World Bank Lends A Hand

The World Bank approves a $1B Development Policy Operations (DPO) loan

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover the World Bank’s $1B DPO Loan and more Q1 2023 Kenyan banks' earnings.First off, enjoy a dose of our weekly business news in memes.

World Bank Lends A Hand

The Deal: The World Bank has approved a $1B (KES 138B) Development Policy Operations (DPO) loan for Kenya:

“The government’s reforms, supported by the DPO, will help to achieve fiscal consolidation, which is essential for reducing the debt burden and related risks, in an equitable and sustainable manner by safeguarding social spending while supporting much-needed revenue and expenditure measures”

World Bank Senior Country Economist for Kenya, Aghassi Mkrtchyan

The Sources: 50% of the loan comes from the World Bank’s International Development Association (IDA) while the other 50% comes from the International Bank for Reconstruction & Development (IBRD). The IBRD loan comes with a variable interest rate set at 85.0 basis points above the Secured Overnight Financing Rate (currently at 5%).

The Impact: The yield on Kenya's 2024 Eurobond fell 124 basis points to 15.19%, the biggest decrease since November. Here is what two analysts had to say about this lending:

“This is positive as i) it will reduce the dollar scarcity in the economy that should hopefully lead to further normalization of the interbank FX market, ii) enable the government to meet its budgetary borrowing requirement for the fiscal year, iii) reduce local borrowing requirements and thus reduce the pressure on interest rates, iv) reduce the risk of default on the maturing 2024 Eurobonds, and v) improve the country's FX buffers, which may allow it to tap external markets for further funding.”

Financial Analyst, Ronak Gashia

“The DPO loan disbursement was expected. Nonetheless, the drop in Eurobond yields indicates that it has allayed some of the concern about Kenya’s ability to refinance its upcoming debt maturities. These include a principal payment of around USD 300m to China Exim Bank due in July. With multilateral financing sources tapped out in the near term, President Ruto is likely to focus on some form of debt relief from China in FY 23/24.”

