Rating Agencies on the Spot

Is a Buyback a Default?

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover Kenya’s inflation in July 2023, the upcoming banking sector earnings season, and Moody’s rating comments on Kenya.First off, enjoy a dose of our weekly business news in memes.

This week's newsletter is brought to you by:

Co-operative Bank of Kenya. Ready to take control of your financial future? Start your journey to financial success with a YEA Account. Save, invest, and grow your wealth with access to mobile loans and a range of financial benefits.

Rating Agencies on the Spot

Is a Buyback a Default? Kenya has USD 2B in Eurobonds maturing next year in June. The government has been considering various options including buybacks. A buyback can be done either in the open market or via the submission of a tender offer to bondholders. Though Kenya has yet to give details on which approach it will use, Moody’s poured cold water on the buyback option saying that buying the bonds back at a price below par value might be deemed a default:

“We deem a distressed exchange occurs when there are economic losses to creditors and when the transaction has the effect of allowing the issuer to avoid a likely eventual default. We need to see the details and the terms of the buyback before we can assess whether it constitutes a distressed exchange, and therefore a default under Moody’s definition.”

David Rogovic, vice president & senior credit officer at Moody’s

What to Do? We asked Mark Bohlund, Senior Credit Analyst at REDD Intelligence, about the upcoming KENINT 2024 maturity, its refinancing, and the buyback option:

“The refinancing is likely to include a cash buyback of part of the 2024 Eurobond, although it can be questioned what utility such a buyback would have if only months remain on the maturity…Kenya’s 2024 Eurobond is currently indicated at 95-96 according to Cbonds, in line with bonds of equivalent maturity from similarly and higher-rated peer sovereigns. This contrasts sharply with the sharp discounts Ecuador paid for bond repurchases in its recent debt-for-nature swap which Moody’s deemed as being a distressed debt exchange. The Ecuadorian government repurchased just over USD 1bn in face value of its 2035 bond at 38.5 cents on the dollar, USD 202m of a 2030 note bought at 53.25 cents, and USD 420m of a 2040 bond bought at 35.5 cents. Kenya’s repurchase prices are unlikely to be at such a “substantial discount to par”.”

Concerns Raised: Following Moody’s comments, the African Peer Review Mechanism, which supports African countries on credit ratings, has termed the comments by Moody’s as highly speculative and damaging given that details on the buyback are scanty. Kenyan President, Dr. William Ruto, over the weekend, also expressed his concerns over the influence of credit rating agencies:

“The APRM notes with concern the comments made by Moody’s Investors Service on 2nd August 2023 in which the rating agency states that it will treat Kenya’s planned buyback of a portion of its Eurobond debt as default….The APRM views the comment as highly speculative, damaging and ignores the ‘voluntary’ nature of the proposed bond buyback program.”

“Last week me and my finance CS Prof Njuguna Ndung’u in collaboration with some partners came up with a plan to repay the debts earlier because we did not want to wait until next year. But strangely, some rogue credit rating agencies who are used to using unorthodox means to inflate our debts wrote some letter demanding to know why we want to repay earlier than scheduled, but I know they wanted us to default.”

Kenyan President, Dr. William Ruto

Yields Rise: The comments by Moody’s seemed to have spooked investors sending Kenya's 2024 Eurobond up 98.7 basis points week-on-week to end the week at 12.98%.

Side Note: Buybacks need to be executed discreetly as they can result in price increases that move against your original intention to buy back:

“…the repurchase method was employed by a number of Heavily Indebted Poor Countries to reduce their debts. Funding for those countries’ buybacks came from official sector grants. However, in those contexts, as pointed out by Bulow and Rogoff (1988), debt buybacks ended up being ineffective due to the accompanying price increases, and the repurchases ultimately benefitted the creditors in lieu of the sovereign debtors.”

