Inflation Up Slightly

Kenya’s inflation in October 2023 stood at 6.9%

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a summary of key capital markets and business news items from East Africa.This week, we cover Kenya’s inflation in October 2023, SMEP MFB’s acquisition by Hope Advancement, and Uganda’s restructuring of fuel importation.This week's newsletter is brought to you by:

Co-operative Bank of Kenya. Introduce your child to the world of savings and responsible money management with Coop Bank’s Jumbo Junior Account.

Kenya's Inflation Up Slightly

10 bps: In October 2023, Kenya’s inflation rate stood at 6.9%, up 10 basis points (bps) on a month-on-month basis from September 2023. On a year-on-year basis, inflation was down by 270 bps. This is the 4th consecutive month this year that the inflation rate has fallen within the Central Bank of Kenya's (CBK) target band of 5.0% +/- 250 bps.

Surging Transport Prices: The transport index (9.6% weight) was the fastest growing year-on-year, posting double-digit growth of 13.6% on account of increases in fuel prices recorded from the start of H2 2023. The alcoholic beverages, tobacco and narcotics index (3.3% weight) was the second-fastest growing index at 9.0% followed by the food and non-alcoholic beverages index (32.2% weight) at 7.8%. The information and communication index (7.8% weight) posted the lowest growth at 1.0%.

Elevated Electricity Costs: Across commodities, the price of 50 kWh of electricity rose by 44.1% year-on-year to KES 1,388.99 to become the commodity with the highest price change from October 2022. For 200 kWh of electricity, the price was up 30.3% year-on-year to KES 6,686.00. On a month-on-month basis, the changes across the 50 kWh and 200 kWh of electricity were 3.3% and 5.0%, respectively, as compared to -2.5% and -2.1% in September 2023.

Across Borders: Uganda’s annual headline inflation fell to 2.4% in October 2023 from 2.7% in September 2023, while core inflation stood at 2.0%. This is a 2-year low and is down by 40 basis points from September.

Deals, Mergers and Acquisitions

ARM Meeting Creditors: ARM Cement, which was placed under administration with effect from 17th August 2018, and subsequently placed under liquidation on 1st October 2021, has issued a notice of its second meeting with creditors slated from 15th November 2023 from 10:00 AM. The meeting will be held virtually.

“The purpose of the meeting will be to lay before the meeting the account of the Liquidators’ acts and dealings, and the conduct of the liquidation during the preceding year.”

SMEP MFB Acquisition: The Central Bank of Kenya (CBK) this week announced the acquisition of a 51% stake in SMEP Microfinance Bank by Hope Advancement Inc. Hope is a wholly owned subsidiary of HOPE International Inc., a charitable organization based in Pennsylvania, USA.SMEP Microfinance Bank is a large microfinance bank in Kenya with a 5.09% market share. The acquisition is expected to strengthen SMEP MFB through the injection of additional capital, improvement of IT infrastructure, and reconstitution of the board to bolster governance.

Base Resources to Exit Kwale: Base Resources is set to close down its Kwale operations at the end of December 2024 as per the current mine plan. Base resources focus at Kwale now turns to detailed closure planning and transition to post-mining land use, and will focus on the Toliara Rare Earth project in Madagascar after the Kwale mine closure.

“We have explored all avenues for further extending the life of Kwale Operations. However, despite these efforts and broad support from the local community, we have been unsuccessful in identifying additional mineral deposits of sufficient grade or scale to support a further extension.”

Base Resources Managing Director, Tim Carstens

Africa Capitalworks Acquires Cipla Stake: The COMESA Competition Commission has unconditionally approved the buyout of Cipla’s entire 51.18% stake in Quality Chemical Industries, and according to reports, Cipla is expected to earn USD 25M - 30M from the transaction.

“The committee determined that the merger is not likely to substantially prevent or lessen competition in the Common Market or a substantial part of it, nor be contrary to public interest.”

