidity risks. Domestic funding conditions have deteriorated considerably over the past two months, with very low net domestic issuance contributing to financing shortfalls and delays in government spending…The initiation of the review for downgrade is prompted by the risk that the deterioration in Kenya's domestic financing conditions persists amid still constrained external financing options.”

The Mwango Explainer: A credit rating refers to an assessment of a borrower’s creditworthiness in general terms or with respect to a particular debt or financial obligation. A credit rating can be assigned to any entity that seeks to borrow money - an individual, a corporation, a state or provincial authority, or a sovereign government.

Source: Moody’s

{kind=link}

Lacklustre Local Debt Markets: Investors have been seeking the safety of shorter-term debt and this is evident from the market data in the auctions in the year. Year-to-date, the average performance rate for the 91-day paper stands at 470.6%, while the 182-day and 364-day papers have rates of 72.7% and 39.8%, respectively. Kenya's decision to cancel the planned reopening of a 15-year government bond reflects the duration risk appetite investors have. As investors become more risk-averse, they are less willing to take on the potential volatility and uncertainty associated with longer-term investments. Data from Kenya’s National Treasury shows domestic borrowing receipts at KES 406.6B as of April 2023 against the FY 2022/2023 (ending July 2023) target of KES 886.5B.

“Government financing conditions in the domestic market have deteriorated significantly since early March 2023, with weaker demand for government securities resulting in shortfalls in net domestic financing. Demand for Treasury bills has shifted toward the shortest-maturity Treasury bills, the 91-day bill. Demand for longer-dated bonds has also weakened, with very low demand at recent auctions, including a planned re-opening of a 15-year government bond which was cancelled in April.“

External Debt Amortisation in Sharp Focus: In 2024, the gross external debt redemption stands at $3.5B, equivalent to 2.9% of GDP. Out of this, $2B is the KENINT 2024 eurobond maturity in June. Further down in the pipeline, there are Eurobond payments of $300M per year between 2025 and 2027 and a $1B principal maturity due in 2028, bringing into focus the scale of external financing requirements in the medium term.

“While external financing is anchored by an IMF program and strong support from multilateral development banks, it is also contingent on the government’s ability to deliver on fiscal consolidation. Without access to international bond markets, Moodys expects Kenya to rely primarily on concessional financing from multilateral financial institutions along with commercial syndicated loans and borrowing from regional development banks, to meet its external financing needs.”

Implications of the Downgrade: We asked two analysts for their perspectives on the Moody’s downgrade and the impact on Eurobonds. They agree that the focus should be more on the “review for downgrade” part:

“Eurobond yields continued trending lower, declining by an average of 59bps in the week. KENINT 2024 declined by 203bps in the week. Moody’s downgraded Kenya rating a notch lower to B3, potentially after trading hours. On a comparative basis, Moody’s rating puts it a notch lower compared to ‘B’ ratings of Fitch Ratings, and S&P. Investors will look beyond this latest downgrade action and focus on the ‘review for downgrade’ as we could see Kenya falling to triple C rating status. We think a CCC rating status will be a more ‘alarming’ threshold as passive bond investors may be forced to sell KENINTs as Kenya is dropped off benchmark indices. Although the Moody’s downgrade has flagged some risks, we think this is already priced in the market. Egypt was also placed by Moody’s for downgrade review earlier in the week, but the market reaction was not adverse. We think this will be the case with Kenyan Eurobonds next week, but the market will be on the lookout for triggers that could lead to a further downgrade.”

IC Asset Managers Economist, Churchill Ogutu

“It will be interesting to see the Eurobond market reaction to the Moody’s move, given the amount of negativity to Kenya already priced. The downgrade to B3 is likely to be widely expected, as the B2 rating has been on a negative outlook for close to three years. The ‘review for downgrade’ is more surprising given the strong fiscal consolidation achieved and the reasonable expectation that there will be sufficient multilateral support to get Kenya through its current funding squeeze. It could thus add to the negative market sentiment. Moody’s has historically been slower to move its rating than other rating agencies and was behind the curve, most notably by downgrading South Africa into junk territory in 2020, three years after Fitch and S&P. However, they have shifted to a more aggressively negative view of African credits in the past two years. While it was ahead of the other rating agencies in downgrading Ghana, the downgrade of Nigeria to Caa1 was harder to justify. My view remains that the continued fiscal consolidation and increased multilateral borrowing, potentially paired with some maturity reprofiling from China, will allow Kenya to get through the 2023/23 funding squeeze. My fears are primarily on the repercussions for frontier market financing conditions from defaults by Egypt and Pakistan in the coming year.”

