EPRA’s Energy Regulation Update

Kenya’s new Energy Regulations 2024 gazetted

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a summary of key capital markets and business news items from East Africa.This week, we cover EPRA’s New Energy Regulations, Stanbic Holdings FY 2023 Results, and Bamburi’s Share Sale in Hima Cement.This week's newsletter is brought to you by:

Co-operative Bank of Kenya. Whether it's restocking shelves with pharmaceuticals for your chemist, replenishing agricultural supplies for your agrochemical shop, or acquiring tools and equipment for your hardware store, their tailored financing solutions can help you get the cash you need.

EPRA’s New Energy Regulations

Restructuring: Kenya’s new Energy (Electricity Market, Bulk Supply, and Open Access) Regulations 2024 were gazetted last week and are expected to come into effect within six months (August 2024). The new dispensation is geared towards opening up access to transmission and distribution systems by opening up the electricity retail market to more players. The changes affect the entire electrical energy value chain from generation to retail supply.

“One of the expected highlights of these regulations is how we are going to structure and design the electricity market which will be developed in this country. We will be working in consultation with the Cabinet Secretary in the Ministry of Energy and Petroleum to undertake regular reviews of the electricity market to ensure it moves and evolves to the emerging needs and priorities. We will also provide guidelines for the market structure setting out the rules and performance targets for licensees during this transition phase.”

EPRA Director General, Daniel Kiptoo

Operationalization: The principle of Open Access in Kenya’s energy sector was first introduced in the Energy Act 2019 which encompasses direct bulk purchases by consumers from electricity generating companies. The upside is more distribution players entering the market, more competition which will in turn result in operational efficiency, more consumer choice, and lower prices.

“Open access holds the potential to unlock new investment opportunities to enhance great reliability and ultimately deliver greatness to consumers who can enjoy lower power bills, less frequency of outages, and more choice when it comes to electricity supply. The authority will ensure fair pricing by approving and reviewing tariffs to be charged by the licensees. With this, we will have more competition in the retail segment. We will ensure we have access as consumers and give optionality to consumers and these regulations will move us as a country to the next level.”

EPRA Director General, Daniel Kiptoo

"What we're looking at now is competition...competition in generation, competition in transmission, competition in distribution, competition in retail...right now we don't have much of consumer choice because if you're on the grid, it's either Kenya Power or Kenya Power."

Requirements: Part of the licensing requirements include the payment of wheeling charges and the use of system charges and auxiliary charges. Players will be required to provide the wheeling network for the electrical energy within the safety, reliability, and maintenance constraints required for operating a network of such a scale. Obligations of licensed players to the market include the bulk purchase of electrical energy and onward supply to consumers with whom they have standing contracts.

Banking Sector FY 2023 Results

Last week, Stanbic Holdings became the first listed Kenyan bank to release FY 2023 results.. The lender posted KES 41.3B in total income, up 28.8% year-on-year, boosted by net interest income which edged higher by 35.4% to KES 25.6B to account for 62.1% of total income [FY 2022: 59.1%]. Net income and earnings per share stood at KES 30.75, up 34.2% in both cases. The Board of Directors declared a KES 14.20 final dividend, which, in addition to the KES 1.15 interim dividend, brings the total dividend for the year to KES 15.35.

We had the privilege of hosting Stanbic Bank's Chief Finance and Value Officer, Dennis Musau, on X Space following the release of the results, and below are the key takeaways:

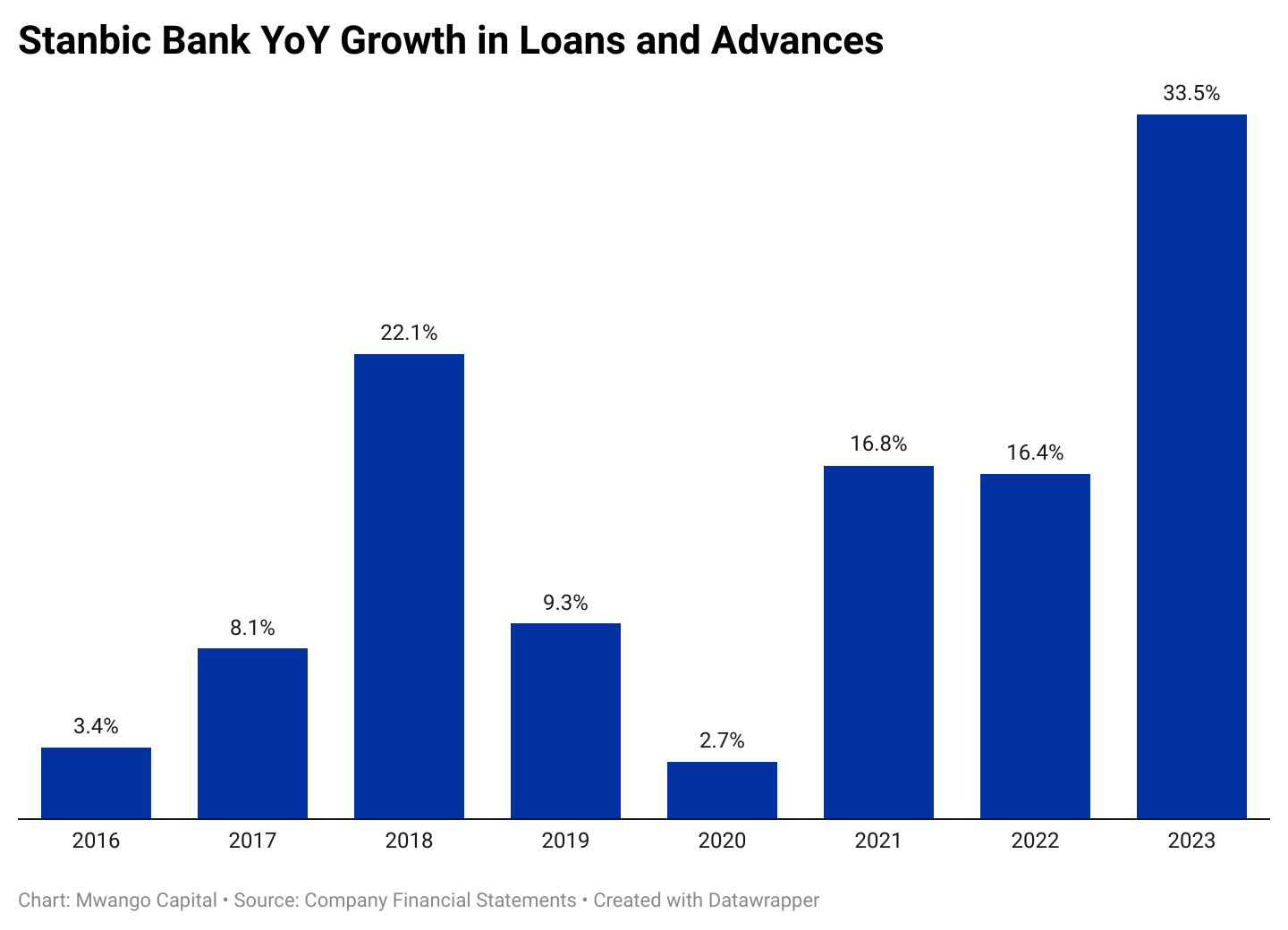

Loan Book Expands by 33.5%: The loan book notably grew by 33.5%, the highest growth in over a decade, to reach KES 356.2B and account for 77.6% of the asset base [FY 2022: 66.7%]. This coincided with a 45.7%[KES 38.2B] decline in financial investments on the balance sheet to KES 45.3B, underscoring a shift in the asset allocation strategy from investments in securities to more lending. At the group level, the customer deposit base grew by 14.1% to KES 347.2B to bring the loan-to-deposit ratio to 102.6% [FY 2022: 87.7%]. This is the first time the loan-to-deposit ratio has crossed the 100% mark since 2016 and 2015 when it stood at 111.1% and 120.6%, respectively.

“Our customer loan book term funding in 2022 was 75% as at close of 2023 that term funding was 69% so we did see an uptick in short-term facilities be they trade, overdraft, etc, and that's kind of subliminally linked to the credit appetite that we've seen from customers. We've seen more and more customers borrowing on the short end of the curve given where we've seen rates. The second thing is that the customer loans profile is a shift from foreign currency to local currency. When we closed 2022, our loan book was 48% Kenya Shillings and 52% foreign currency predominantly the dollar. We closed 2023 with a 15pp shift where local currency is now 63% compared to 37% foreign currency.”

