2024 at a Glance

The market saw impressive performances across its indices

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a summary of key capital markets and business news items from East Africa.This week, we cover key themes from 2024, Kenya Airways' resumption of trading, and Sasini's FY 2024 results.2024 at a Glance

NSE Performance: In 2024, E.A. Portland Cement Co. Ltd and Kenya Orchards Ltd were the top gainers, closing at KES 30.60 and KES 70.00, reflecting increases of 282.50% and 258.97%, respectively. Conversely, Standard Group Plc and Nation Media Group Plc saw significant losses, closing at KES 5.02 and KES 14.40, with declines of 35.14% and 28.18%, respectively. The market saw impressive performances across its indices, with the NSE All-Share Index up by 34.06%, the NSE 20-Share Index rising by 33.94%, the NSE 10-Share Index climbing by 43.50%, and the NSE 25-Share Index increasing by 42.96%.

“The year 2025 holds the promise of stability, with no seismic shifts anticipated in the economic or investment space. However, it is shaping up to be a year of strategic positioning as frontier economies become increasingly attractive. With interest rate cuts in developed markets, we foresee a surge in foreign activity driving gains in large-cap stocks, particularly those with global exposure.

This momentum is likely to be reinforced by a gradual shift from fixed-income assets to equities, as the era of “free lunches” in fixed income fades. That said, opportunities in the fixed-income space will persist, especially as rising demand for equities drives stock prices higher, making entry positions more challenging. Conservative investors, in particular, may still find value in the secondary market, leveraging pockets of stability.

Ultimately, 2025 will be a year where entry positions play a critical role in determining overall profitability. Coming off a high base of very good returns in 2024, investors will need to be selective and tactical to maximize gains in this evolving landscape.”

Standard Investment Bank Senior Associate Research, Stellar Swakei

Inflation: Kenya's annual inflation rate rose for the second consecutive month in December 2024, reaching 3%, up from 2.8% in November, but remaining at the lower end of the central bank's target range of 2.5% to 7.5%. Inflation in 2024 showed a marked decline across key indices. Food inflation steadily decreased, while Transport costs fell sharply, turning negative by October due to lower fuel prices. Housing and utilities experienced the most significant relief, dropping from 9.7% in January to -0.2% in December. However, Alcoholic Beverages and Tobacco remained relatively stable, with inflation hovering around 7% toward the year-end.

“I think the economic outlook for Kenya in 2025 will be mixed, partly due to countervailing impetus from fiscal and monetary policy, with real GDP growth likely to come in similar to 2024 at 4-5%. I expect the government to continue its efforts to rein in the budget deficit despite pressures from higher interest costs, which will weigh on economic growth. On the other hand, the decrease in inflation and interest rates should boost both private consumption and capital investment. A focus for the government and the CBK will be to maintain FX reserves at their current elevated levels to support a shift in the WB/IMF assessment of Kenya's debt-carrying capacity back to 'strong' from 'medium' at present.”