REDD Intelligence Senior Analyst, Mark Bohlund

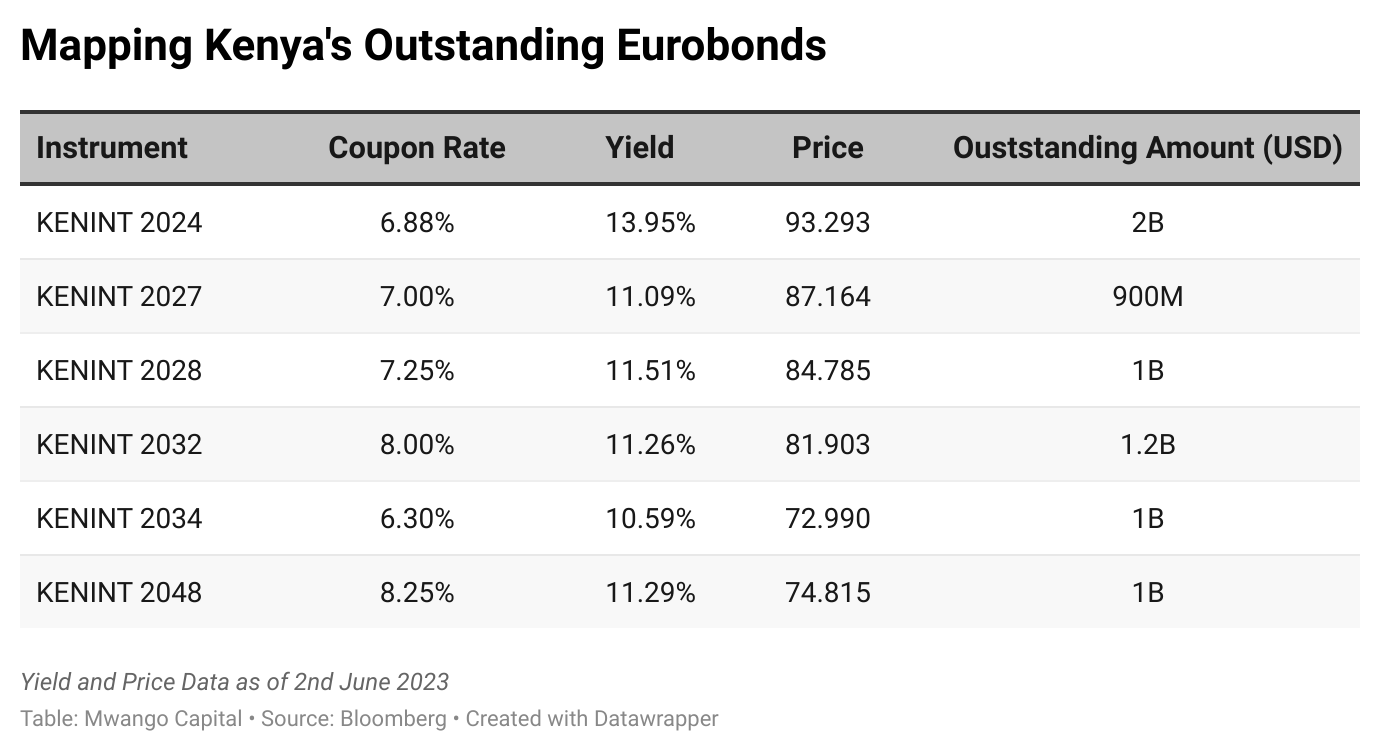

Dealing with the Eurobond: Meanwhile, the government’s plan on how to deal with the $2B Eurobond that is maturing next year on 24th June 2024 includes the issuance of a new Eurobond as an option. Business Daily is reporting that the final shortlist for the planned arrangers for the new Eurobond that Kenya wants to issue are Citigroup, JPMorgan Chase, Standard Bank, and Standard Chartered Bank. Here are the options that the government has in full:

“To settle this Eurobond at maturity at minimum costs at risk, the government is considering several options. These options include liability management operations, using alternative financing solutions to settle maturities, undertaking buybacks, which means a tender offer through open market operations or a bond switch exchange with the current bond with different longer tenure bonds in consultation with sovereign rating agencies, and we also shall consider bilateral and multilateral concessional funding to buy back. The National Treasury is at an advanced stage of procuring lead managers to provide advisory services in the next few weeks.”

National Treasury Permanent Secretary, Chris Kiptoo

Dollar-Denominated Bond? The CBK Governor nominee, Dr. Kamau Thugge, has proposed working with the treasury in issuing a dollar-denominated local bond in the same way they issue an infrastructure bond in order to tap into the close to KES 1 trillion in dollars held by Kenyans in local banks. The outgoing CBK governor, Dr. Patrick Njoroge, strongly disagreed with this proposition:

“If you can get those Kenyans who are holding the dollars in the deposits to buy into it, cause I'm sure the government can offer a better rate, that will have the possibility of actually increasing the liquidity of dollars in the system, but also building up the foreign exchange in the central bank because ultimately, once the national treasury gets those dollars, they will sell them to the Central bank and get the shilling equivalent.”

CBK Governor Nominee, Dr. Kamau Thugge

“What would [it] accomplish?... It wouldn't get any more [new dollars]...It wouldn't mop up those excess [local] dollars because there are no excess dollars..."

Outgoing CBK Governor, Dr. Patrick Njoroge

Kenyan Banks Q1 2023 Results

I&M Group, Diamond Trust Bank Kenya, HF Group, and Absa Bank Kenya concluded Kenya’s banking sector Q1 2023 results this week. Below are our key takeaways:

Loan Book: KCB Group had the largest loan book in absolute terms at KES 928.8B, up 31.9% year-on-year. This was the largest change across the largest listed lenders that have reported so far. StanChart recorded the lowest lending in the operating period in absolute terms at KES 137.1B, down from 37.6% in 2022. Notably, Absa Bank Kenya’s lending grew by 27.7% to KES 309.9B, against a deposit base of KES 310.8B, bringing the loan-to-deposit ratio to 99.7% [2022: 90%].

