Proposed Eurobond Buyback

Kenya is currently weighing a partial buyback of the USD 2B KENINT 2024 Eurobond

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a summary of key capital markets and business news items from East Africa.This week, we cover the proposed partial buyback of the KENINT 2024 Eurobond, Kenya’s inflation in January 2024, and Ndindi Nyoro’s reduced stake in Kenya Power.This week's newsletter is brought to you by:

Co-operative Bank of Kenya. Get ready for the YEA account movie magic giveaway by opening a YEA account.

Proposed Eurobond Buyback

Partial Debt Buyback: After failing to buy back part of the Eurobond by the end of December 2023 as earlier indicated, Kenya is currently weighing a partial buyback of the USD 2B KENINT 2024 Eurobond in February or March this year. This could be followed by a return to the international capital markets to refinance the debt, and according to President William Ruto, a general expectation of securing favorable pricing.

“There are several options that are available to us, but the positive thing about all the options is that the market is now open for Kenya and that is very positive news. It means we can repay the whole bond from resources from the market and therefore it’s a very positive development. We are looking at a buyback of some amount. We are yet to determine what that buyback amount is and then the rest of it, we will pick it up from the market.”

“What they have recommended is we do a buyback in February, March, and then we go to the market. Because of the situation that we now see in the market, we believe that it would be a lot easier even for us to raise that money in the market, rather than through syndication.”

President of Kenya, William Ruto

Context: Kenya has been exploring ways of repaying the KENINT 2024 Eurobond, considering the prevailing macroeconomic environment that has largely been characterised by elevated interest rates. This has challenged refinancing efforts. However, Kenya seems to have seen a path to raising capital in the international markets, and the plans around the partial debt buyback and debt issuance are against the backdrop of the recent sovereign bond issuances by Côte d'Ivoire, whose yields came in at single-digit rates - 7.875% for the USD 1.1B 2033 paper and 8.5% for the USD 1.5B 2037 paper. The Côte d'Ivoire issuances pulled an aggregate outcome that was 3X oversubscription, indicating the high level of investor interest in the instruments. Investors are, however, likely to demand a higher premium were the country to float dollar-denominated debt, given Kenya's set of financial and economic conditions.

Here is what IC Asset Managers Economist Churchill Ogutu had to say on the prospect of buyback and refinancing:

“A buyback and/or refinancing will entirely be dependent on market conditions, and it is not cast in stone that GoK will exercise that option as the President may want the market to believe. In fact, I think the whole rhetoric around the timing of a potential buyback and/or refinancing only fuels uncertainty in investors' minds and puts the transaction advisors in an awkward decision. Granted, the Sovereign is allowed to buy up to USD 200M (10.0% of the outstanding USD 2B) but as we near the maturity date and on receding default fears, investors are holding on to the paper. With KENINT 2024 trading at 97.4c to the US Dollar, this essentially means that GoK would have to pay at least par (USD 1) or slightly more for every USD 1 face value to entice the investors to the buyback. Otherwise, repaying the amount upon maturity is the path of least resistance, as opposed to conducting a buyback.”

“It goes without saying that with KENINT 2024 yields at c. 14.0%, it may be difficult to access the market at least this 1H 2024, more so on the back of Friday's hot US labour report that pushes the start of the global rate easing cycle. To reiterate, markets will demand yields above 10.0% when Kenya taps the international bond market in the near future and we hope that the authorities may not be side blinded by the recent success of IVYCST whose bonds have been trading at sub 10.0% levels even before returning to the international market last month. Unless GoK dangles a sovereign/green bond, a refinancing is off the table, in my view. Let's make it clear, unlike the KENINT 2019 (USD 750M June 2019 maturity) which was refinanced by the dual-tranches of KENINT 2027 (USD 900M May 2027) and KENINT 2032 (USD 1.2B May 2032), a plain vanilla Eurobond refinancing may not be feasible. We thus think the authorities will make do with the increased IFIs flows to refinance the USD 2B KENINT 2024.”

IC Asset Managers Economist, Churchill Ogutu

Forex Reserves: The government has been sourcing external funding in what is part of its reserve build-up in the run up to the KENINT 2024 maturity. So far, the IMF and the Trade Development Bank have extended some facilities to Kenya, with more foreign flows expected. As of last week, the stock of foreign exchange reserves edged higher for the second consecutive time to reach USD 7.1B, a level last recorded in September 2023.