REDD Intelligence Senior Credit Research Analyst, Mark Bohlund

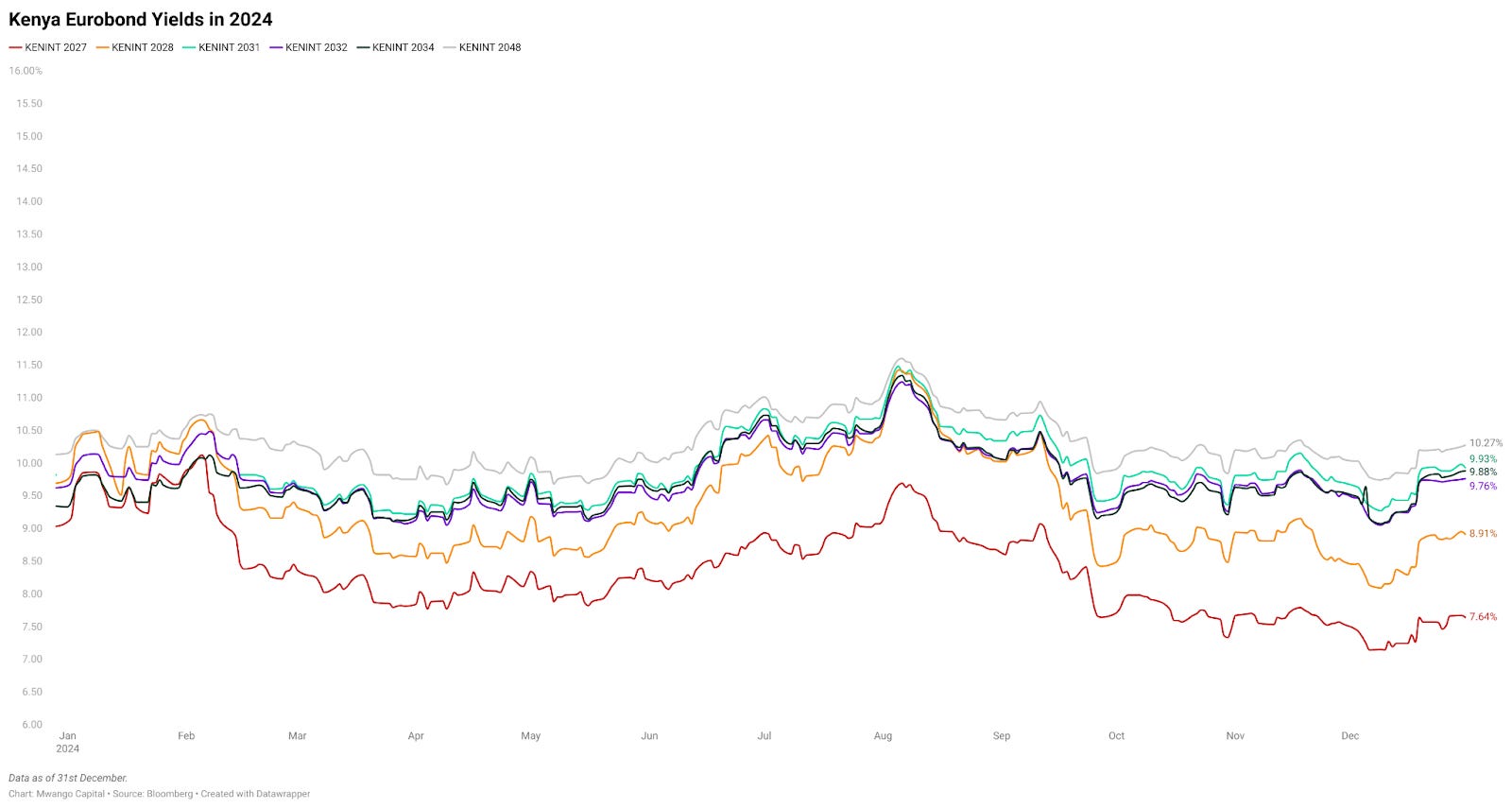

Eurobonds: In 2024, yields on Kenya's Eurobonds showed mixed movements across maturities. Shorter-term bonds like KENINT 2027 and KENINT 2028 experienced notable declines in yields, dropping by 145.40 bps to 7.642% and 83.70 bps to 8.908%, respectively. In contrast, longer-term bonds saw yields increase, with KENINT 2031, 2032, and 2048 rising by 10.90 bps to 9.927%, 11.00 bps to 9.763%, and 12.00 bps to 10.266%, respectively. The KENINT 2034 bond recorded the largest yield gain, up 54.80 bps to 9.878%.

Treasury Bills Yields: Treasury bill yields in Kenya fell sharply in late 2024, driven by successive Central Bank of Kenya (CBK) rate cuts from 13% to 11.25% between August and December. The 91-day T-bill rate dropped below 10% in December, marking its lowest level since April 2023, as returns from government securities tumbled. Earlier in the year, T-bill rates had peaked at highs of 16.72% to 16.99% in March and remained elevated until the rapid decline began in late September. By year-end, yields settled at 9.8252% for the 91-day, 10.0259% for the 182-day, and 11.3711% for the 364-day.

Central Bank Rate: In December 2024, the Central Bank of Kenya (CBK) cut its benchmark lending rate for the third time, bringing it down by 175 basis points over three rate cuts throughout the year, reaching 11.25%. This marked the lowest level in 12 months, following a high of 13% between February 6 and August 5, 2024. The Monetary Policy Committee (MPC) urged commercial banks to reduce their lending rates accordingly, aiming to stimulate credit to the private sector.

