Kenya’s 2023/2024 Budget

Kenya Kwanza’s debut budget

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover Kenya’s FY 2023/2024 budget and World Bank’s economic update on Kenya.First off, enjoy a dose of our weekly business news in memes.

This week’s newsletter is brought to you by:

Co-operative Bank of Kenya. Co-operative Bank of Kenya is providing reduced-interest mortgages of 9.9% on a reducing-balance basis, enabling you to borrow up to Kes 8 million to buy or build a home in any part of Kenya.

Kenya’s 2023/2024 Budget

Debut Budget: Last week, the Parliamentary Budget and Appropriations Committee chaired by Kiharu Constituency Member of Parliament Ndindi Nyoro, tabled its report on the Consideration of the Estimates of Revenue and Expenditure for FY 2023/2024 and the Medium Term. This will be Kenya Kwanza’s debut budget since its ascension to power following the August 2022 presidential election.

Here are some of the key takeaways:

Increased Expenditure: Kenya’s FY 2023/2024 budget is KES 3.68T, an 8.6% bump from FY 2022/2023. It consists of KES 1.51T in recurrent expenditure, KES 738.89B in development expenditure, KES 1.84T in Consolidated Fund Services, and KES 385.43B in Counties' Equitable Share. Across the Consolidated Fund Services, KES 1.63T has been allocated towards debt service, out of which, KES 775.14B is interest payments and KES 850.13 is redemptions.

Ambitious Revenue Targets?: Ordinary revenue consisting of direct and indirect taxes is projected at KES 2.57T, a 17% increase from the expected FY 2022/2023 collection, which the Budget and Appropriations Committee has termed as ambitious:

“The Committee notes with concern that this revenue target is quite ambitious, taking into account that historically, ordinary revenue has grown at an average of around 10%. Further, the downward revision of GDP growth projection is indicative of a concomitant reduction in revenue collection.”

National Assembly, Budget and Appropriations Committee

Fiscal Deficit: The fiscal deficit as a proportion of GDP is set to fall from 5.7% (KES 824B) in FY 2022/2023 to 4.1% (KES 663.5B) in FY 2023/2024. The reduction of the deficit in absolute terms in FY 2023/2024 is projected at KES 160.5B but is contingent on increased tax revenue collection.

“The committee notes, however, that this projected reduction in the deficit is partially attributed to an ambitious projection in tax revenue collection. Should the revenue collection not materialise, it will necessitate a downward revision in expenditure through a supplementary budget.”

National Assembly, Budget and Appropriations Committee

Borrowing: To fund the budget deficit, Treasury will be looking to borrow KES 720.1B in FY 2023/2024, 13.6% lower than the amount sought in FY 2022/2023. KES 521.5B of the borrowing will be sourced domestically while KES 198.6B will be sourced externally.

Key Sectoral Allocations: The education sector has seen its total allocation grow from 25.7% of the budget in FY 2022/23 to 27.1% in FY 2023/2024 on account of additional requirements at the junior secondary school level and the recruitment of new teachers by the Teachers Service Commission. The Energy, Infrastructure, and ICT sector had the second-largest allocation, accounting for 19% of gross expenditure.

Finance Bill 2023: The Bill seeks to increase ordinary revenue in FY 2023/2034 by KES 379.2B. Some of the key taxation amendment proposals in the bill include:

3% contribution of an employee’s basic salary (matched by 3% employer contribution) towards the National Housing Development Fund. The sum of employee and employee contributions is capped at KES 5,000.

35% taxation rate for individual employment income exceeding KES 500,000.

Revision of turnover tax from 1% to 3% and further revision of the band from KES 1M - KES 50M to KES 500,000 - KES 15M.

A requirement to deposit 20% of the disputed amount for players advancing tax disputes to the Tax Appeals Tribunal.

Standardisation of VAT on fuel products from 8% to 16%.

The National Assembly Finance and National Planning Committee will table its report on the Finance Bill 2023 next week.

You can find the National Assembly, Budget and Appropriations Committee report here.