Chair of the COMESA Committee Responsible for Initial Determination, Dr Mahmoud Momtaz

Markets Wrap

NSE: In Week 44 of 2023, CIC Insurance was the top-performing stock, up 17.1% to close at KES 2.19. Sasini was the worst-performing stock, down 14.8% to close at KES 20.45. The NSE 20 index fell by 1.3% to close at 1,443.4 points, the NSE 25 dropped by 3.9% to close at 2,307.8 points, and the NASI index fell by 4.1% to close at 85.7 points. Equity turnover went down to KES 622.8B from KES 2.3B the prior week while bond turnover closed the week at KES 0.88B compared to the prior week’s KES 11.6B.

Treasury Bills: The weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day were 15.1863%, 15.2714%, and 15.4391% respectively. The total amount on offer was KES 24B with the CBK accepting KES 23.71B of the KES 24.67B bids received, to bring the aggregate performance rate to 102.82%. The 91-day and 364-day instruments recorded 562.00% and 9.14% performance rates, respectively.

Eurobonds: In the week, yields fell across the 6 outstanding papers.

KENINT 2028 fell the most week-on-week, down by 105.9 bps to 12.283% while KENINT 2024 fell the least, depreciating by 66.3 basis points to 13.332%. The average week-on-week change stood at -85.28 bps.

KENINT 2028 rose the most on a year-to-date (YTD) basis, appreciating by 197.1 bps to 12.283% while KENINT 2048 rose the least at 67 bps to 11.494%.

Prices rose across the board week-on-week, with KENINT 2034 rising the most at 6.6% to 71.671. KENINT 2024 appreciated the least at 0.5% to 96.193. Year-to-date, KENINT 2024 was the only price that rose, appreciating by 4.0%. The largest price losses YTD were 7.5% for KENINT 2034 to 71.671. The average price change week-on-week and YTD was -0.03% and 0.04%, respectively.

Market Gleanings

⛽| UG to Cut Reliance on KE for Fuel | Uganda is proposing a law to cut its reliance on Kenya for petroleum products. Uganda currently imports more than 90% of its petroleum products through the port of Mombasa. The proposed law would give the Uganda National Oil Company Limited (UNOC) the mandate to source and supply petroleum products for the country. The move is a response to Kenya’s government-to-government importation deal with UAE and Saudi Arabia which has exposed Uganda to an increase in pump prices.

⚠️| C&G Profit Warning | Car & General (Kenya) plc has issued a profit warning, stating earnings for the 15-month period ending 31st December 2023 are expected to fall by 25% in comparison to 2022. The drop in performance is due to FX losses, deterioration of unit economics of motorcycles, finance costs growth, and demurrage costs in Tanzania. Separately, Longhorn Publishers announced a delay in the approval and publishing of financial statements for the year ended 30th June 2023 on account of ongoing consultations regarding the interpretation and application of an accounting standard.

🛑| US to Revoke AGOA Benefits | In a letter to Congress, US President Joe Biden announced that the United States will terminate the designation of the Central African Republic, Gabon, Niger, and Uganda as beneficiary sub-Saharan African countries under the African Growth and Opportunity Act (AGOA), effective 1st January 2024 due to their failure to meet AGOA eligibility requirement, which include respecting internationally recognized human rights, establishing the rule of law, and protecting political pluralism. Uganda's case is a response to the country's anti-LGBTQ laws.

💱| Improving Tanzania FX Situation | In a statement by the Monetary Policy Committee of the Bank of Tanzania (BoT), the Bank’s Governor noted that the shortage of foreign currency was easing in the country on account of inflows from cash crops, minerals, manufacturing, and tourism. The BoT’s participation in the interbank FX market has also helped to unwind the shortage and ease the access of US dollars in the market.