“Customer deposits excluding interbank deposits were up 18%. Quite pleased with that actually given the competition for funding whether you think about this in the context of government borrowing, higher interest yields that can be earned from various investment opportunities. We did still record decent growth in our customer liabilities. Now, what's important to note however is that last year we reported current savings accounts, kind of your traditional funding sources, last year 2022 that was 86% of our customer deposits. That number came down to 76%. So because of the increased interest rates, we saw more and more customers migrate to fixed deposits or go and chase yield elsewhere.”

Stanbic Holdings Chief Finance and Value Officer, Mr. Dennis Musau

Improved Asset Quality: Loan loss provisions grew by 26.1% to KES 6.2B which was equivalent to 26.1% of total income [FY 2022: 15.4%]. The stock of gross Non-Performing Loans (NPLs) in the Kenyan banking unit amounted to KES 26.5B, representing a decline of 6.97%, while net NPLs were KES 7.9B, down 25.5%. Gross NPLs as a share of the loan book was 10.2% [FY 2022: 12.1%], while net NPLs represented 3% of loans [FY 2022: 4.5%]. There was a considerable improvement in the gross NPL ratio in the year which closed at 9.47% [FY 2022: 11.09%]. On a net basis, which strips out interest expenses, the NPL ratio closed 2023 at 7.51% [2022: 9.07%].

“Our NPLs ratio closed at 9.47% in 2023 compared to 11.09% in 2022. You might have seen a 9.07% NPL ratio in 2022, that 9.07% was net of interest expenses so the gross NPL ratio was 11.09%. For parity, if I do net of interest expenses the ratio will be 7.51% so generally we saw our NPL ratio kind of come down. Appetite is to keep that a single digit at less than 10%. We do think that when the industry is at around 14.8% from 13.8% in 2022. We do think 500 bps below where the market is a good risk profile for the banks so not taking risk or not taking too much risk.”

“We did see some new NPLs come into the profile during the year. Those new NPLs were particularly in the commercial sector. There are businesses that have really been impacted and think about the tail between 2022 and 2023. A lot has happened to businesses whether it's supply chain disruption or whether it is business model changes, whether it is the inflation, currency pressures, interest rates, there are businesses that struggled so we did classify some names into NPLs in 2023. But also we did write off some of the sticky NPLs that have been there for a while, especially in the unsecured area. We don't think or think it will be an inordinate effort to recover the money. We've gone ahead and written off some of those especially in the unsecured spaces in terms of loans. We look at what is realisable so that we do partial write offs where and when necessary. That is how we ended up at 9.47%, so a mix of cures, new NPLs.”

Stanbic Holdings Chief Finance and Value Officer, Mr. Dennis Musau

KES 10B Net Profit Club: Profit before taxes grew by 40.4% to KES 17.1B equivalent to 41.4% of total income earned in the operating period. On a net basis, profit edged higher by 34.2% to KES 12.2B, equivalent of 29.4% of total income recorded, [FY 2022: 28.2%].

“I am quite comfortable with that given it is weaving our risk appetite internally and at all that in sum gives you a profit after tax of KES 12.2B which is 34% up year-on-year and I was reminded earlier today that that makes us join the 10B club so I guess that's a positive thing. RoE at 18.6%. in 2020, our RoE was 10.3% in 2020. We improved that by 300 bps to 13.3% in 2021. We moved it up 200 bps to 15.3% in 2022 and now we have gotten it up 300 bps up to 18.6% so quite comfortable with the play that we have done there. That is just a function of ensuring that we are optimally capitalized but on the other side generating returns out of that capital.”

Stanbic Holdings Chief Finance and Value Officer, Mr. Dennis Musau

Dividends: The Board of Directors declared a final dividend of KES 14.20, which, in addition to the KES 1.15 interim dividend, brings the total dividend for the year to KES 15.35. This translates to a dividend yield of 12.8% based on the share price as of the market close last week.