Government Securities: The trend in Q1 2023 has been a downsizing in investment in government securities and a pivot towards lending. I&M Group cut its pile by 13.3%, the largest margin across all banks, to KES 72.7B, to represent 15.4% of the balance sheet [2022: 19.5%]. Across the banks, the average growth in investment in government securities stood at -0.4%, while the average change in lending growth was 18.5%, underscoring the scale of capital allocation during the operating period.

Asset Base: KCB Group’s balance sheet which grew the fastest across all banks at 39.7% to reach KES 1.1T, the largest by size in East Africa. Equity’s gross asset base grew by 21.12% to reach KES 1.5T, taking into account the completion of the Spire Bank acquisition. NCBA Group’s asset base grew the least across all banks, expanding by 7% to reach KES 628.8B.

Interest Income: At KES 24.6B, KCB Group recorded the largest amount of interest income from lending, representing 31.4% growth from 2022. Equity’s interest income was up 21% to KES 20.7B while Cooperative Bank of Kenya’s was up 11.64% to KES 10B.

From government securities holdings, Equity accrued the largest amount of interest income at KES 10.6B, followed by KCB at KES 8.7B, and NCBA at KES 6.6B, to represent a growth of 14.4%, 14.6%, and 14.8%, respectively. DTB and Stanbic registered the largest increases in interest income from government securities at 29.8% and 28.1%, respectively.

FX Trading Income: With challenges around accessing US dollars in the country, banks reported a whopping average growth of 97.7% in FX Trading Income. Equity reported the largest increase at 152.3% to KES 5.2B, followed by Stanbic at 147.7% to KES 4.3B. While Co-operative Bank reported the lowest change at 43.9% to KES 1.1B, the income from Forex Trading accounted for 15.5% of Non-Funded Income, up from 11.9% in 2022.

Loan Loss Provisions: KCB reported the largest amount of loan loss provisions through the income statement at KES 4.1B, up 98.4% - to represent 17.9% of gross operating expenses,[2022: 13.8%]. I&M recorded the highest change from 2022, with the provisions edging higher by 241.5% to reach KES 1.6B, increasing its share of gross operating expenses in the period by 2.2X when compared to 2022. StanChart registered the least size of provisions at KES 790.9M, but a significant change from 2022 where the provisions stood at KES -86M in 2022. Excluding KCB and StanChart; DTB, Stanbic, Absa and Equity registered significant growth in provisions, increasing them by 134.7%, 132.9%, 103.3% and 92.5% to KES 1.3B, 1.1B, KES 2.4B and KES 3.4B, respectively.

Profitability: The highlight in profitability growth was Stanbic, which witnessed its net income grow by a whopping 84.3% to reach KES 3.9B. Absa, NCBA and StanChart recorded impressive growth in Net Income, expanding by 50.7%, 48.5% and 45.7% to KES 4.4B, KES 5B and KES 4B, respectively. Equity was the most profitable, recording a net result of KES 12.8B in the operating period, an increase of 7.9%. Banks which reported a drop in their net profit position include KCB Group and I&M, falling by 1.5% and 2% to KES 9.7B and KES 2.6B, respectively.

This week on #MwangoSpaces, we hosted Sunil Sanger, Managing Director at Orion Advisory Services, for a discussion on Kenya’s banking sector Q1 2023 results. Below are key quotes from the discussion:

On Holdings of Government Securities by Kenyan Banks:

“I think firstly, banks' portfolios are very heavy in government securities, and with the way the interest rates have moved, all of them are carrying large losses on their books. Some of it is there in the Other Comprehensive Income, on the Available For Sale portfolios, and some of it is in the Hold To Maturity portfolios which of course are carried at cost but if they were to be marked to market there would be a very significant loss. There was nobody who had an aggressive increase in their government securities book or in lending to the government, possibly I think the only exception was I&M which was at a 14% increase. Everybody else was in single-digit increase and three of the banks were actually negative.”

