Banks Cut G-Sec Holdings

Equity, StanChart, and Cooperative reduce their holdings of gov't securities

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover Kenyan Banks Q1 2023 results and the nomination of Dr. Kamau Thugge as the tenth Governor of the Central Bank of Kenya. First off, enjoy a dose of our weekly business news in memes:

Kenyan Banks Q1 2023 Results

Equity Group Holdings, Standard Chartered Bank Kenya, and Co-operative Bank Kenya released their Q1 2023 results this week. Below are our key takeaways:

Loan Book: Equity’s loans and advances increased by 21% to reach KES 756.3B, accounting for 49% of the balance sheet, unchanged from 2022. StanChart’s aggregate lending totalled KES 137B, up 7%, equivalent to 35.3% of the asset base [2022: 37.6%]. Cooperative Bank recorded KES 360B in loans in the period, an increase of 11% to account for 57.1% of the asset base, up from 54.4% in 2022. The loan-to-deposit ratios for the three banks stood at 68.1%, 85.8%, and 45.3%, respectively, from 78.9%, 69.2% and 48.3% in 2022.

Government Securities StanChart’s pile of government securities stood at KES 95B, down marginally by 6.21% to account for 24.5% of the balance sheet, the lowest it has been in the last 5-year review period. For Cooperative Bank, government securities on the balance sheet totalled KES 179B, a 2.3% drop from 2021. Equity Group reduced its government securities pile by 7.7%, as compared to the 21% growth in net loans. As a proportion of the asset base, net loans accounted for 49.2% [2022: 49.1%], while government securities accounted for 25.5% of the asset base [2022: 30.7%]. The general trend across the board was that of a pivot away from government securities.

Asset Base: Co-operative Bank’s balance sheet expanded by 5.7% to KES 631.1B while StanChart's grew by 14% to reach KES 388B. The projection for StanChart is an asset base that breaches the KES 400B mark in H1 2023 with a possibility of closing FY 2023 with assets in excess of KES 450B. Equity Group’s asset base expanded the most across the banks that have reported so far, increasing by 21.1% to a total of KES 1.54T.

Interest Income Mapping: In the operating period, StanChart Kenya recorded KES 7.6B in gross interest income, up 34.1%. Interest Income from Loans grew faster, at 29.4% compared to the 8.9% growth in interest from government securities. Cooperative Bank’s gross interest revenue rose by 11.2% to reach KES 15.6B, while Net Interest Income expanded by 4% to KES 10.8B. Equity Group’s Total Interest Income edged higher by 21.6% to KES 32.4B, while on a net basis, interest income edged higher by 12.1% to KES 21.7B on account of a higher pace of growth in interest expense as a result of repricing of interest rates. Here is what the Equity Group CEO had to say about the increased interest expenses.

“Just one more line I would like to draw your attention to is borrowed funds. If you look at borrowed funds, they’re in dollars. And they were LIBOR+. Now, LIBOR moved from 0.35% when we borrowed, and it's now 5.5%. What rate did we borrow at? We borrowed at an average of 2.7% to 3.5%. What are we paying now? Between 8 and 9%. Three times on 160B Kenya shillings. Loans grew by 21% and interest grew by 21%, but look at interest expense, it grew by 47% because of repricing the loans that we had borrowed globally, which we used to pay at 3%, but we are now paying at 9%.

Equity Group CEO, James Mwangi

Loan Loss Provisions: After reporting KES -86M in loan loss provisions through the income statement in Q1 2022, and aggregate provisions of KES 1.3B in FY 2023, StanChart’s provisions grew substantially year-on-year, but were down by 39.2% quarter-on-quarter to KES 790.9M. Co-operative Bank provisions edged higher by 0.7% to KES 1.5B while Equity’s provisions were up a whopping 92.5% to KES 3.5B. The cost of risk stood at 0.6% for StanChart, 0.24% for Cooperative [2022: 0.26%], and 0.46% [2022: 0.29%] for Equity.