“That gives you Earnings Per Share of KES 30.75 up from KES 22.92 in the previous years and the directors were pleased subject to shareholder approval to declare 50% of that in dividends at KES 15.35 noting that KES 1.15 of that was already paid in August [2023] as an interim dividend so the final dividend is KES 14.20 per share and that full dividend is 22% up on 2022's KES 12.6.”

Stanbic Holdings Chief Finance and Value Officer, Mr. Dennis Musau

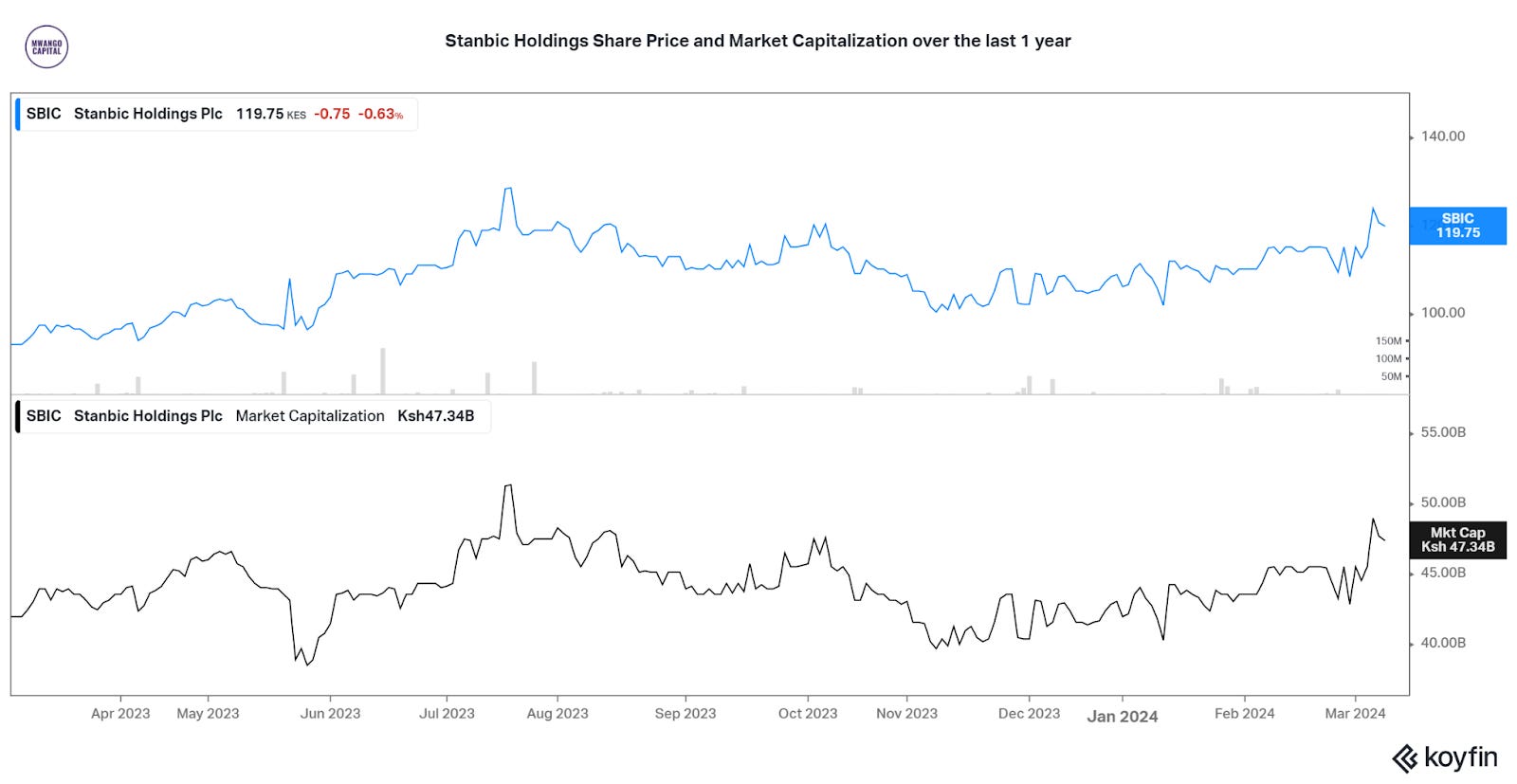

Share Price: As of market close last week, Stanbic’s share price stood at KES 119.75, up 13% year-to-date and up 11.7% over the last year. Its market capitalization closed the week at KES 47.3B.