REDD Intelligence Senior Analyst, Mark Bohlund

Where are the Dollars?

Where will the Kenya Shilling settle at? The shilling closed the week at KES 136.90, down 11% this year. The falling shilling, coupled with challenges in accessing dollars, has been causing investors to flee the Nairobi Securities Exchange. Absa Bank Kenya sees the shilling hitting KES 150 vs the USD by the end of the year.

“The trend will keep on for the rest of this year. This year, as much as inflation is expected to ease heading towards the statutory level, we forecast the shilling to continue weakening on the backdrop of steady interest rates which are already on post-Covid highs.''

Head of FICC Research and Chief Economist for Absa Bank Kenya, Jeff Gable

Dollar Repatriation Issues? The Safaricom Chairman, when responding to a question on the share price, gave an indication that there could be additional issues with dividend repatriation for foreign investors that relate to dollar availability.

“...there has been some difficulty in taking the dividends out, which then puts a little bit of pressure on some of the funds that are holding these shares.”

Safaricom Chairman, Adil Khawaja

Will Dollar Shortages Ease? According to the Energy CS, the USD KES rate should ease soon to below 130 from its current levels as a result of the Government-to-Government oil deal.

“With the stability and the symmetry on the interbank, we are likely to be converting these ones at 133-134. Progressively, we will possibly be seeing the dollar coming below 130. The pump prices today are more impacted not by the prices which have been coming down or going up, but more by the volatility of the shilling which went all the way to 147. So to the extent that the pump price is converted using the dollar price of the month, we will really remove that disadvantage by stabilising our shilling again vs the dollar by removing that pressure on the dollar due to what was happening.”

Energy CS, Davis Chirchir

Impact on Earnings: The forex issues are impacting earnings. Specifically, Airtel Africa noted this week that the depreciating Kenyan shilling had impacted its earnings.

“Net finance costs increased by $320m, largely due to higher foreign exchange and derivative losses of $245m. This increase mainly comprised a $67m loss on derivatives and higher foreign exchange losses arising from the revaluation of balance sheet liabilities (a loss of $82m on devaluation of the Nigerian naira, and other devaluation losses of $96m mainly arising from the Kenyan and Ugandan shilling, Malawian and Zambian kwacha).”

Source: Airtel Africa

Safaricom’s Profit Dips a Third Consecutive Time

Dip in Profits: Safaricom reported a 22% decline in its FY 23 net profit to KES 52.5B with the Ethiopia venture weighing heavily on aggregate earnings. Capital Expenditure (CapEx) has been ramped up as operations expand into more towns and the subscriber base grows. As of the end of FY 23, the Ethiopia subsidiary had 3M gross adds, with 2.1M 90-day active customers. Consolidated CapEx was KES 96.1B, up a whopping 93%. Margins have contracted as a result, and on a net basis, margins declined by 576 basis points (bps) to 16.9%.

Revenues Rise Steadily: Total revenues were up 4.3% year-on-year to KES 310.9B. Service revenues rose by 5.7% year-on-year to KES 297.2B, accounting for 95.6% of gross revenues [FY 22: 94.3%]. There was positive growth across all categories in service revenue, with Data revenue growing the most at 11.4% to KES 54B. Messaging revenue recorded positive growth for the first time since FY 18, expanding at 4.6% to KES 11.4B.