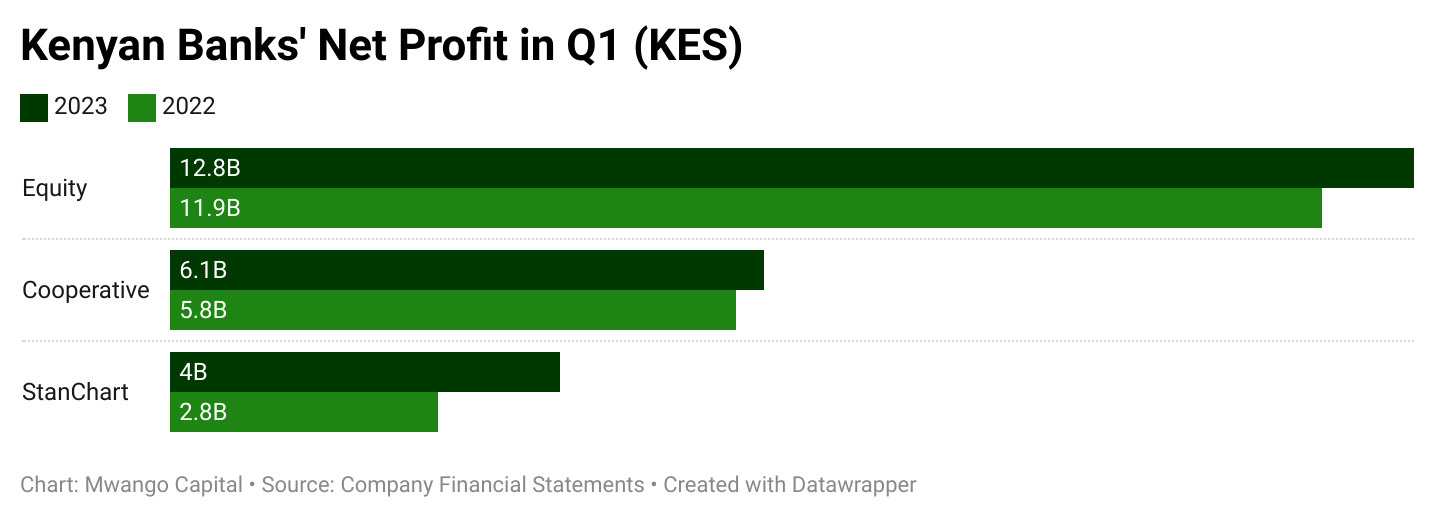

Profitability: StanChart’s Total Operating Income grew the most at 45.2% to reach KES 10.8B, Equity’s increased by 28.2% to KES 40.1B, while that for Co-operative rose by 10.8% to reach KES 17.9B. Notably, in a span of three years, Equity has managed to double its Gross Operating Income to KES 40.1B from KES 19.9B in 2020. Net profit increased the most at Co-operative at 47.2% to KES 6.1B, StanChart 45.7% to KES 4B, while Equity recorded the least growth at 7.9% to KES 12.8B.

Here are links to the full results of Equity Group Holdings, Standard Chartered Bank Kenya, and Co-operative Bank of Kenya.

Equity’s Insurance Play: The Insurance Regulatory Authority granted Equity Group in-principle approval to set up a general insurance company. Last year, Equity launched Equity Life Assurance Kenya (ELAK), and in 9 months of operations, Gross Written Premium stood at KES 3.99B - ranking 11th out of 25 life insurance companies - and with an asset base of KES 5.5B.

Regional Developments: CRDB Bank, Tanzania’s largest bank by asset size at TSHS 11.9T ($5.1B), this week announced that it had formally ventured into insurance by launching a new full-fledged subsidiary - CRDB Insurance Company (CIC). This comes barely a month after it received a licence to operate in DRC. CRDB’s entry into the DRC market now means that the top three largest East African banks by asset size have a footprint in Africa’s second-largest country. An important point to watch out for is whether the play-out of the increasing players in DRC will have an impact on Equity BCDC’s margins and market share.

Banking Supervision: This week, the CBK released the Bank Supervision Annual Report 2022. Of note is the tune of losses accrued by microfinance banks, which increased 11.7% (KES 103M) to KES 0.98B.

We compiled the key highlights of the report here.