Coming up: We expect earnings from Standard Chartered Bank Kenya on 12th March 2024 and Absa Bank Kenya and Co-operative Bank thereafter.

You can find the results here, our analysis here, and an X thread with key charts here.

Results Wrap

Tullow Oil FY 2023: In FY 23, Tullow Oil Kenya generated USD 170M in Free Cash Flow (FCF), reduced net debt by over USD 250M, and secured USD 400M debt with UK’s Glencore Energy. The firm also submitted an updated plan to develop 470 Million Barrels of Oil Equivalent (MMboe) resources and forecasts USD 800M FCF from 2023 – 2025.

MTN Uganda FY 2023: In FY 2023, MTN Uganda's total revenue edged higher by 16.7% year-on-year to USHS 2.67T (KES 108.8B). Service revenue grew by 16.1% to USHS 2.63T (KES 107.2B), equivalent to 98.5% of total revenue [FY 2022: 99.1%]. Pre-tax profits rose by 19.5% to reach USHS 706.3B (KES 28.8B). The net profit for the year totaled USHS 493.08B (KES 20.1B), up 21.4%, with the Board of Directors declaring a final DPS of USHS 6.4 (KES 0.26).

NSSF Uganda AUM Milestone: Uganda's National Social Security Fund has hit USHS 20T in Assets Under Management (AUM), 1.5 years ahead of schedule. The Fund was targeting the end of FY 2024/25 to hit the target, but as of 29th February 2024, the Fund’s AUM stood at USHS 20.018T (USD 5.1B).

Markets Wrap

NSE: In Week 10 of 2024, TransCentury was the top-performing stock, up 17.5% to close at KES 0.47. WPP ScanGroup was the worst-performing stock, down 8.5% to close at KES 2.15. The NSE 20 gained 1.1% to close at 1,556.1 points, the NSE 25 rose by 1.3% to close at 2,525.1 points, and the NASI index edged higher by 1.8% to close at 94.9 points. Equity turnover fell by 49.7% to KES 770MB from KES 1.5B the prior week while bond turnover closed the week at KES 36.2B compared to the prior week’s KES 52.6B.

Treasury Bills: The weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day were 16.6597%, 16.8477%, and 16.9845% respectively. The total amount on offer was KES 24B with the CBK accepting KES 40.3B of the KES 41.8B bids received, to bring the aggregate performance rate to 174.24%. The 91-day and 364-day instruments recorded 515.47% and 111.35% performance rates, respectively.

Treasury Bonds: Out of the KES 40B on offer across the re-opened Treasury Bond Issue No. FXD1/2024/03 dated 11/03/2024, investors submitted bids worth KES 43.1B with accepted bids being KES 34.3B. The weighted average interest rate of the accepted bids was 18.42% against a coupon rate of 18.3854%.