Inflation Back Within Range

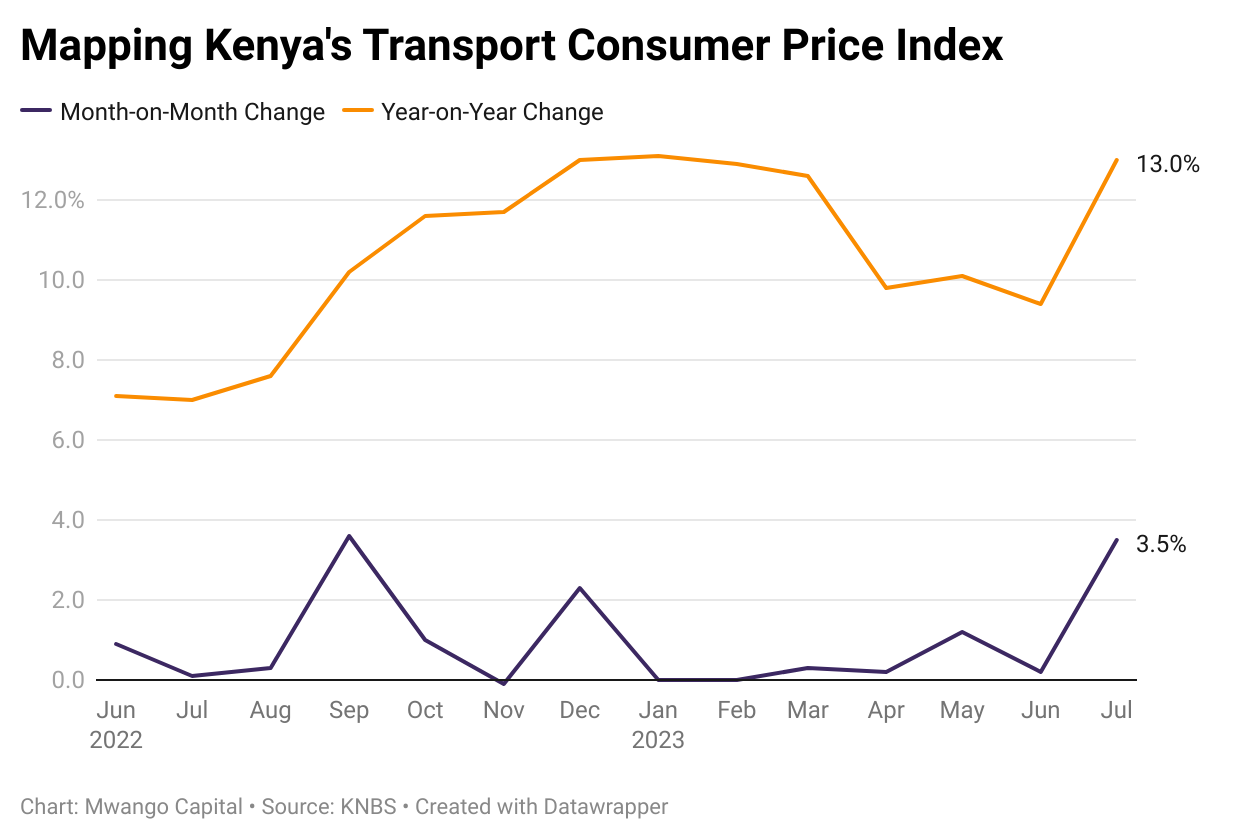

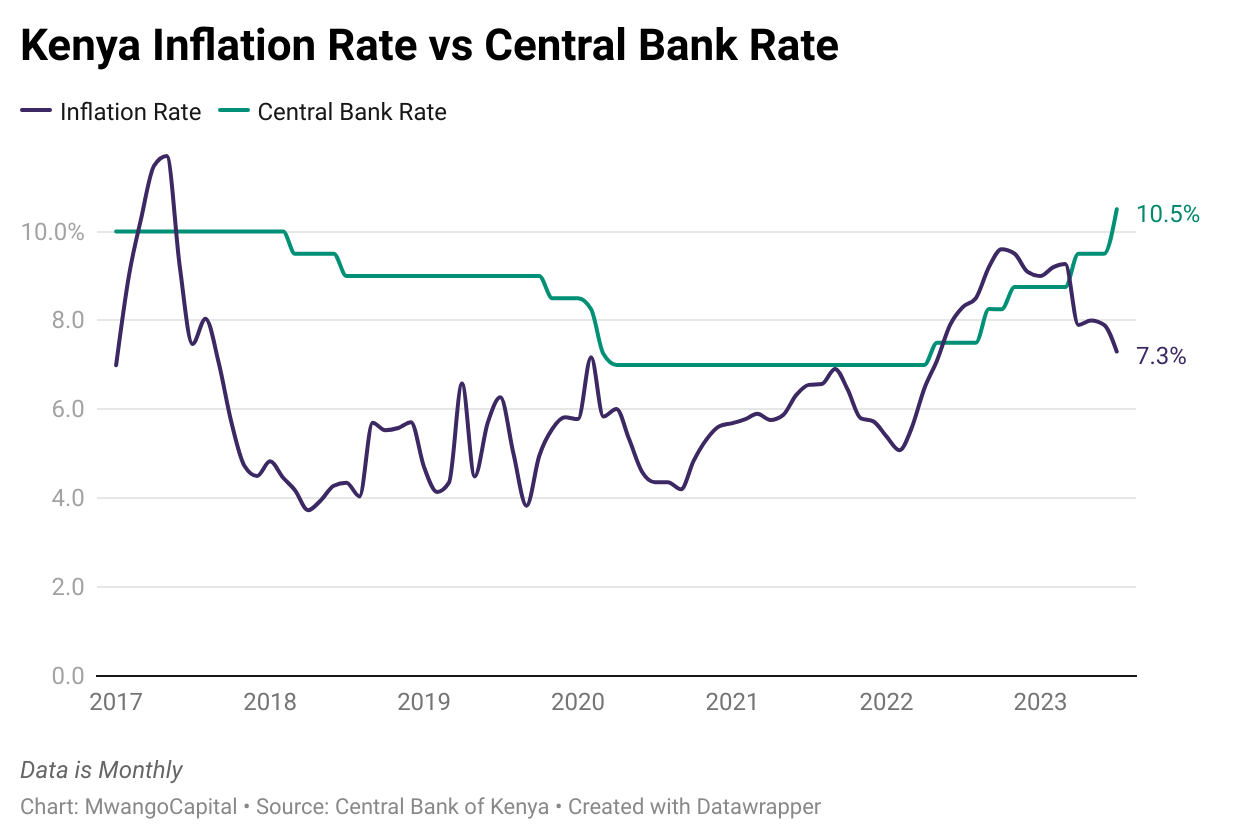

Back Within Range: Kenya’s headline inflation closed July 2023 at 7.3%, down 100 basis points year-on-year and 60 basis points month-on-month, effectively getting back within CBK’s upper target range of 7.5%. This is the first time inflation has fallen below the target range since May 2022 when it closed at 7.1%.

Niggling Transport: The impact of the doubling of VAT on petroleum products to 16% via the Finance Act 2023 resulted in the transport index rising by 13% year-on-year - the highest rising index increase across all indices. Alcoholic beverages, tobacco and narcotics were the other notable increases.

“The Transport index went up by 3.5% between June 2023 and July 2023 mainly due to increase in prices of petrol and diesel, which rose by 6.9% and 7.4%, respectively. During the same period, fares for some public transport routes went up.”

Next MPC Meeting: Central Bank of Kenya’s Monetary Policy Committee (MPC) is set to meet on 9th August 2023 with inflation set to have a key bearing in the interest rate decision. With inflation having eased to 7.3%, 320 basis points lower than the Central Bank Rate (CBR), will the MPC consider an easing in the policy stance? Perhaps not given that the Finance Act has just come into full force this past week and its effects will start being felt in full this month. In its last sitting on 29th July 2023, the MPC hiked the CBR by 100 basis points and, cumulatively, by 175 basis points in 2023. The banking sector’s umbrella body, the Kenya Bankers Association, in a research note, has argued for the retaining of the CBR at 10.5%:

“In view of the above developments, particularly the balance of risks between decisively driving down inflation levels and protecting some economic activity, and the need to allow the transmission of the policy signal effected in late June 2023 to filter through, the KBA Research Centre argues that the sustenance of the current monetary policy stance - in keeping with the CBR unchanged at 10.50% - would be appropriate.”