Thugge Nominated for CBK Governor

10th Governor: Out of the 6 nominees for the position of Central Bank of Kenya Governor, President William Ruto nominated Dr. Kamau Thugge to the position, subject to Parliamentary vetting slated for Tuesday, 30th May 2023.

Profile: Currently, Mr Thugge serves as the Fiscal Affairs and Budget Policy Advisor to the President, after serving as PS to the National Treasury in Uhuru Kenyatta’s administration.

Exit Njoroge: Patrick Njoroge will be completing his 2 terms at the helm of the apex bank. Prior to joining the CBK, he was an economist at the IMF.

Incoming Governor’s In-Tray: The macro variables are at poor levels, and top of the list for the incoming governor will be the situation around the stock of Forex Reserves which currently stand at $6.3B from $7.4B at the start of the year and $8.8B as of January 2022. The debt issue is also another key matter given the mounting pile of public debt and the internal and external debt maturities Kenya faces in the Medium Term, in the context of the depreciating shilling - which fell by 9% in 2022; as well as liquidity challenges in the domestic debt market. The Total Public Debt as of March 2023 stood at KES 9.4T [March 2022: KES 8.4T], with domestic debt at KES 4.5T and external debt at KES 4.9T.

Kenya’s Energy Wrap

May/June Pump Prices: EPRA has increased the prices of super petrol, diesel, and kerosene by KES 3.40, KES 6.40, and KES 15.19 to KES 182.7, KES 168.4, and KES 161.13, per litre, respectively. The increase in prices for diesel and kerosene is steeper than that of super petrol following the removal of subsidies. The mean monthly exchange rate of the USD-KES as quoted by EPRA stood at 138.96 in April from 139.61 in March. As of April 2023, murban crude oil prices were down 8.3% in the year while the mean exchange rate as quoted by EPRA depreciated by 6.4% over the same period.

Bond to Settle OMCs? The unpaid subsidies to oil marketing companies (OMCs) are set to be settled through a bond with a schedule of amounts owed to each OMC. The OMCs will have to open accounts with the CBK to facilitate the transaction, and the bonds will either be discounted or held at will at a negotiated interest of 15% every 6 months. In its manifesto, the government outlined that it would also issue a roads bond to offset arrears owed to contractors.

Kenya Power Starts LMCP Phase 4: The electricity utility has started the fourth phase of the Last Mile Connectivity Programme (LMCP) estimated to cost KES 26.8B. 280,473 households are expected to benefit from the program that targets 32 counties, or 68.1% of counties in the country. Technically, the project will involve the installation of 940 new transformers and the maximisation of the 3,735 existing ones. Across the first 3 phases, over 1M Kenyans have been connected to electricity, bringing electricity access to over 75% of the population [2012: 29%], and an aggregate of KES 1.1B or 53.08GWh has been realised in sales.

Restructuring at Kenya Power: This week, the Cabinet approved the restructuring of Kenya Power’s balance sheet with the objective of restoring profitability and addressing asset-liability mismatches. Earlier this month, President William Ruto appointed Dr. Eng. Joseph Siror to head the utility.

Kenya Power - Ormat: In Q1 2023, Kenya Power accounted for 14.5% ($26.9M) of Ormat Technologies’ revenue [Q1 2022: 14.1%($25.9M)]. The total amount overdue from Kenya Power as of 31st March 2023 was $36.9M, of which $9.8M (26.6%) was paid in April 2023.

Across the Region: Equinor, Shell, and Exxon Mobil have agreed on a deal with Tanzania for the development of an LNG export terminal estimated to cost $30B, even though the final investment decision has not been reached. Shell operates Block 1 and Block 4 which hold 16T Cubic feet (Ccf) in estimated recoverable gas, while Equinor operates Block 2, estimated to hold in excess of 20T Ccf of gas. ExxonMobil holds a stake in Block 2.