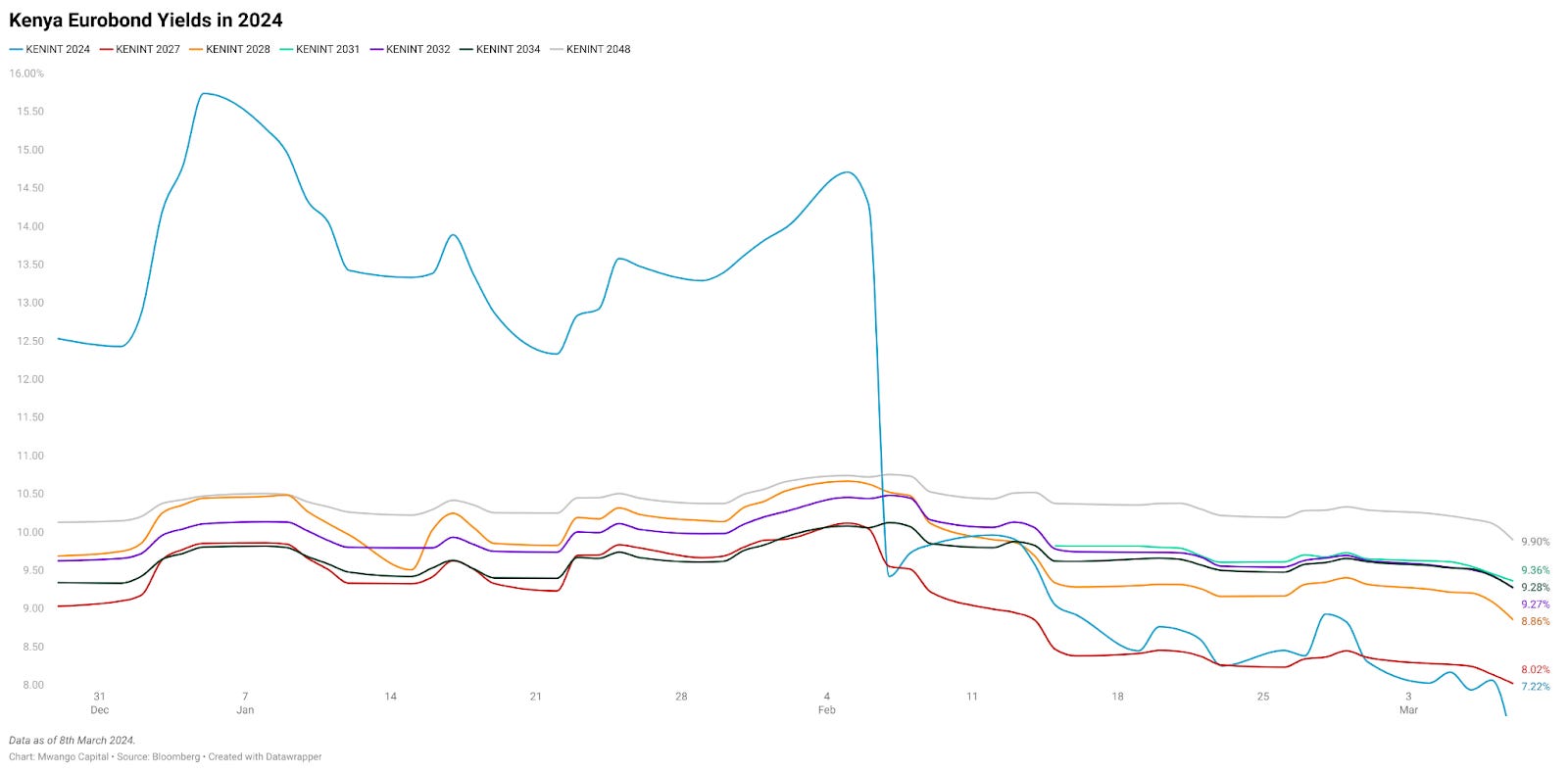

Eurobonds: In the week, yields fell across the 7 outstanding papers.

KENINT 2024 fell the most week-on-week, down by 108.80 bps to 7.218% while KENINT 2034 fell the least, depreciating by 33.60 basis points to 9.276%. The average week-on-week change stood at -117.79 bps.

KENINT 2024 fell the most on a year-to-date (YTD) basis, depreciating by 532.10 bps while KENINT 2034 fell the least at 6.10 bps.

Prices rose across the board week-on-week, with KENINT 2048 rising the most at 2.8% to 84.258 while KENINT 2024 rose the least at 0.3% to 99.875. Year-to-date, KENINT 2027 and KENINT 2028 rose the most at 3.2% to 97.159 and 94.718, respectively, while KENINT 2034 rose the least at 0.7% to 81.023.

Deals, Mergers, and Acquisitions

Bamburi’s Hima Share Sale: In the week, Bamburi Cement announced that it had on 5th March completed the sale of 1.3356M shares in its Ugandan subsidiary, Hima Cement, to Sarrai Group & Rwimi Holdings. The transaction was first announced on 14th November 2023, and the share sale saw Bamburi dispose of 1.3356M shares, equivalent to 70% of the total issued shares in Hima Cement.