World Bank’s June 2023 Economic Update

Barely a week after extending a $1B Development Policy Operations loan to Kenya, the World Bank has issued an economic update for Kenya. Below are some of the key highlights from the report:

Labour Force Participation: According to the Update, Kenya’s Labour Force Participation (LFP) Rate took a hit during the COVID-19 pandemic to edge lower by 5.3% in Q2 2020 as compared to Q2 2019. At the end of Q4 2022, the LFP rate stood at 66.7%, unchanged from Q1 2019. While the number of people between the 15-64 age bracket has increased by 9.3% from Q1 2019 to Q4 2022, the number of employed people has risen by 10.8%, while that of the unemployed has expanded by 172.4%. Within the same timeframe, the unemployment rate contracted to 4.9% from 6.2%.

Subsidies: In FY 2022/2023, the total absolute amount budgeted for subsidies stood at KES 22.2B, equivalent to 0.2% of GDP, 3.6X lower than KES 80.7B, or 0.6% of GDP in FY 2021/2022. While subsidies on fuel and maize were withdrawn at the onset of FY 2022/2023, the gross expenditure on subsidies in the first nine months of the current fiscal year totalled KES 43.4B, equivalent to 0.3% of GDP and 1.9X the budgeted outlay.

Pending Bills: The stock of pending bills by the national government stood at KES 481B as of the first half of FY 2022/2023, accounting for 3.3% of GDP. In FY 2021/2022, the total stock of pending bills was KES 504.7B, or 0.4% of GDP - a significant increase from KES 64.7B in FY 2018/2019 - when they accounted for 0.7%.

“A large share of pending bills is from State corporations (about 80%) compared to ministries and state departments. Regarding the composition, the largest share of pending bills constitutes payments owed to contractors/projects suppliers (around 70%). Most pending bills are due to challenges in cash management, and non-adherence to PFM systems including delayed payments, lack of commitment controls, and unrealistic budgets”

You can access the full report here.

Markets Wrap

NSE: In Week 23 of 2023, Nairobi Business Ventures was the top gainer on the Nairobi Securities Exchange, up 30.1% week on week to KES 3.33, while Eveready Kenya was the top loser, down 6.9% to KES 1.62. The benchmark indices closed the week in the green. The NASI was up 0.7% while the NSE 20 and NSE 25 were up 2.4% and 1.4% respectively. Equity turnover was down 57.2% to KES 1.4B while bonds turnover was up 5.3% to KES 7B.

Treasury Bills: In the short-term public debt markets, the weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day treasury bills were 11.414%, 11.548%, and 11.608% respectively. The total amount on offer was KES 24B with the CBK accepting KES 32.1B of the KES 33.1B bids received, to bring the aggregate performance rate to 137.95%. The 91-day, 182-day and 364-day instruments recorded 725.5%, 18.94% and 21.95% performance rates, respectively.

OMCs Bond: For the KES 45B fuel subsidy arrears accrued to Oil Marketing Companies (OMCs) in the FY 2022/2023 by the government which are equivalent to 0.3% of GDP, reports this week indicated that the National Treasury was exploring ways to convert the amount owed into a 3-year interest-earning bond.

“We raised the concern that our money was sitting with the government without earning any interest while we continue to suffer cash flow challenges.”

The plan to float a bond to offset OMCs’ arrears is similar to one devised in India in 2005/2006, which allowed India to shield its budget from OMCs’ debt. In 2013, as OMCs were sitting on bonds worth Rs 30K crore/$5.62B issued at a coupon rate of 6.9%, the yields on the ten-year instruments rose to over 8.4% from 7.86% in April 2012, exposing the OMCs to an aggregate loss of Rs 6K/$1.1B, equivalent to almost 20% of the entire bond portfolio.