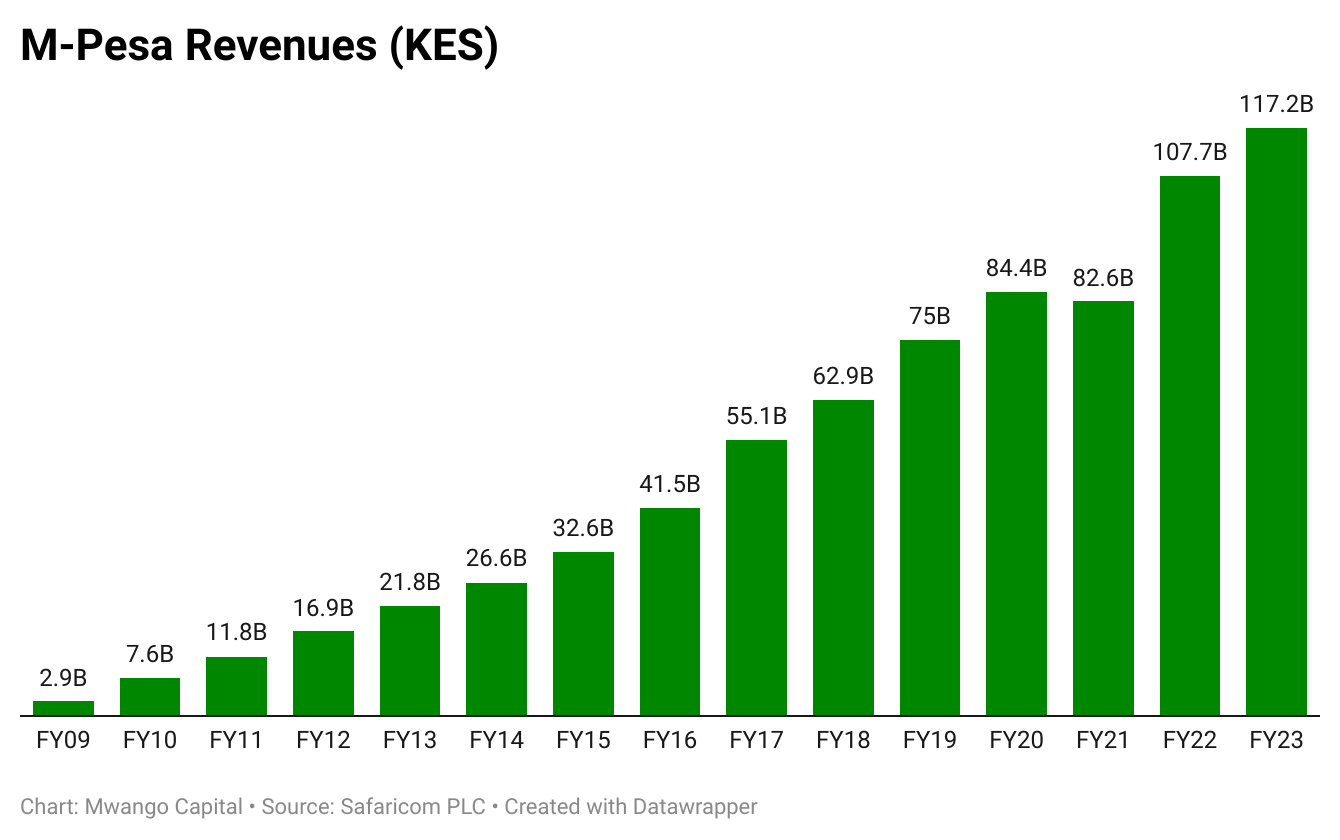

The M-Pesa Goldmine: M-PESA revenue grew by 8.8% to reach KES 117.2B, accounting for 39.7% and 37.7% of service revenue and total revenue, respectively, from 38.3% and 36.1% in FY 2022. Revenues generated from lending via Fuliza and KCB M-PESA declined by 8.3% while M-Shwari revenues expanded by 11.6% to KES 2.1B.

Update from Ethiopia: This week, the National Bank of Ethiopia issued a Mobile Money (MoMo) license to Safaricom Ethiopia to operate M-PESA in the country. Safaricom Ethiopia will be looking to launch mobile money services by the end of 2023, and at the AGM slated for 29th July 2023; Safaricom PLC will seek shareholder approval to create a subsidiary to house Ethiopia MoMo services. The license cost is $150M, out of which $83M/55.7% has been paid. Safaricom Ethiopia has made considerable progress in coverage, and as of the end of FY 23, 22% of the population had been covered across 22 out of 84 cities. Network sites totalled 1,272 [Self-built: 68.8% or 875, Collocated: 31.2% or 397].