Across the Region: Uganda’s inflation closed July 2023 at 3.9%, down 100 basis points from 4.9% in June 2023, to reach the lowest level since March 2022. Currently, Uganda’s Central Bank Rate (CBR) stands at 10%, bringing the delta between the CBR and inflation to 610 basis points.

Bank Earnings Season Ahead

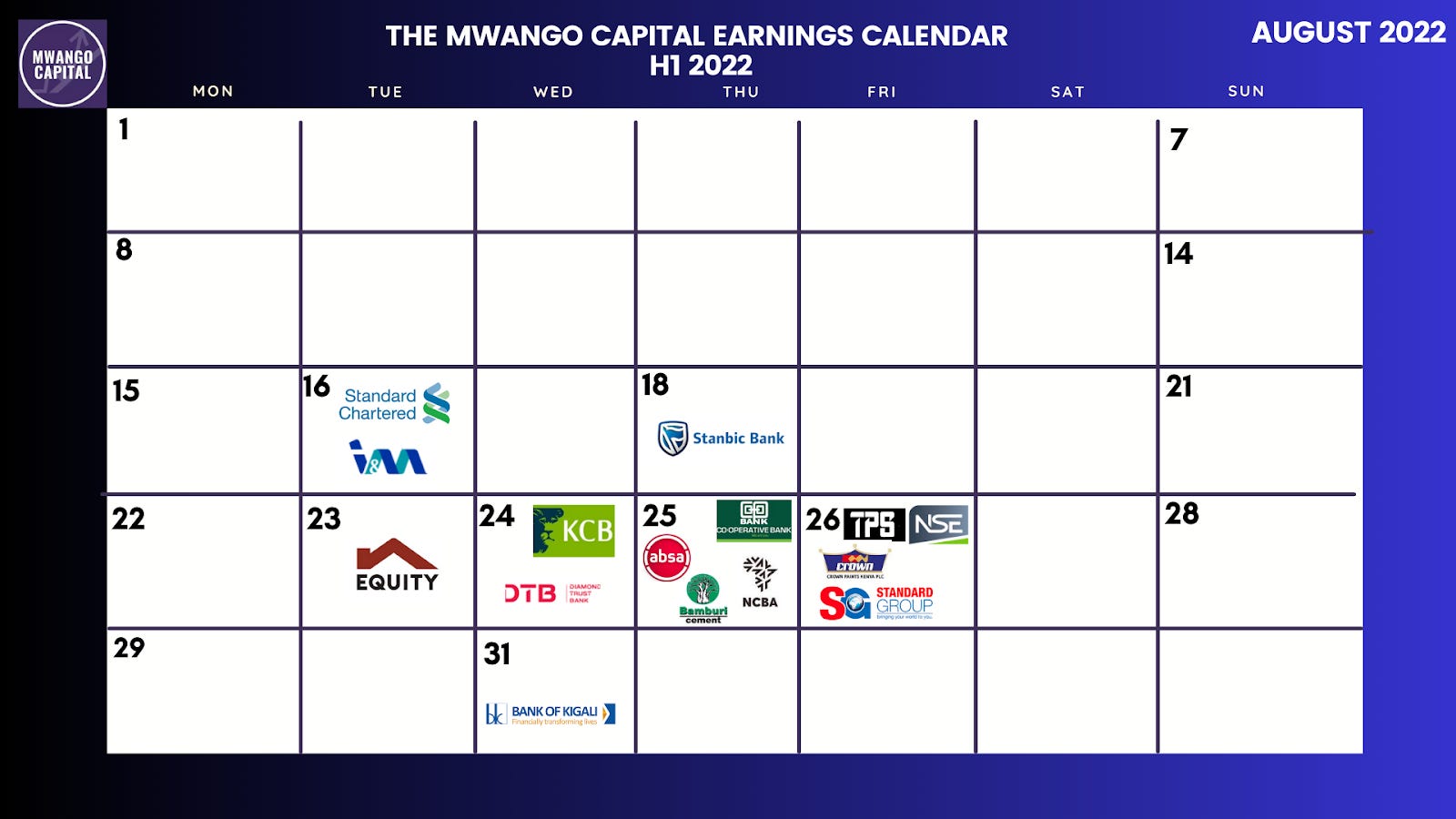

Bank Earnings Season: Kenyan banks have until 31st August 2023 to report their results for the half-year ended 30th June 2023. The first bank expected to report is Stanbic Holdings on Thursday, August 10th. Among the unlisted lenders, Bank of Africa was the first to report its H1 2023 results last week. Here is what the earnings calendar looked like last year in August:

Expectations: We asked Michael Odundo, Research Analyst at Standard Investment Bank, about his key expectations ahead of the results this month:

“Profitability should start to slow as rates rise. We see banks, especially KCB, coming under pressure as interest expenses continue to tick up which may likely cause it and other local banks to post single-digit growth rates. The lender also had thin capital ratios in 1Q23 - in excess of statutory minimums by only 0.8% - which we will be keen to look at in the half-year results. For the sector, we saw a considerable uptick in the interbank rates within 2Q23 which should eat into margins. Non-funded income growth will still be robust given the prevailing volatility in the FX market. More loan loss provisions will start to be witnessed as the NPL ratio rose to 14.9% by May from 13.3% in December. We expect NCBA to announce an interim dividend, likely KES 2, similar to last year. Stanbic and Absa should also resume payment of interim dividends.”

2022 Tax Contributions: Last week, the Kenya Bankers Association in conjunction with PwC Kenya released a report on the Total Tax Contribution of the Kenyan Banking Sector for the fiscal year ending 31st December 2022. 39 banks participated in the study [2021: 38], representing 97.65% of the market share. Here is a summary of the tax contribution:

Gross Contribution: In 2022, the participating banks made a total tax contribution of KES 181.27B, with tax collected at KES 77.99B and taxes borne at KES 103.28B. In aggregate, this was a growth of 39.96%. The total tax contribution by the sector accounted for 8.93% of all taxes in Kenya [2021: 6.8%].

Excise Duty: Excise duty from Kenya’s banking sector grew by 76.41% to KES 25.88B in 2022. The total excise duty collected by KRA from the financial services sector amounted to KES 40.89B with the banking sector contributing 63.28% or KES 25.9B.

PAYE: The banking sector’s PAYE taxes were KES 37.23B representing 7.85% of gross PAYE in 2022 [2021: KES 26.62B or 6.18%]. The rise in PAYE is on account of an 11.3% increase in employees and a 13.31% rise in employment costs between 2021 and 2022.

WHT: Withholding Tax (WHT) collected by Kenya’s banking sector was KES 37.31B, up 18.03%, while participating banks contributed KES 26.56B in taxes, up 15.49%. Growth in interest expense on deposits was the main factor behind WHT growth.

Link to the report.

Markets Wrap

NSE: In Week 31 of 2023, Longhorn was the top-performing stock, up 16.1% to KES 2.45. Britam was the worst-performing stock, down 12% to KES 4.35. The NSE 20, NSE 25, and NASI indices were up 1%, 0.7%, and 0.8% respectively closing at 1,594.2, 2,758.8, and 106.2 points respectively. Equity turnover was down 90.3% to KES 418.2M while bonds turnover fell by 52.5% to KES 8.69B.

Treasury Bills: The weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day closed at 12.686%, 12.558% and 13.107% respectively. The total amount on offer was KES 24B with the Central Bank of Kenya (CBK) accepting KES 10.3B of the KES 11.29B bids received, to bring the aggregate performance rate to 47.08%. The 91-day and 364-day instruments recorded 167.37% and 2.56% performance rates, respectively. Notably, the rate on the 364-day T-bill breached the 13% mark in the week.

Treasury Bonds: The Central Bank of Kenya issued a prospectus seeking KES 40B through the new issuance of FXD1/2032/02 and the reopening of FXD1/2023/5. The period of sale is between 31st July 2023 to 16th August 2023.