Inflation Edges Higher

Jan Inflation Up 30 bps: In January 2024, inflation rose by 30 basis points month-on-month and 210 bps year-on-year to reach 6.9%. Across indices, transport rose the most year-on-year, up by double digits at 10.6%, followed by the Housing, Water, Electricity, Gas and Other Fuels index which surged by 9.7%. The Insurance and Financial Services index recorded the least change relative to January 2023 at 1.0%.

KBA Issues Guidance: Ahead of the Central Bank of Kenya’s Monetary Policy Committee (MPC) meeting slated for Tuesday, 6th February 2024; the Kenya Bankers Association (KBA) has called for the MPC to keep the Central Bank Rate (CBR) unchanged, citing easing inflationary pressure, softening economic performance outlook, ongoing transmission of the 200 bps hike in December 2023, asset quality concerns in the banking sector, and expected easing in the USDKES exchange rate in the foregoing.

“In view of the above developments and a balance of risks on inflation and the direction of the exchange rate; we argue for a maintenance of the current stance of monetary policy - in keeping the CBR unchanged; allowing the 200 basis points upward adjustment effected in December 2023 to be fully transmitted in the market and protect the fragile economic activity.”

Upcoming MPC: The MPC is happening against the backdrop of a +30 bps increase in inflation, a 2.8% depreciation of the USD/KES rate year-to-date, and rising rates across the board. In its December 2023 decision, the MPC hiked the CBR by 200 bps but there is growing consensus that the MPC will still hike in its meeting this week to double down on its tightening stance. Here is what various economists and analysts have to say on this:

“While the CBK surprised markets with a 200 bps hike in December, it may want to reinforce the message that it is prepared to maintain tight policy to support the KES. We now expect February to be the last hike of the cycle. We now see the policy rate at 14.5% at end-Q1-2024 (12.5% previously), 14% at end-Q2 (12.5% prior), and 13% at end-Q3 (12.5%). Our year-end forecast remains 12.5%.”

Standard Chartered Head of Research, Africa and Middle East, Razia Khan

“My sense is a retention. One, inflation is still within range, and two, the currency is fluctuating as opposed to before when it was depreciating steadily. A hike is unlikely but not impossible. I am assuming it should be a balance between anchoring inflation and stimulating economic growth though private sector credit growth remains resilient. A cut is highly unlikely given that inflation rose despite being within range and cutting will mean more dollar outflows. So a retention to allow the jumbo hike to transmit within the economy.”

Standard Investment Bank Research Analyst, Stellar Swakei

“I foresee a HOLD decision in the upcoming CBK MPC meeting. The latest inflation print although bucking the disinflation trend that played out in 4Q 2023, cyclical aspects were built on the print which may fade off with upcoming inflation prints, in my view. Furthermore, I think the policymakers may let the previous rate tightenings, the 200 bps rate hike in the December 2023 MPC meeting, filter through the economy with the necessary lags. I also believe that the CBK will speak on the recent KES performance, last week showing green shoots of reversing the depreciation trend that has been entrenched since 2023.”

IC Asset Managers Economist, Churchill Ogutu

Find the inflation press release here and the research note by KBA here.