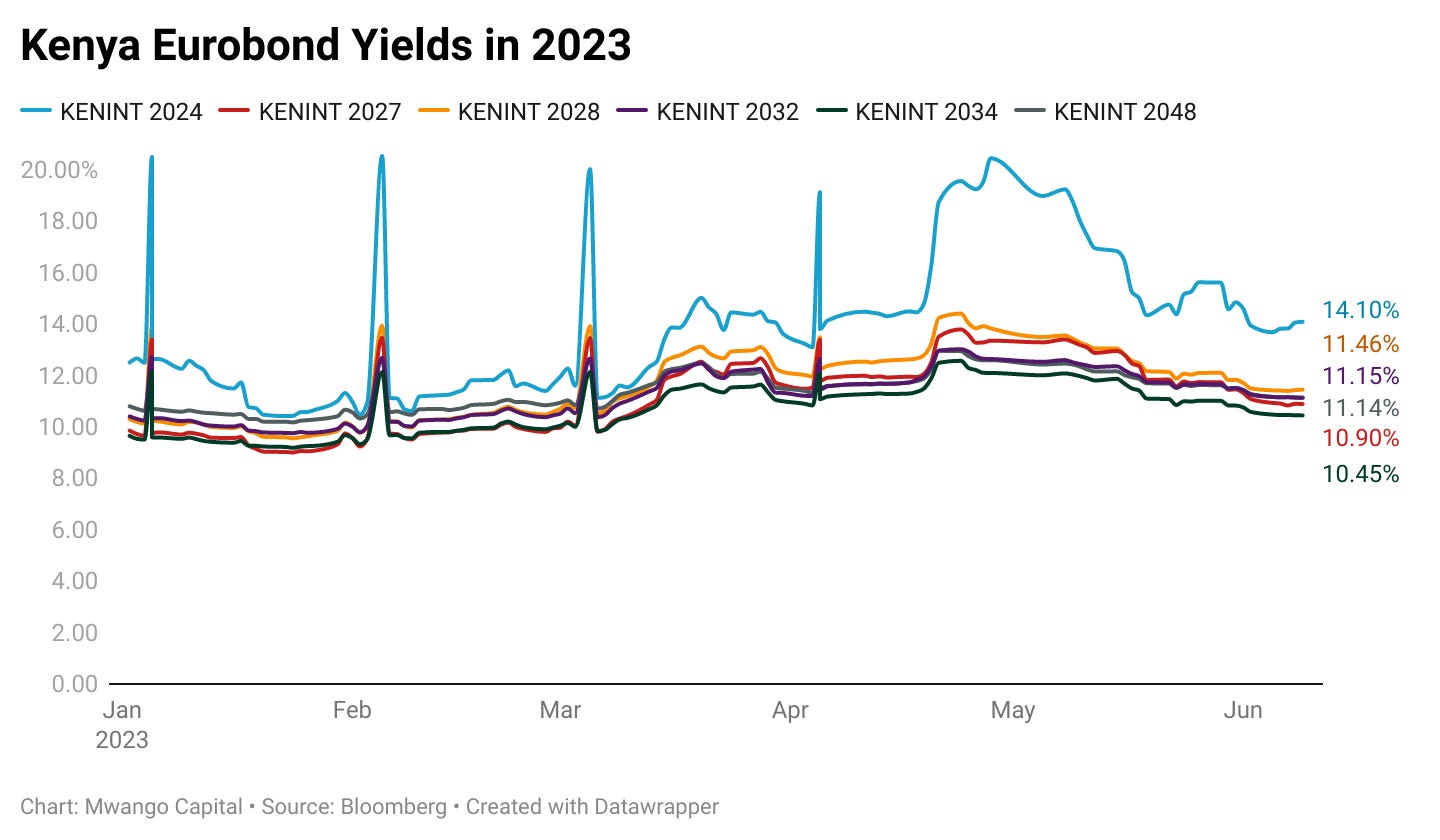

Eurobonds: Last week, all yields except KENINT 2024 fell across the 6 outstanding papers.

KENINT 2024 yield was up by 14.5 basis points to 14.5%, while KENINT 2027 led losses, falling 19.3% to 10.897% and 11.145%, respectively. On average, yields were down 8.3 bps week-on-week.

All yields were up on a Year-To-Date (YTD) basis. KENINT 2024 led the gains at 149.3 bps, while KENINT 2048 appreciated the least, by 31.5 bps, and the average increase was 91.48 bps.