On the High Interest Expenses:

“So I think traditionally banks in Kenya obviously have got very high interest spreads. I guess for a change usually, when the rates move up, when there is a movement in interest rates, banks are normally able to widen their interest margins and this time there seems to be a bit of a lag in widening the interest margins because the interest cost, I think they are competing with government and treasury bonds which are issued by CBK as well as I think money market has been generally tight so I think banks are paying higher rates on their borrowing so that has tended to increase their interest expense.”

On Provisioning for Bad Loans:

“I think KCB is definitely the highest among the listed banks and given its size of course it impacts the overall ratios of the industry as well. I think their non-performing loans as at March were 17.3% of the book which was above the industry average. Most banks seem to have been making reasonable provisions. I think overall, everybody is within 50 - 60% of the non-performing loans having been provided for. I think the outliers in that, there were around 2 outliers which is, StanChart has the highest level of provisioning. I think they have provisioned about 78% of their non-performing loans and I think StanChart has traditionally tended to be more conservative in provisioning. On the lower end of the provisioning scale are DTB and NCBA which are below 50% in terms of provisioning. I think everybody else falls within the 50 - 60% band.”

On Profitability:

“In general, most of them have recorded very good performances. I think the stand-out stars really have been Stanbic Bank which increased profits by about 84%, Absa Bank with a 51% increase, NCBA 49%, and StanChart 46%. And the interesting fact about these stars in performance recorded this growth despite fairly hefty increases in provisions for non-performing loans. So they were able to absorb and increase provisioning on the bad debt book but at the same time, they managed to record very good growth in their profitability. The only 2 banks among the listed banks which had a slight fall in profit in the first quarter compared to 2022 were KCB and I&M, and both had a very high level of increase in provisions. I think KCB provisions were almost doubled and in I&M’s case, it was actually more than 2.5X the provisioning compared to the first quarter of last year. So that accounted for the performance being flat to negative.”

Find a consolidated document for Kenyan banks’ Q1 2023 results here.

Markets Wrap

The NSE: In Week 22 of 2023, Olympia was the top-performing stock on the Nairobi Securities Exchange, unchanged from last week, appreciating by 19% to KES 3, while Express PLC was the worst-performing stock, falling 10% to KES 0.18. The NSE 20 index rose by 4.6% to 1,556.6 points while the NSE 25 index was up 6.3% to 2,699.8 points. The NSE All Share Index (NASI) appreciated by 7.3% to close above 100 points at 105.1 points, ending three consecutive weeks below 100. Equity turnover was up 2.1% to KES 1.4B while bonds turnover fell by 51.1% to KES 7B.

Treasury Bills: In the short-term public debt markets, the weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day treasury bills were 11.103%, 11.112%, and 11.497% respectively. The total amount on offer was KES 24B with the CBK accepting KES 20.6B of the KES 22B bids received, to bring the aggregate performance rate to 98.2%. The 91-day and 364-day instruments recorded 511.31% and 25.63% performance rates, respectively.

Here is what Sunil Sanger had to say on #MwangoSpaces on Banks Q1 2023 results with regards to asset allocation to government securities in the context of the surging interest rates on the shorter-term instruments as compared to the longer-dated ones:

“I think if you look at the trends of government borrowing over the last 2 to 3 years, even 2.5 years ago, the government borrowing was about 30% on treasury bills and 70% on longer-term government bonds. And that ratio, by March this year, had turned to such an extent that borrowing on treasury bills was less than 15% of the total borrowing by the government and 85% was on government securities. And we look at what securities have been issued over the last 2 years, they have generally tended to be very long, you know 15 years, 10 years, 20 years - that kind of paper. So I think banks are sitting with very mismatched investment portfolios, very long-term securities funded by very short-term deposits…I think you have seen the yield curve for the shorter term going higher and higher, I mean 3-year paper went at 14.23% or thereabout, the 91-day treasury bill has gone above 11%. So we are going to see a flattening of the yield curve. I think the longer-end is not being touched because there is more new issuance and there are very few sales/trades on that level because most holders are preferring not to book the sales so we are only seeing sporadic sales on the longer term. The yield is sort of flattening, and it could even at some point turn to a negative sloping yield curve with shorter-term rates higher than the longer-term rates.”