Markets Wrap

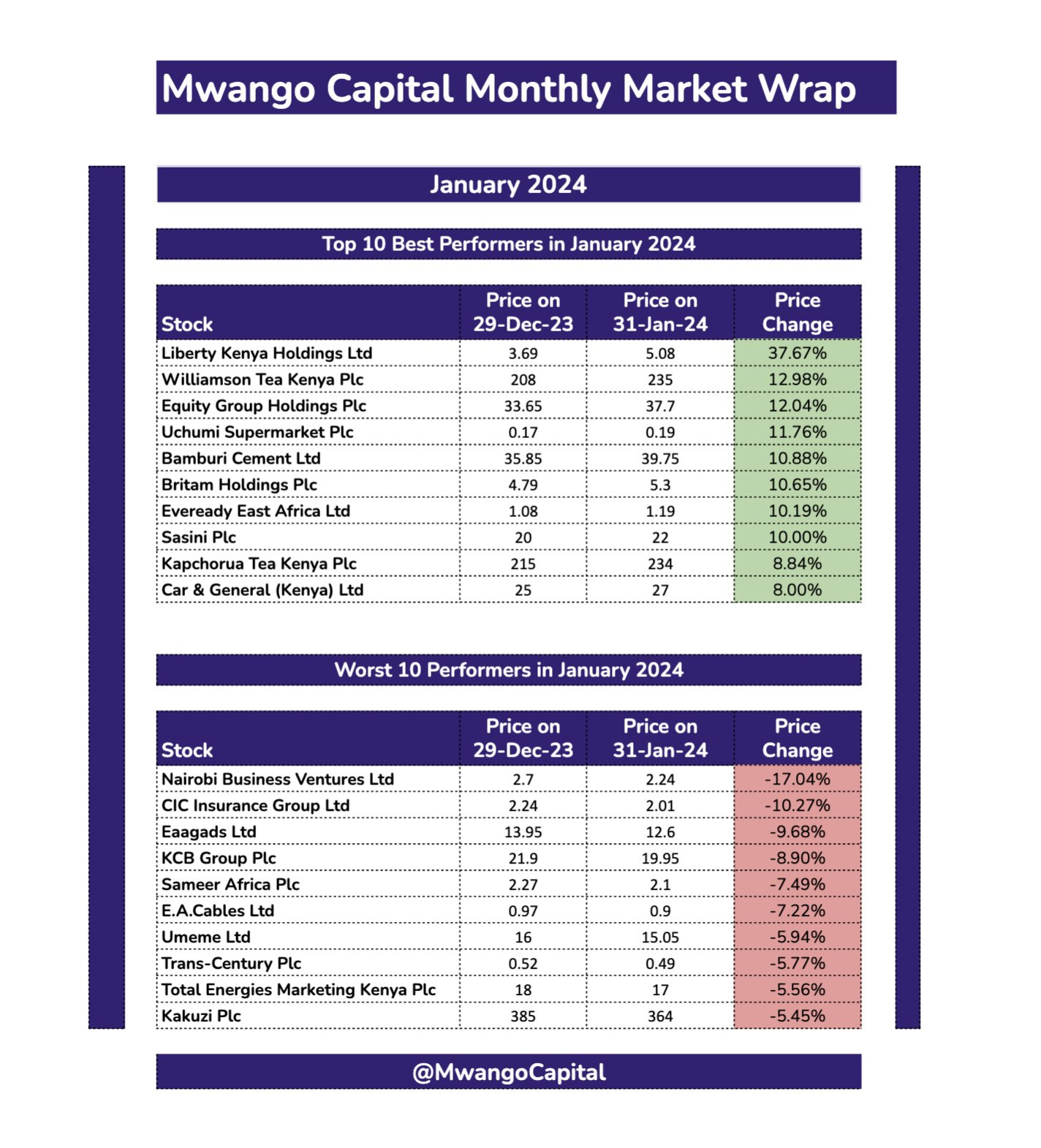

NSE: In Week 5 of 2024, Uchumi was the top-performing stock, up 11.1% to close at KES 0.20. Sanlam was the worst-performing stock, down 9.7% to close at KES 6.34. The NSE 20 gained 1.0% to close at 1,512.6 points, the NSE 25 rose by 1.6% to close at 2,409.3, and the NASI index edged higher by 2.0% to close at 92.2 points. Equity turnover rose by 53.2% to KES 839.45M from KES 547.99M the prior week while bond turnover closed the week at KES 22.7B compared to the prior week’s KES 18.6B. In January 2024, Liberty Kenya Holdings Ltd was the top performer at the NSE with a 37.7% gain to KES 5.08, while Nairobi Business Ventures Ltd was the worst performer, down 17% to KES 2.24.

Treasury Bills: The weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day were 16.3747%, 16.5058%, and 16.6801% respectively. The total amount on offer was KES 24B with the CBK accepting KES 24.7B of the KES 25.8B bids received, to bring the aggregate performance rate to 107.50%. The 91-day and 364-day instruments recorded 515.7% and 35.09% performance rates, respectively.