Markets Wrap

The NSE: In Week 20 of 2023, Eveready PLC was the top-performing stock on the Nairobi Securities Exchange, appreciating by 28.6% to KES 1.08, while BOC Kenya was the worst-performing stock, falling 22.4% to KES 70. The NSE 20 index fell by 0.3% to 1,467.8 points while the NSE 25 index rose by 2.7% to 2,571.8 points. The NSE All Share Index (NASI) was up by 5.3% to 1,533.7 points. Equity turnover was up 16.4% to KES 1.6B while bonds turnover rose by 30.7% to KES 18.2B. Notably, NASI remained below 100 points at 98.5.

T-Bills: In the short-term public debt markets, the weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day treasury bills were 10.518%, 10.978%, and 11.39% respectively. The total amount on offer was KES 24B with the CBK accepting KES 35.9B of the KES 36B bids received, to bring the aggregate performance rate to 150.09%. The 91-day and 364-day instruments recorded 602.33% and 77.12% performance rates, respectively.

T-bonds: In the FXD1/2023/003 Tap Sale with KES 10B on offer, the coupon rate was 14.228%, and investors submitted KES 10.6B in bids at Face Value. The CBK accepted KES 10.6B.

Eurobonds: Last week, all yields fell on a week-on-week basis across the 6 outstanding papers.

KENINT 2024 fell by 261.3 basis points week-on-week to 14.349%, touching a one-month low, while KENINT 2048 fell the least, by 46 bps to 11.701%.

All yields were up on a Year-To-Date (YTD) basis. KENINT 2027 led the gains at 196 bps to 11.834%, while KENINT 2048 appreciated the least. By 87.7 bps to 11.701%. KENINT 2048 appreciated the least YTD, by 161bps.

KENINT 2034 led price gains week-on-week, rising by 5% to 70.364. On a YTD basis, prices on all yields except KENINT 2024 (+0.2% to 92.705) fell, with KENINT 2034 leading price losses at 9.2% to 70.364.

The softening of yields in the week coincided with Kenya's National Treasury meeting with IMF staff to discuss Medium Term Plans, Fiscal and Macro variables. This sent an indication to the markets and investors regarding the IMF's support for Kenya's economy, consequently influencing market sentiment.

Market Gleanings

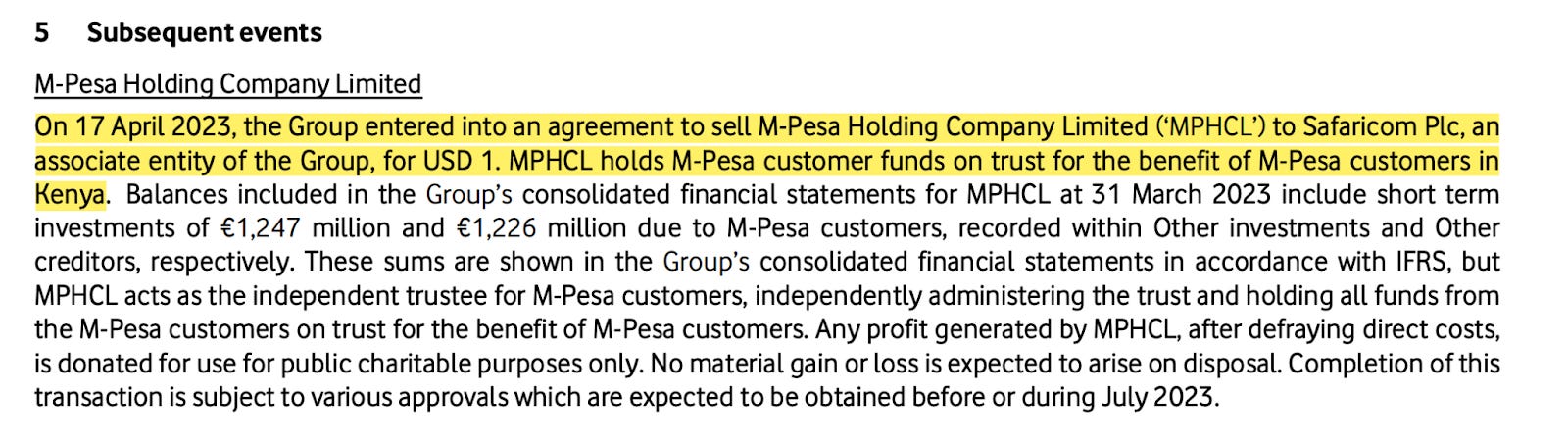

💼 | Vodafone Sells M-Pesa for $1 | Vodafone Group is set to sell the M-Pesa Holding Company Limited (MPGCL) to Safaricom for a symbolic $1. MPHCL holds the M-Pesa customer funds on trust for the benefit of M-Pesa customers in Kenya:

💵 | Safaricom in Ethiopia | Safaricom is making rapid progress in Ethiopia so far. They have ~1300 sites in the first 7 months and are aiming to reach 3000 sites by the end of this financial year about half of the total sites they have in Kenya). By comparison, Ethio Telecom has around 7,000 sites.

"In February, Safaricom hosted its first Investor Day covering its strategy and key growth factors. In addition to exciting growth opportunities in its core consumer connectivity, including fiber, Safaricom set out its growth plans for Ethiopia, M-Pesa, and enterprise. Ethiopia presents a unique opportunity to digitally and financially transform Africa's second most populous country. Having launched in October 2022, Safaricom Ethiopia has already surpassed two million customers and covered 22 cities. The growth potential of this market is further enhanced by us securing a mobile money license. We plan to commercially launch M-Pesa in the coming months, marking another exciting milestone for this early-stage investment. Safaricom Kenya has also exciting growth opportunities, including M-Pesa and the enterprise segment.”

Vodacom CEO, Shameel Joosub

💵 | IMF Approves Ghana $3B Bailout | The IMF Executive Board this week approved an aggregate amount of SDR 2.4B ($$3B) under a 36-month Extended Credit Facility (ECF) arrangement for Ghana. This approval enabled an immediate disbursement equivalent to SDR 451.4M ($600M).

“The combination of large external shocks and preexisting fiscal and debt vulnerabilities precipitated a deep economic and financial crisis in Ghana. In response, the authorities have launched a comprehensive reform program, to be supported by the ECF arrangement. It is focused on restoring macroeconomic stability and debt sustainability as well as implementing wide-ranging reforms to build resilience and lay the foundation for stronger and more inclusive growth.”

IMF Managing Director, Kristaline Georgieva

| Leadership Changes |

The Nairobi Securities Exchange has started the process of getting a new CEO by putting out a Request For Proposal (RFP) to facilitate the recruitment of a new CEO. The term of the current CEO, Geoffrey Odundo, was extended by one year to 1st March 2024.

Maurice Nduranu (new Chair), Wilfred Ole Saroni & Faith Mwaura joined Eveready PLC’s Board of Directors on 10th May, while Lucy Waithaka (exiting Chair), Fauzia Shah & Akif Hamid Butt resigned on the same day. Mr. Nduranu currently serves as the Chairperson of CPF Financial Services.

📈 | The Ethiopian Securities Exchange | Ethiopia last week started selling shares to raise funds required to set up the country’s first-ever securities exchange, the Ethiopia Securities Exchange (ESX), by 2024. The aim is to raise 75% of the required funding with the other 25% being held as a minority interest by the Ethiopian Investment Holdings, the country’s sovereign wealth fund. FSDA says that at least 50 companies, including banks and insurance companies, are expected to list at the exchange's launch.

🏛️ | On Credit Bank | The Central Bank governor has issued a notice that the proposed acquisition of 20% of the share capital of Credit Bank by ShoreCap III GP will take effect on 15th June 2023 having gotten all the necessary approvals. Shore Cap III fund is run by Equator Capital Partners and a fun fact is that in 2016, ECP acquired a 15% stake in Jamii Bora Bank for KES 600M at a Price-to-Book of 1.3X. Jamii bora bank was later acquired in 2020 by Cooperative Bank Kenya for a purchase consideration of KES 1B.

💰 | Diaspora Remittances | In April 2023, remittances totalled $320.3M, down 9.8% year-on-year. On a month-on-month basis, the remittances fell by 10.5%, and the cumulative 12-month remittances to the month ending April 2023 reached $3.985B, up 0.4% year-on-year.

Charts of the Week