💰| IMF Agreements | The IMF concluded agreements last week with some countries across the Horn and East Africa. Here is a rundown:

Tanzania: The IMF has reached a staff-level agreement with Tanzania on economic policies and policies to conclude the second review of its economic program under the Extended Credit Facility (ECF). The agreement is subject to approval by the IMF management and Executive Board. Upon completion of the review, Tanzania will have access to USD 113.37M, bringing the total IMF financial support under the agreement to USD 452.7M.

Rwanda: The IMF and Rwanda have reached a staff-level agreement on policies to complete the second review of Rwanda’s policy Coordination instrument and program under the Resilience and Sustainability Facility (RSF). The two sides also agreed on a new 14-month Standby Credit Facility (SCF) with a total access of about USD 262M to help mitigate the balance of payment pressures arising from climate-related shocks. Upon approval, Rwanda would have access to USD 48.5M under the RSF and USD 87.5M under the SCF.

Somalia: The IMF and Somalia have reached a staff-level agreement on economic policies and reforms to be supported by a new 36-month arrangement of about USD 100M under the ECF. Somalia is on track to reach the Heavily Indebted Poor Countries (HIPC) completion point in December 2023, which will pave the way for debt relief and a full normalization of relations with its key creditors. The new program aims to bolster key economic institutions and foster macroeconomic stability and growth.