KENINT 2048 led price gains week-on-week, rising by 1.3% to 75.82, respectively, while KENINT 2024’s price was flat at 93.28 On a YTD basis, with the exemption of KENINT 2024 which was up 0.8%, other prices fell, with KENINT 2034 leading price losses at 4.9% to 73.733.

Market Gleanings

🗳️ | Equity To Seek ESOP Approval | In its AGM slated for 28th June 2023, Equity Group is set to table resolutions for the consideration of the establishment of an Employee Share Ownership Plan (ESOP), the reorganization of the Group corporate structure by the establishment of a non-operating holding company to oversee the Group’s technology-related investments, and the incorporation of a subsidiary to exclusively undertake general insurance business in Kenya. On the ESOP plan, Equity will be seeking approval to give a greenlight to the creation of a maximum of 198,614,463 ordinary shares at a unit price of KES 0.5, aggregating to 5% of the issued share capital.

💰 | IFC, MIGA Investment in Safaricom Ethiopia | The IFC this week announced equity investment totalling $157.4M in the Global Partnership for Ethiopia BV - the Special Purpose Vehicle that facilitated the entry of Safaricom into Ethiopia. Additionally, the IFC is set to extend an A-loan amounting to $100M to Safaricom Ethiopia, a move set to carve out a minority position for the IFC in Safaricom Ethiopia, and consequently dilute/impact the existing shareholding structure. The Multilateral Investment Guarantee Agency (MIGA) is set to provide 10-year guarantees of $1B to cover the equity investments of Safaricom Ethiopia shareholders including the Vodafone Group, Vodacom, Safaricom, and British International Investment.

"IFC is delighted to announce its support to Safaricom Ethiopia, the first private sector-led telecoms operator in the country, and its parent company the Global Partnership for Ethiopia. Through this investment, we hope to help the company create a competitive market for mobile connectivity, reflecting our strategy to increase competition in the digital sector globally and reduce costs for consumers."

IFC Vice President of Industries, Mohamed Gouled

📈 | NMG Share BuyBack | Nation Media Group’s Board of Directors has recommended a minimum price of KES 20 per ordinary share in its proposed buyback scheme to purchase up to 10% of its issued share capital (~19,029,516 shares). The shares targeted in the current proposal are 1.7M lower than those targeted in the 2021 share buyback, which resulted in an 82.5% uptake (~17.1M shares).

👨🏽💼 | Kamau Thugge Nomination Approved | Parliament’s Departmental Committee on Finance and National Planning this week recommended that the National Assembly approve the nomination of Dr. Kamau Thugge as CBK Governor. Dr. Patrick Njoroge, who has now served for two terms at the helm of the Apex Bank is set to exit on 17th June 2023.

“Having considered the suitability, capacity and integrity of the nominee, and pursuant to sections 13(1) and 13C of the Central Bank Act, sections 3 and 8 of the Public Appointments (Parliamentary Approval) Act (No. 33 of 2011), and Standing Order 216(5) (f) of the National Assembly Standing Orders, the Departmental Committee of Finance and National Planning recommends that the National Assembly approves the nomination of Dr. Kamau Thugge, CBS as Governor of the Central Bank of Kenya.”

National Assembly, Finance and National Planning Committee

🛍️ | Companies Stockpiling Inputs | The Stanbic Bank Kenya PMI for May 2023 indicated that input prices rose at the sharpest record in May on the backdrop of a weaker shilling and higher fuel prices. The headline PMI stood at 49.4, below the 50.0 neutral mark, albeit an increase from 47.2 recorded in April 2023.

“Input prices are now at their highest since the survey began in 2014 as the shilling depreciated further, which increased import costs. Inventories of inputs continued to grow modestly, as firms looked to keep unused items in case of further price rises and supply shortages.”

Stanbic May 2023 PMI

⚠️ | Profit Warning | Longhorn Publishers, whose share price is down 15% this year, has issued a profit warning for the financial year ending June 2023. This means shareholders should prepare to see at least a 25% YoY drop in net profit:

“The underlying reasons for this decline in performance are rising costs including cost of paper which has increased by over 75% in the last 12 months, currency depreciation, lifting of the interest rate restrictions in the second half of the financial year, shrinkage of consumer wallets arising from the rising cost of living and general slowdown in business during the election period.”