Sunil Sanger

Managing Director, Orion Advisory Services

June 2023 Infrastructure Bond: The CBK last week issued a prospectus for IFB issue number IFB1/2023/007 with an advertised amount of KES 60B. The period of sale is between 25th May 2023 to 13th June 2023. Notably, the instrument will be tax-free and the price quote will be on a discounted basis. The bond has a seven-year tenor with 14 interest payments.

Eurobonds: Last week, the yields fell on a week-on-week basis across the 6 outstanding papers.

KENINT 2024 yield fell the most, depreciating by 168.1 basis points to 13.951% while KENINT 2048 fell the least by 34.2 bps to 11.292%. On aggregate, yields were down 68.8 bps week-on-week.

All yields were up on a Year-To-Date (YTD) basis. KENINT 2024 led the gains at 134.8%, while KENINT 2048 appreciated the least, by 46.8 bps, and the average increase was 99.8 bps.

KENINT 2048 led price gains week-on-week, rising by 3% to 74.815, respectively, while KENINT 2024’s price was up the least at 1.8% to 93.293 On a YTD basis, with the exemption of KENINT 2024 which was up 0.8%, other prices fell, with KENINT 2034 leading price losses at 5.8% to 72.99.

Market Gleanings

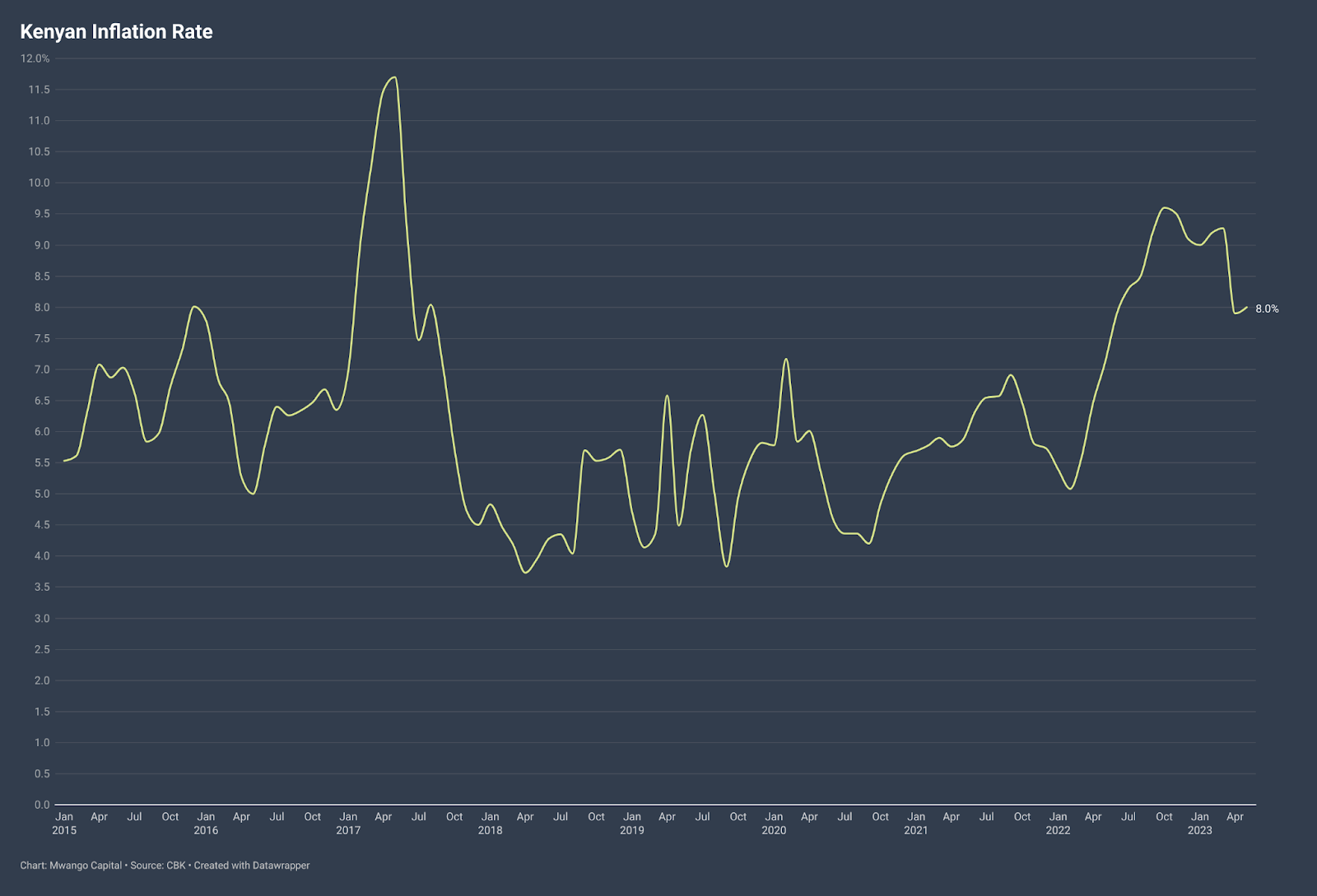

📈 | Sugar High | Kenya's May 2023 inflation barely changed from April's 7.9% and stood at 8.0%. However, two items stood out though: Sugar, which was up 49.2% YoY and 22.1% MoM and electricity which was up 66.5% YoY for 50 KW and 47.2% for 200 KW YoY. The former was mentioned by the outgoing Central Bank governor in his post-MPC briefing this week.