EAGH Acquires Stake in I&M: The Competition Authority of Kenya last week approved East Africa Growth Holding's (EAGH) acquisition of a 10.13% share in I&M Group. EAGH is registered in Mauritius and does not have operations in Kenya. It is, however, affiliated with AfricInvest, a private equity investor, which holds a significant minority stake in Prime Bank. EAGH will acquire shares from British International Investment, gaining indirect control. Post-merger, I&M Bank & Prime Bank are set to operate independently but will have a 7.69% market share. The merger retains all 1,414 I&M employees.

E.A. Cables to sell Stake: East African Cables has entered into a share purchase agreement with Msufini Limited to sell 51% of its share capital in its Tanzania subsidiary E.A. Cables Tanzania. The sale will reshape the firm's ownership given that E.A. Cables Tanzania will cease being a subsidiary of E.A. Cables and completion of the transaction is subject to regulatory approvals.

SIB Gets Pension Licence: Standard Investment Bank has been licensed by the Retirement Benefits Authority to manage retirement benefits schemes under the Retirement Benefits Act (1997).

Market Gleanings

🧾 | eTIMS Update | Small-scale traders and farmers to feel the pinch as KRA now requires all traders to electronically generate and transmit their invoices through the eTims system, regardless of their annual turnover. Separately, The High Court has declared KRA's hiring of 1,406 Revenue Service Assistants unconstitutional for lacking ethnic diversity. Further recruitment has been barred until KRA establishes a policy that upholds ethnic diversity and regional balance and should be in place within 30 days. Separately, from the courts, the High Court has cleared the way for the Affordable Housing Bill to progress in Parliament after affirming the adequacy of the public participation process.

✅ | CBK Licenses 19 DCPs | The CBK last week approved 19 newly licensed Digital Credit Providers (DCPs), bringing the total number of licensed DCPs to 51.

"Other applicants are at different stages in the process, largely awaiting the submission of requisite documentation. We urge these applicants to submit the pending documentation expeditiously to enable completion of the review of their application."

📈 | Stanbic Bank Feb PMI | Stanbic Bank Kenya PMI for Feb 2024 stood at 51.3 (up from 49.8) indicating improving business conditions. Kenyan firms expanded staffing and boosted input purchases resulting in private sector activity expansion partly fueled by easing input and output price pressures.

🍃 | Kenya’s Debt-for-nature Plan | Kenyan lawmakers last week approved plans by the National Treasury to offer debt-for-nature and food-security swaps to bolster the nation’s finances for its next fiscal year (FY 2024/2025) set to start on 1st July.

📈 | Uganda Hikes CBR | In an unscheduled monetary policy committee meeting held last week, the Bank of Uganda hiked the Central Bank Rate (CBR) by 50 bps to 10% seeking to deal with inflation and to help shore up the Shilling which is down ~7% since August vs. the dollar and down ~3% this year. The decision comes after the MPC elected to keep the rate constant during the last 3 meetings.

🤝 | Somalia’s Admission to the EAC | Somalia last week officially became the 8th Partner State of the East African Community (EAC) after presenting its Treaty of Accession ratification to the EAC Secretary General Hon. Peter Mithuka, in Arusha, Tanzania, paving the way for the country to participate in all activities and programmes of the EAC.

💰 | Canal+ Raises MultiChoice Bid | Canal+, the biggest shareholder in MultiChoice, agrees to raise its bid to 124 rand per share, or a value of 33.7B rand (USD 1.77B) from its earlier offer of 105 rand for the shares that it does not already own. This is after MultiChoice rejected the 105 rand per share offer, saying it significantly undervalued the Group.

🤝 | IMF - Egypt Agreement | The IMF and Egypt last week inked a deal on critical Extended Fund Facility reforms, boosting economic stability with support under the current program increasing from USD 3B to USD 8B in response to Egypt's economic challenges. Egypt expects nearly USD 20B in funding from the recent actions it has pursued, with USD 8B expected from the IMF, USD 3B from the World Bank, and USD 9B from other sources. Among key reforms agreed upon included a flexible FX rate, monetary tightening, and reduced infrastructure spending to restore economic stability, manage external shocks, and foster private sector growth. Notably, Egypt's annual headline inflation rate was recorded at 35.7% in February 2024, as compared to 29.8 percent in January 2024.

Charts of the Week