Longhorn

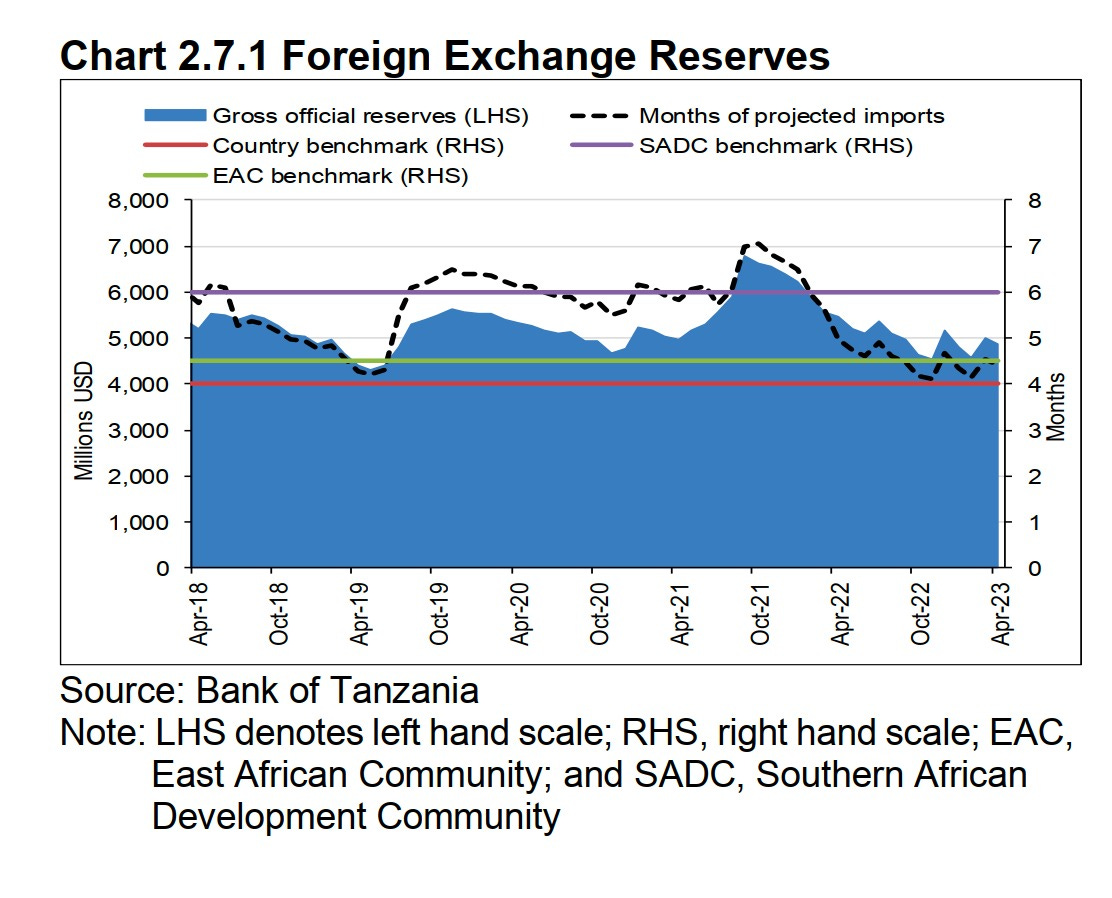

💲 | Tanzania’s Forex Reserves | As of the end of May 2023, Tanzania’s foreign exchange reserves stood at $4.9B, down 11% YoY. The Bank of Tanzania, last week, came out to reassure the public that the reserves were sufficient to cover import requirements for the next 4 months and remain above the East Africa convergence zone criteria. Barely two weeks ago, the BoT issued new forex directives that came into effect on 1st June 2023, and key among them was forex transactions in excess of $1M per transaction in the retail market to be traded within the interbank FX market prevailing quote prices.

“I, first of all, admit that there is a shortage of foreign exchange, but this has been caused by external factors, which are beyond the control of many countries...There is a decline in foreign exchange reserves in the country, however, that is not a crisis, as the level of reserves remains sufficient to cover four months of imports.”