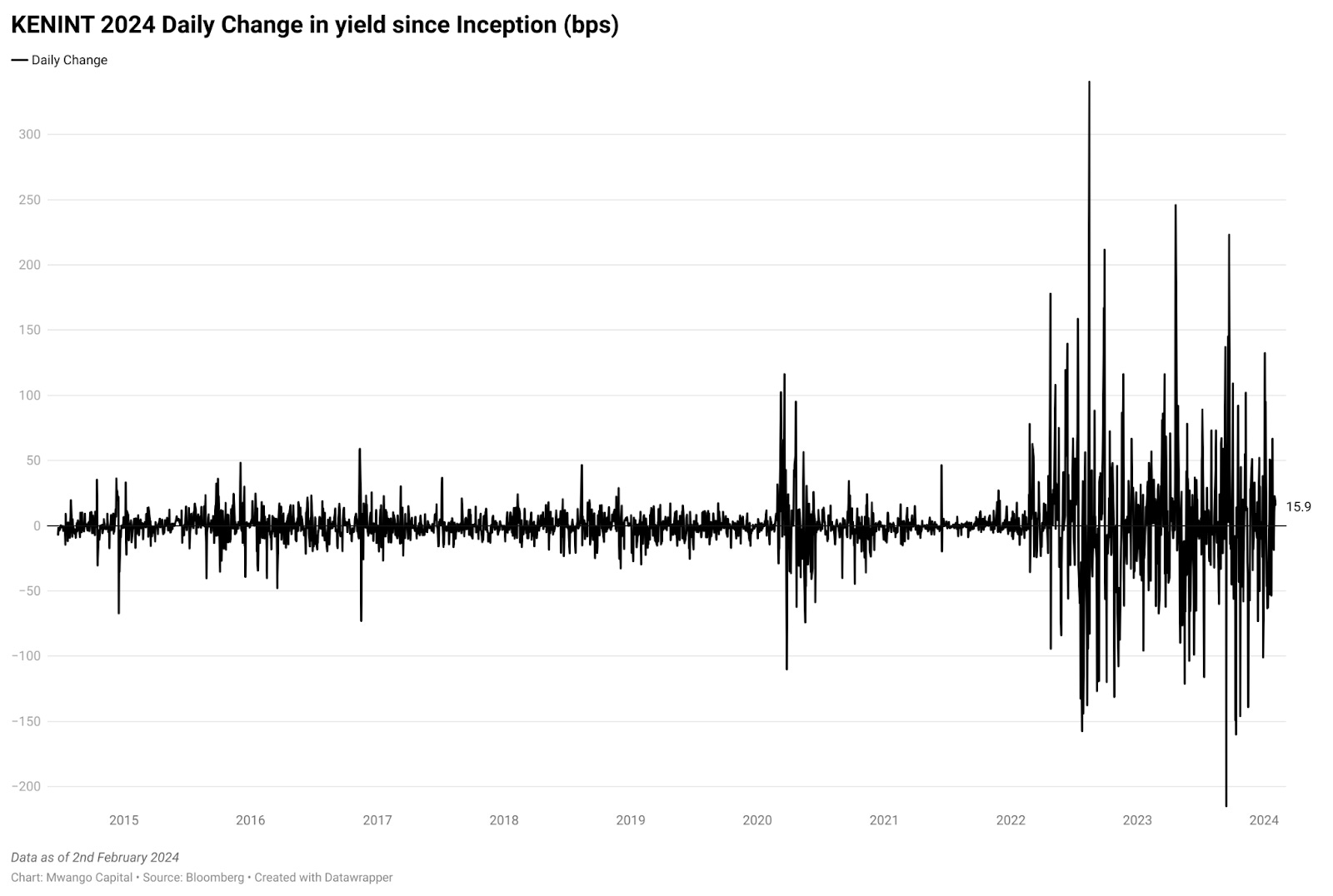

Eurobonds: In the week, yields rose across the 6 outstanding papers.

KENINT 2024 rose the most week-on-week, up by 50.30 bps to 13.978% while KENINT 2027 rose the least, depreciating by 11.50 basis points to 9.906%. The average week-on-week change stood at 27.47 bps.