DhowCSD Takes Off: Last week the CBK officially launched DhowCSD, a digital platform that allows investors to invest in government securities in an easy and convenient way. The platform integrates functionalities such as the Central Security Depository which allows users to open and bid for government securities. DhowCSD can be accessed through its website or the DhowCSD Mobile App for Android and iOS users.

Eurobonds: In the week, the yields rose across the 6 outstanding papers this week.

KENINT 2024 rose the most, up by 98.7 basis points to 12.984%, while KENINT 2048 fell the least, down 7.5bps to 10.993%. The average week-on-week change stood at 32.47 bps.

All yields were up on a Year-To-Date (YTD) basis. KENINT 2028 led gains, appreciating by 79.2 bps, while at the lower end, KENINT 2048 appreciated by 16.9 bps. The average increase was 47.08 bps.

All instruments recorded price losses week-on-week. KENINT 2034 led price losses week-on-week, depreciating by 1.4% to 74.342. On a YTD basis, only KENINT 2024 appreciated, rising by 2.8% to 95.061. KENINT 2034 led losses at 4.1%. The average price change on a week-on-week and YTD basis was -1.0% and -0.9%, respectively.

Market Gleanings

🧾 | Sameer Africa Half-Year Results | Sameer Africa's revenue fell by 36% year-on-year to KES 201M, while gross profit was down by 14% to KES 175M to bring the gross margin to 86.8% [2021: 64.9%]. Operating profit was lower by 11% to KES 126M on the back of the depreciating Kenyan shilling and KES 48M exchange losses from term loans. Net income was also down by a significant 64% to KES 24M]. Here is the company’s outlook for H2 2023:

“The infill expansion project is at the final stages of approval and is on course to commence this year. Once completed, the new facilities will provide an opportunity to increase earnings predictably through long-term lease agreements. Further, proceeds from the sale of a portion of undeveloped leasehold land that we expect to conclude in the year will allow the Group to retire a significant portion of the debt, providing savings in finance costs and reducing exposure to foreign exchange losses.”

🛢️ | Kenya Petroleum Market Share | As at the end of Q1 2023, the top 10 companies in the petroleum market had a combined overall market share of 81.64%, up 288 basis points from Q4 2022. The retail segment accounted for 50% of the market share, down from 52.3% in Q4 2022, while resellers’ market share fell by a marginal 30 basis points to 19.7% in Q1 2023.

⛽ | Tanzania Fuel Prices Increase | Tanzania’s Energy and Water Utilities Regulatory Authority has revised the prices of Petrol and Diesel upwards by 17% and 15.4% to TZS 3,199 and TZS 2,935 per litre, respectively, for the August 2023 pumping cycle. Kerosene’s price has been lowered by 5.7% to TZS 2,668. EWURA has cited challenges in US Dollar availability, fuel levy changes, petroleum price movements in global markets and premiums in the importation of petroleum products as key factors behind the changes.

🛠️ | Developments in Nigeria | S&P upgraded Nigeria’s outlook to stable from negative on account of President Bola Tinubu’s planned reforms. Last week, Tinubu announced a stimulus package totalling N500B ($652M) targeted at various sectors as part of the government’s efforts to subdue the effects of the new government’s measures including devaluation of the naira and ending fuel subsidies. The devaluation of the naira has continued to impact the earnings of multinationals in Nigeria with Guinness announcing it was facing some challenges in acquiring US Dollars:

“At the Nigerian forex market, we have seen a little bit of offers, at rates ranging between 800 and 850 naira a dollar, but not a big supply. We expect liquidity to improve in the next couple of months. The rate is not the problem; we need dollar availability.”

Guinness Nigeria Finance and Strategy Director, Emmanuel Difom

🛠️ | Ghana’s Debt Restructuring | Ghana is inviting local pension funds to exchange about USD 2.7B of existing investments for two bonds maturing in 2027 and 2028 with an average interest rate of 8.4%. Earlier in February this year, investors exchanged debt totalling 87.8B cedis as part of a wider debt restructuring programme that now includes reprofiling of $809M of domestic USD bonds.

“This alternative offer has been designed to achieve the same average maturity, achieve a better average coupon while alleviating the cash constraint for the government during the initial years after the exchange.”

Charts of the Week

Very decent read! 👌