“We see a major risk that is coming from sugar inflation. That said of course the monetary policy does not work on sugar prices or vegetable prices & frankly, this relates to second-round effects because sugar is used for many products."

Outgoing CBK Governor, Dr. Patrick Njoroge

📈 | Tough Forex Directives | Bank of Tanzania has issued new forex directives that come into effect on June 1st, 2023. These include that all forex transactions exceeding $1M per transaction in the retail market shall at all times be traded within the interbank FX market prevailing quoted prices. Tanzania's forex reserves were down 11% YoY to $5.5B (4.4 months of import cover) as of the end of April 2023. By comparison, Kenya's forex reserves were down 23%to $6.5B (3.6 months of import cover) over the same period.

🗠 | CBK Keeps CBR Unchanged | In what was CBK Governor Patrick Njoroge’s last MPC meeting ahead of his exit on 17th June 2023, the MPC kept the Central Bank Rate (CBR) unchanged at 9.5%.

“The Committee noted that the impact of further tightening of monetary policy in March 2023 to anchor inflationary expectations was still transmitting in the economy. Additionally, the MPC noted that this action will be complemented by the recently announced Government measures to allow duty-free imports on specific food items particularly sugar, which are expected to moderate prices and ease domestic inflationary pressures. In view of these developments, the MPC decided to retain the Central Bank Rate (CBR) at 9.50%.”