This week, Orange Middle East and Africa CEO, Jerome Henique, was in Ethiopia and met with Ethiopia’s State Minister of Finance, Eyob Tekalign. Henique expressed Orange's interest in the Ethiopian market and the region. A move into Ethiopia will create significant competition for Safaricom Ethiopia at a time when it is ramping up operations there.

Looking to Raise: Safaricom is in the market to raise ~$150M in debt to refinance loans and fund infrastructure projects in Kenya and Ethiopia. Standard Chartered is among the advisors for the financing.

“This is now the final stage where we are because from their side they have gone through their investment committee approval, they have gone through their board approval but now we have to do our part to make sure that few issues are sorted out. IFC coming in, all the Consortium members will dilute yeah in terms of our Equity investment but you will still continue to hold the majority shareholding. On the debt side, they are coming in and then they’re just our capital structure. So them coming, actually yes they do dilute, but it doesn’t to a point that you lose our majority.”

Safaricom PLC CFO, Dilip Pal

Share Price Reaction: Safaricom‘s share price closed the week at KES 13.25, down 16% this week only. The company is down 68% from its peak in August 2021. This decline (drawdown from peak) is the worst since the company was listed in 2008.

Here are links to the results presentation and the booklet.

Telco Updates Around Africa

Vodacom Tanzania Rebounds to Profit: In FY 2023, Vodacom Tanzania recorded a TSHS 44.6B/$19.2M profit up from a TSHS 20.3B/$8.7M loss recorded in FY 22. Service revenue increased by 10.2% year-on-year to reach TSHS 1.05T/$453.6M, buoyed by 34.2% growth in mobile data revenue - the fastest segment-wise. Gross revenues expanded by 10.5% to TSHS 1.07T/$461.9M. Operationally, Vodacom Tanzania secured low and mid-band spectrum for an aggregate acquisition price of TSHS 143.1B/$63.2M payable in 18 months. Regarding, market coverage, the customer base reached 1.4M while the market share stood at 30%.

Airtel Africa: For the fiscal year ended 31st March 2023, gross revenue was up 18.6% year-on-year to $5.2B, surpassing the $5B mark. MoMo was the growth driver in the period, increasing by 28.9% to reach $692M, while the bulk of revenues were from Voice at $2.5B, an increase of 9.4%. While Nigeria’s contribution to total revenues was 40%, the largest across Africa Markets on an aggregate basis; the striking point was East Africa’s contribution to aggregate MoMo revenue, which stood at 76.7%. There was a recognition of a deferred tax credit of $117M in Kenya, $25M in the DRC and $19M in Tanzania; bringing total tax charges down by $185M. Net profit for the year fell by 60 bps to $750M, resulting in a net margin of 14.3% [2022: 16%].

Source: Airtel Africa

MTN Africa Disposals: MTN Group, the largest mobile operator in Africa, is in advanced discussions to sell some of its assets to Axian Group, a pan-African group based in Madagascar, as it looks to simplify its portfolio and concentrate on core markets such as Nigeria and Ghana. The potential sale of MTN's assets in Liberia, Guinea-Bissau, and Guinea-Conakry is in line with what telecom companies across the region are doing in assessing their portfolios in light of challenging business conditions. Good to note that Axian bought Millicom International Cellular’s Tanzanian operations last year.

MTN Rwanda Q1 2023: Service revenue increased by 14.9% to reach Rwf. 58.4B, and on a gross level, revenues rose by 14.8% to RWf 59.4B. While EBITDA increased by 9.4%, the EBITDA margin edged lower to 45.5% [2022: 47.7%]. Market share grew the fastest across Momo subscriptions at 17.2% compared to Mobile subscriptions (7%) and data subscriptions (-0.7%). In the current fiscal year, MTN Rwanda is set to separate its MoMo functions and warehouse them in Mobile Money Rwanda Limited, and the operational focus for Q2 2023 is the launch of 4G country-wide. The net result from operations was down 32% to RWf 2.8B.