KENINT 2024 rose the most on a year-to-date (YTD) basis, appreciating by 144.80 bps while KENINT 2048 rose the least at 53.10 bps.

Prices fell across the board week-on-week, with KENINT 2048 falling the most at 1.9% to 79.255. Year-to-date, KENINT 2048 fell the most, depreciating by 4.7% to 79.255, while KENINT 2024 fell by 0.1% to 97.375.

Markets Gleanings

🪓| Nyoro Cuts Kenya Power Stake | Kiharu Member of Parliament and Budget and Appropriations Committee Chairman Ndindi Nyoro has reduced his stake in Kenya Power by 36% in the period between June and December 2023. The offloaded stake totals about 11.78M shares, bringing his shareholding to 20.72M shares. In the year to June 2022, Nyoro had tripled his shareholding to 27.3M shares from 9.1M shares in June 2021.

🏭 | Maiden SEZ in Western Kenya | The Cabinet Secretary for Investments, Trade and Industry - Rebecca Miano, last week launched the Riwa Special Economic Zone - the first Special Economic Zone (SEZ) in Western Kenya. Riwa SEZ is located at West Karachuonyo and spans 532 acres.

🧾 | Pending Bills Verification | Last week, the National Treasury held a media briefing and issued an update on the resolution of government pending bills spanning from 2005 to 30th June 2022. As of 30th January 2024, the Pending Bills Verification Committee had received 1,537 claims from 38 Ministries, Departments, and Agencies (MDAs) amounting to KES 145.5B. 309 claims relate to goods, 945 to services, 1,195 to works, and 2 to labour.

🏦 | Tanzanian Banks Results |

NMB: NMB Bank Tanzania reported their Full Year 2023 results last week. The bank’s total assets grew by 5.5% to TZS 12.2T. Net interest income surged by 35.7% to TZS 938.9B. Customer deposits rose modestly by 1.9% to TZS 8.2T, while loans increased significantly by 10.1% to TZS 7.7T. Both operating income and net income grew by 36.2%, reaching TZS 774.7B and TZS 542.5B respectively.

NCBA Bank Tanzania: NCBA Bank Tanzania’s 2023 financial results revealed a slight quarter-on-quarter increase in loans by 0.4% to TZS 276.9B, while government securities dipped by 0.6% to TZS 85B. Deposits decreased by 3.4% to settle at TZS 261.7B with the total assets growing by 0.3% to TZS 515.2B. Net interest income increased by 29% to TZS 39.1B while profit after tax stood at TZS 19.7B from a loss of TZS 35B reported in 2022.

CRDB: CRDB Bank’s quarterly balance sheet shows a 4.1% increase in loans to TZS 8.5T, while gov’t securities decreased by 1.5% to TZS 2.2T. Deposits grew by 2.4% to TZS 8.7T and the total assets increased by 4% to TZS 13.2T. The company had a 19% increase in net interest income to TZS 846B, a 10.7% rise in non-interest income to TZS 448B, and a 21% growth in profit after tax to TZS 424B.

📉 | Naira Depreciation | Nigeria’s naira experienced a record depreciation against the dollar, following a change in the exchange rate methodology and allegations of rate manipulation by traders. The currency fell by 31% to 1,413 naira per dollar in the official foreign exchange window, marking the second devaluation in seven months. This shift brings the naira closer to its parallel market rate of 1,468.

📡 | Airtel Africa Q3 2024 Results | In its Q3 2024 results, its customer base expanded by 9.1% to reach 151.2 million, with data customers surging by 22.4% to 62.7 million and mobile money users rising by 19.5% to 37.5 million. Revenue recorded a 20.2% increase in constant currency. However, foreign exchange headwinds impacted overall profitability, resulting in a USD 2M net profit. The company is set to launch a USD 100M share buy-back in March 2024.

🗺️ | World Economic Outlook Update | The IMF estimates that the Sub-Saharan African economy grew by an estimated 3.3% year-on-year in 2023, and is projected to grow by 3.8% in 2024 and 4.1% in 2025. The latest projections are revised from October 2023 - including a downgrade of 2024 by 0.2% and an unchanged outlook for 2025. You can find the entire document here.

Charts of the Week