Economic Research and Policy Director Central Bank of Tanzania, Dr. Suleiman Missango

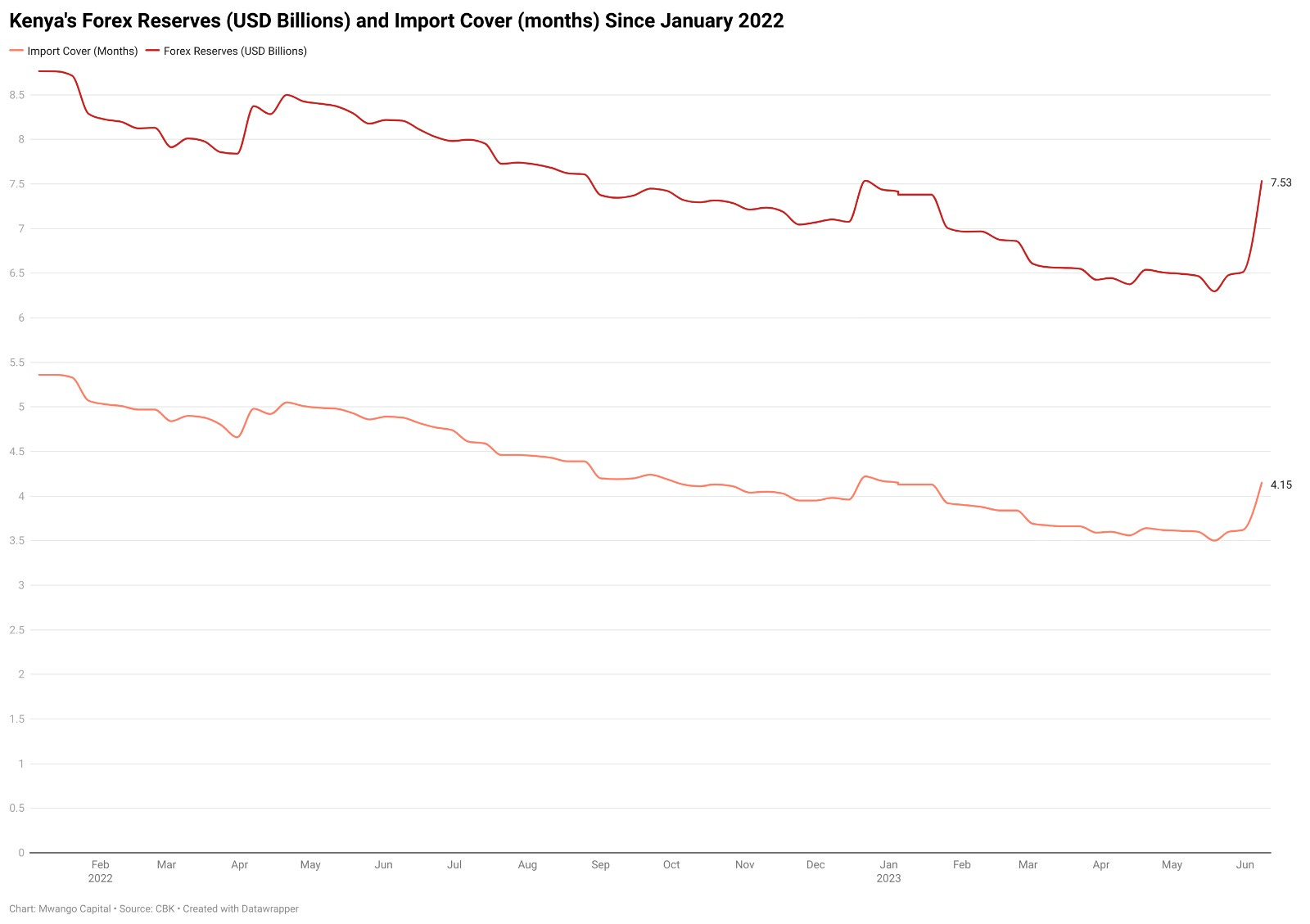

Charts of the Week