🧾| Pending Bills Update | The National Treasury is set to table a Memorandum to Cabinet elaborating plans to clear KES 641B national government pending bills. Contractors and suppliers are the largest creditors at KES 407B, followed by counties at KES 160B, and Ministries, Departments and Agencies at KES 18.3B. Late last month, the national government wired KES 29.6B to counties for the month of March, cutting down the KES 94.4B the government owed counties for March, April and May. Separately, Oil Marketing Companies (OMCs) are set to receive KES 25.22B from the government in the fiscal year starting July 1 after the Treasury set aside the money to clear KES 42B owed to OMCs for the fuel subsidy,

💰 | Hustler Fund Update | As of 1st June 2023, KES 30B had been disbursed through the Hustler Fund, with the amount repaid standing at KES 19.7B. The total number of borrowers stood at 20.2M, and repeat borrowers were 7M. The aggregate number of transactions done over the platform stood at 42.5M. The President last week launched the second phase of the Fund, the Group Loan, during Madaraka Day celebrations held in Embu County. The Group Loan will see small businesses access loans ranging between KES 10K - KES 200K.

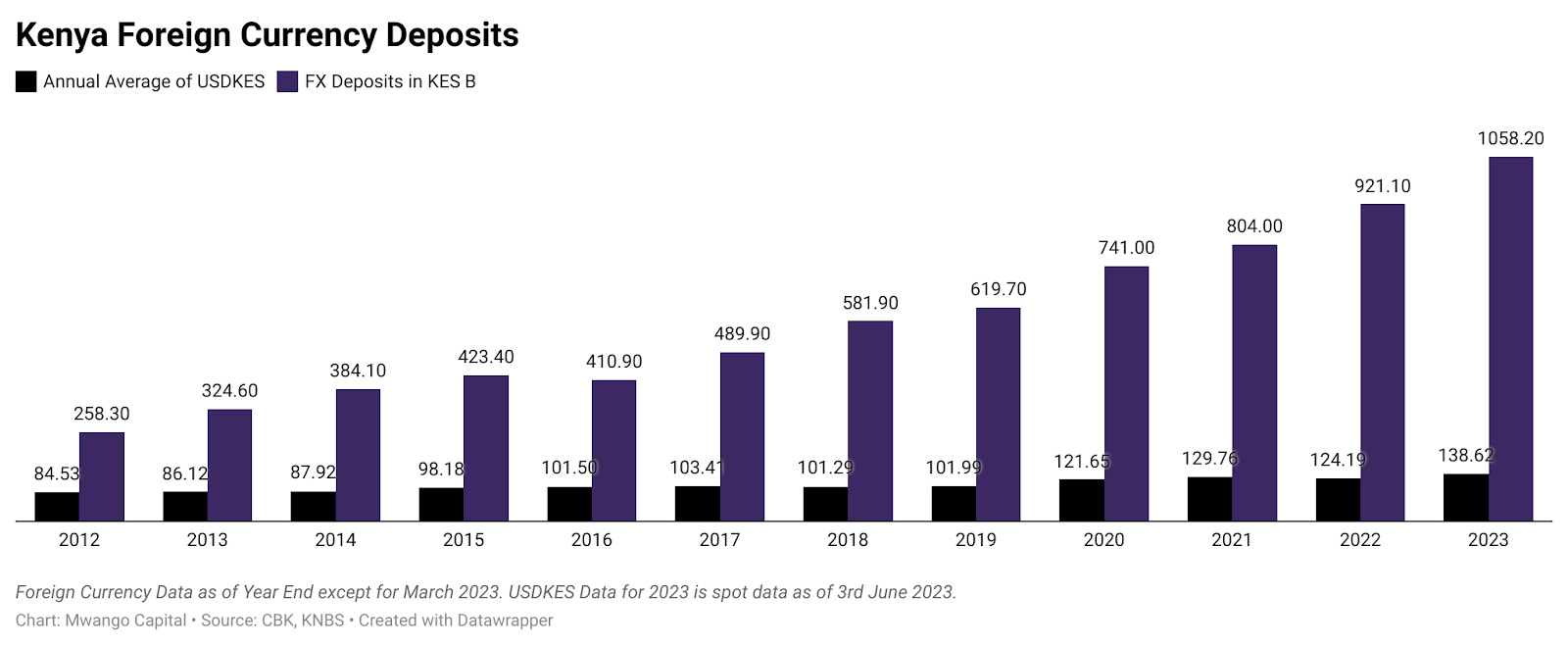

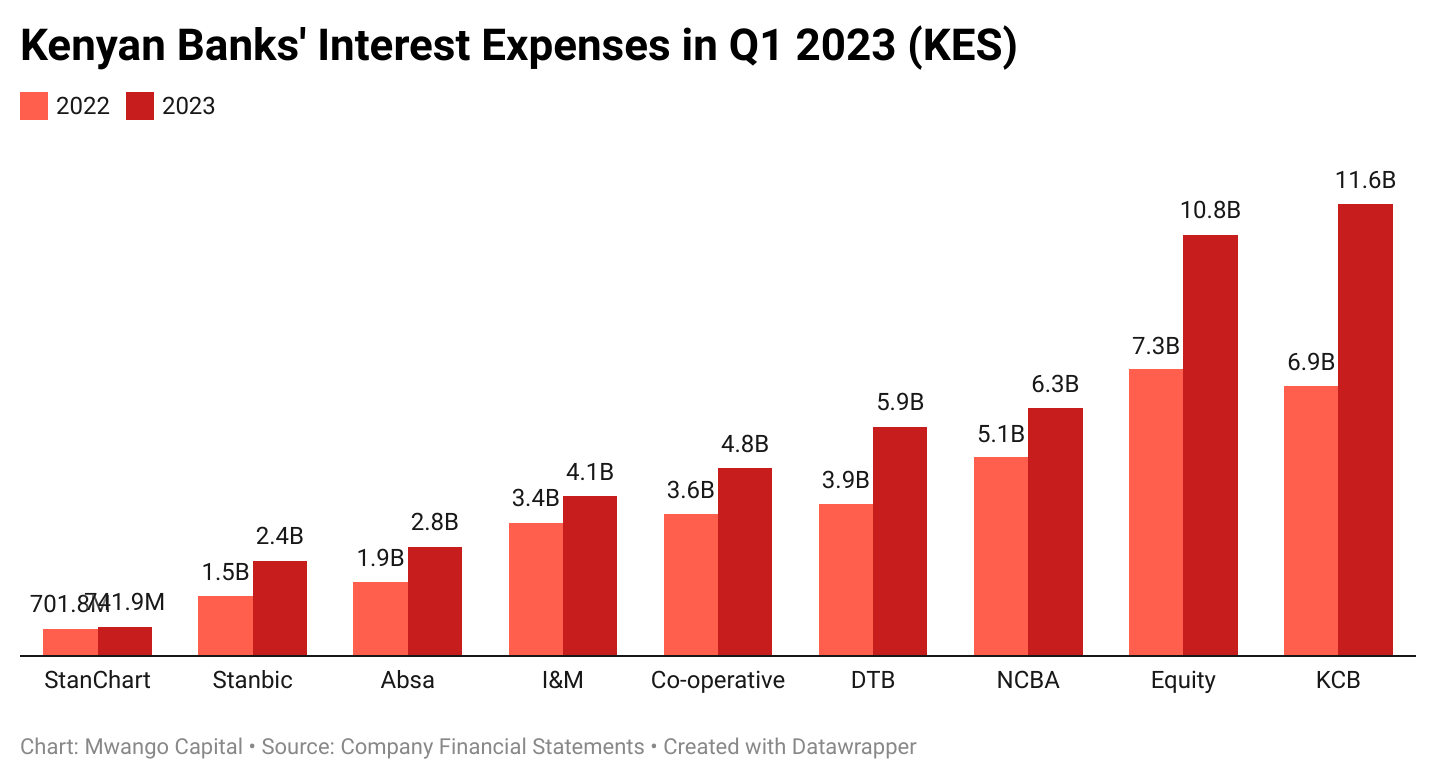

Charts of the Week