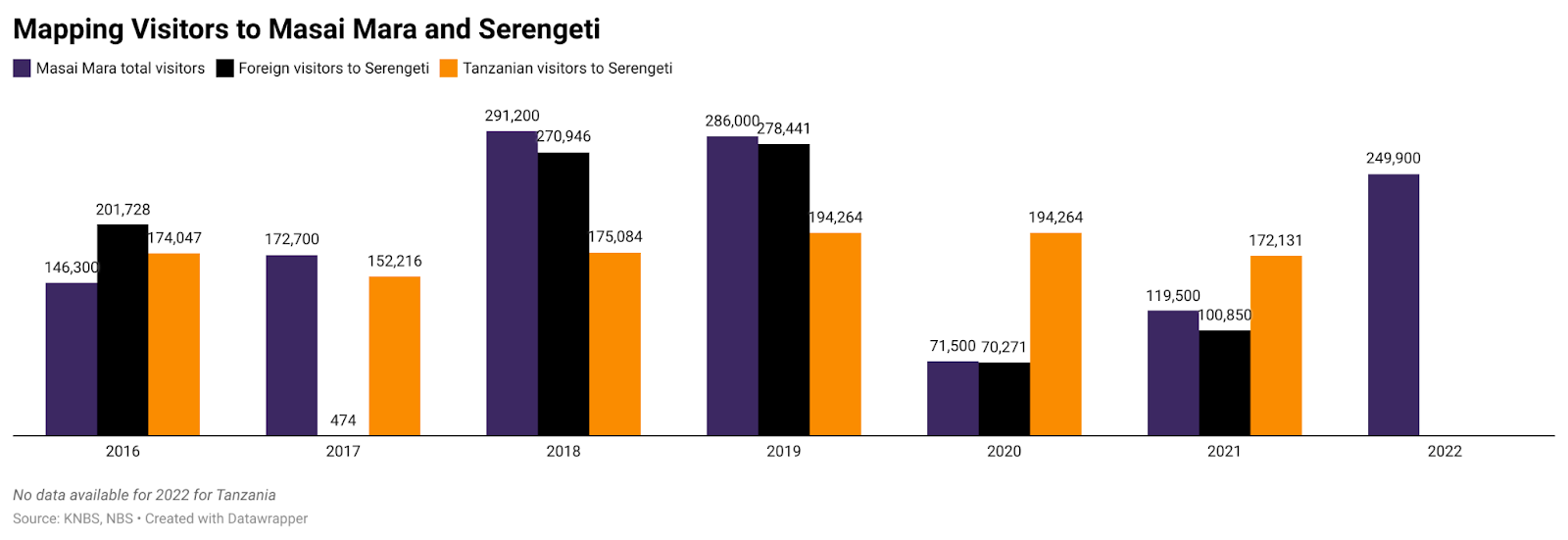

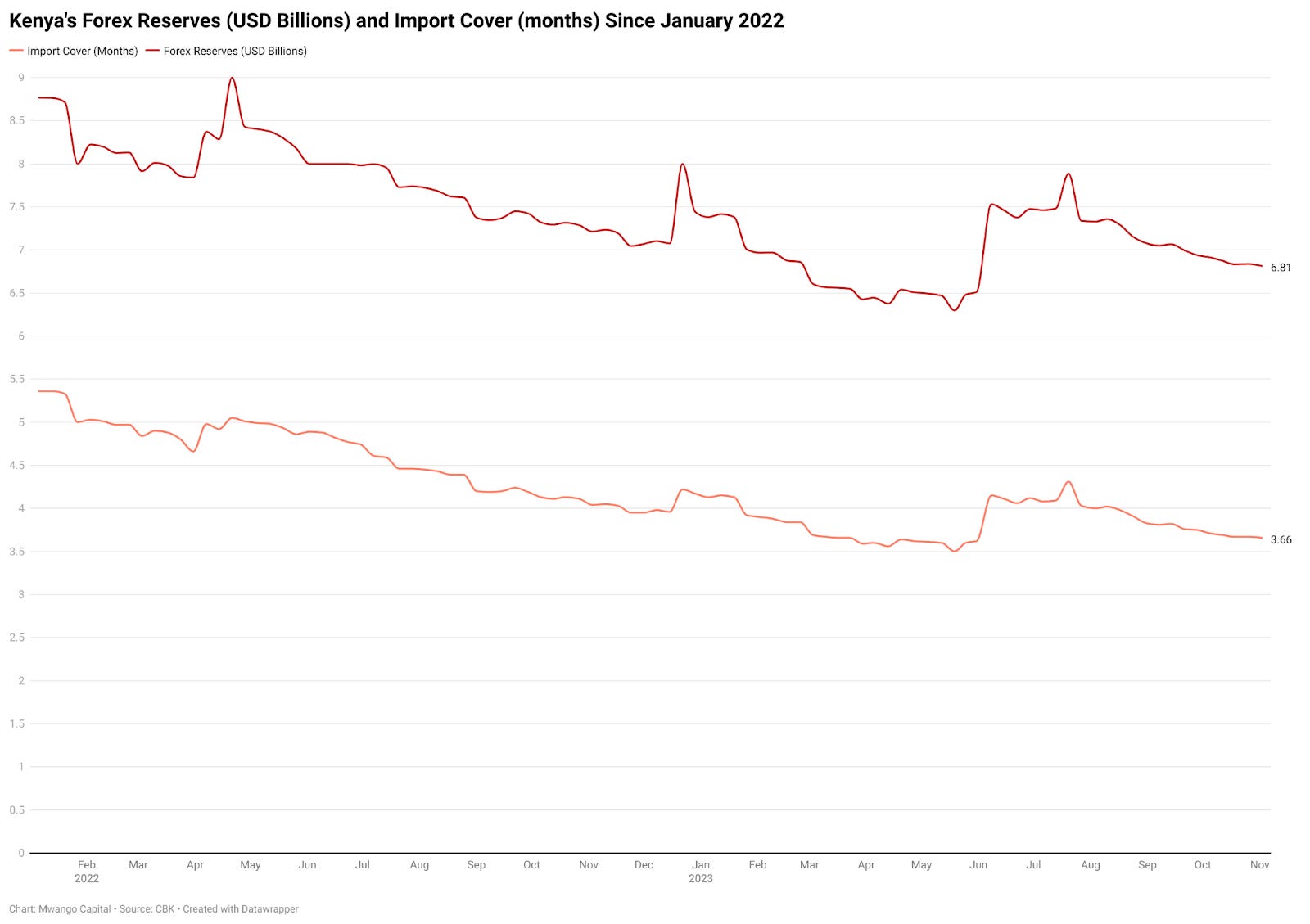

Charts of the Week