Earnings Wrap

Sasini HY 2023 Results: For the 6 months ended March 2023, gross revenue fell by 33.4% year-on-year to reach KES 2.3B. Total Operating Income edged higher by 38.5% to KES 724M, while net profit fell by 71% to KES 122.1M. In the operating period, Sasini lost half of its tea production and some units of avocado and coffee production were impacted as a result of drought.

“Considering our cash position and reserves, the ongoing difficulties with the high cost of living, the Directors recommend the payment of an interim dividend of 100% (KES 1.00) per share, for the year ending 30th September 2023.”

Stanbic Bank Kenya Q1 2023: Customer deposits increased by 24% to reach KES 291B while the loan book expanded by 12% to KES 230B, bringing the loan-to-deposit ratio to 79%. Total revenue increased by 65% to reach KES 11B while the profit for the period grew by a whopping 84% to close at KES 3.9B (35.5% of total revenue).

“Our accelerated efforts in implementing our strategy, driving operational efficiencies, and managing costs have seen us progressively manage our cost-to-income ratio downwards to stand at 40.5% compared to 49.6% in the prior period. As a result, Return on equity in the period under review improved to 21.7% from 17.6% reported in the same period last year.”

Stanbic Bank Kenya CFO, Dennis Musau

Markets Wrap

The NSE: In Week 19 of 2023, BOC Kenya was the top-performing stock on the Nairobi Securities Exchange, appreciating by 11.8% to KES 90.25, while Safaricom was the worst-performing stock, falling 15.9% to KES 13.25. The NSE 20 and NSE 25 indices fell by 4.1% and 8% to 1,472.2 and 2,504.8 points, respectively while the NSE All Share Index was (NASI) down by 9.2% to 93.6 points. Equity turnover was up 57.9% to KES 1.4B while bonds turnover rose by 0.3% to KES 13.9B. Notably, NASI fell below 100 points in the week.

T-Bills: In the short-term public debt markets, the weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day treasury bills were 10.41%, 10.853%, and 11.270% respectively. The total amount on offer was KES 24B with the CBK accepting KES 45.3B of the KES 45.3B bids received, to bring the aggregate performance rate to 188.91%. The 91-day and 364-day instruments recorded 865.75% and 18.64% performance rates, respectively.

T-bonds: In the 3-year Treasury Bond FXD1/2023/003 with KES 20B on offer, CBK accepted KES 20.3B of the KES 20.7B bids submitted, settling a coupon rate of 14.228%. KES 8.2B (40.6%) of the accepted bids is slated for redemptions with the remainder being new borrowing.

Market Gleanings

💼 | Funding Secured | The East African Crude Oil Pipeline project has been looking for ~$1.8 billion in debt financing for the project and they have found it from some Chinese lenders and 2 undisclosed African banks. TotalEnergies has a 62% stake in the project, Uganda National Oil Company and Tanzania Petroleum Development Corporation own 15% each, while the China National Offshore Oil Corporation owns 8%. The project has a 60-40 debt-equity financing mix.

🛑 | Debarred | African Development Bank (AfDB) has debarred a Kenyan company, Goldsun Investments Company, from participating in its infrastructure tenders for 24 months starting January 31st, 2023. This is because the firm engaged in” fraudulent practices during a tender for the dualling of the 84 km Kenol-Sagana-Marua highway.”

“At the expiration of the debarment period, Goldsun Investments Company Ltd. will only be eligible to resume participation in African Development Bank Group-financed operations and activities after it implements an integrity compliance program consistent with the Bank’s guidelines.”

⚙️ | LNG from Tanzania | Latest estimates from Tanzania's Liquefied Natural Gas (LNG) project show that the project costs have risen to $42B, up from $30B, making it the largest energy project in Eastern and Southern Africa. The project's aim is to develop the country's 57.54 trillion cubic feet of discovered gas by 2028 with Uganda and Kenya already having signed agreements to buy Tanzania's LNG. Shell and Equinor are the lead partners with participating interests from the Tanzania Petroleum Development Corporation [Business Insider + The East African].

Charts of the Week