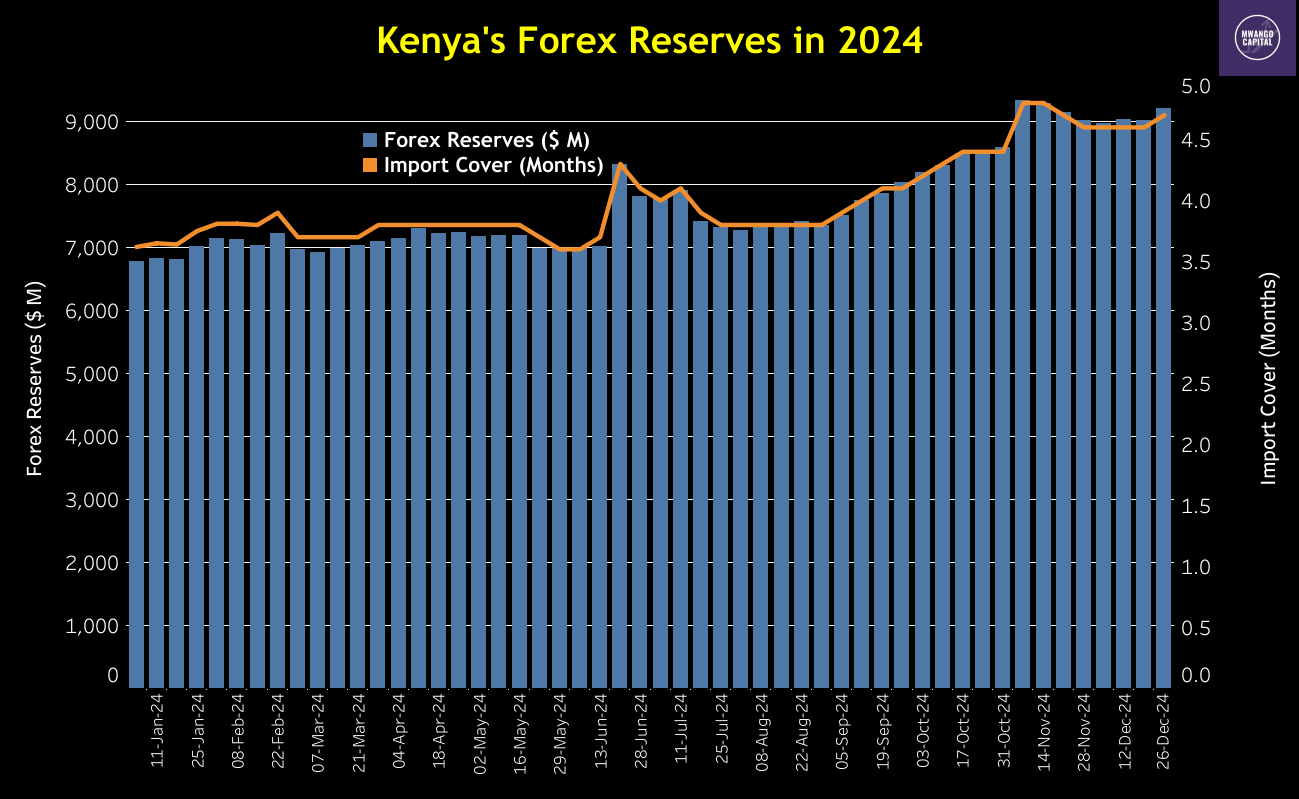

Forex Reserves: Kenya's forex reserves ended 2024 at USD 9.201B, equivalent to 4.7 months of import cover, up from USD 6.775B, equivalent to 3.62 months of import cover, at the beginning of the year. The reserves reached a four-year high in November, peaking at USD 9.323B due to disbursements from the International Monetary Fund (IMF) and net dollar purchases by the Central Bank of Kenya.

Diaspora Remittances: Remittance inflows to Kenya reached USD 423.2M in November 2024, a 19.2% increase from USD 355M in November 2023. Over the 12 months to November 2024, cumulative inflows rose by 16.7% to USD 4,872M, up from USD 4,175M during the same period in 2023. The United States continued to dominate as the largest source of remittances, contributing 53.4% of the inflows in November 2024.

Fuel Prices: Fuel prices in Kenya steadily declined in 2024, with petrol dropping from KES 212.36 in December 2023 to KES 176.29 by December 2024, diesel from KES 201.47 to KES 165.06, and kerosene from KES 199.05 to KES 148.39. The decline was driven by a global fall in crude prices, including a 4.46% drop from USD 641.14 per cubic meter in October to USD 612.53 in November. However, diesel rose 5.76% to USD 643.69, and kerosene increased by 1.87% to USD 660.30. The government also extended its fuel import deal with three Gulf oil firms in December, aiming to shield the shilling from weakening and ensure supply continuity.

Interbank Rate: The average interbank rate in Kenya rose to 12.98% in 2024, up from 9.76% in 2023. Rates peaked at 14.31% on January 2, following the Central Bank of Kenya’s (CBK) December 2023 rate hike. However, with subsequent CBK rate cuts, interbank rates eased, closing the year at around 11%.

USD/KES Exchange Rate: The Kenyan Shilling ranked among the top-performing currencies globally in 2024, appreciating by 17.67% from USD/KES 156.50 at the end of 2023. In the third quarter, the Shilling strengthened by an average of 10.1% against the US Dollar, 9.3% against the Euro, and 7.7% against the British Pound. This stability was driven by Central Bank of Kenya (CBK) measures, including Eurobond buybacks and increased US dollar inflows from global lenders.

This week's newsletter is brought to you by The Kenya Mortgage Refinance Company. First-time homebuyer? Confused about repayments? KMRC can help! Get the info you need to navigate homeownership finances with confidence. Learn more: KMRC website.

Kenya Airways Resumes Trading on the NSE

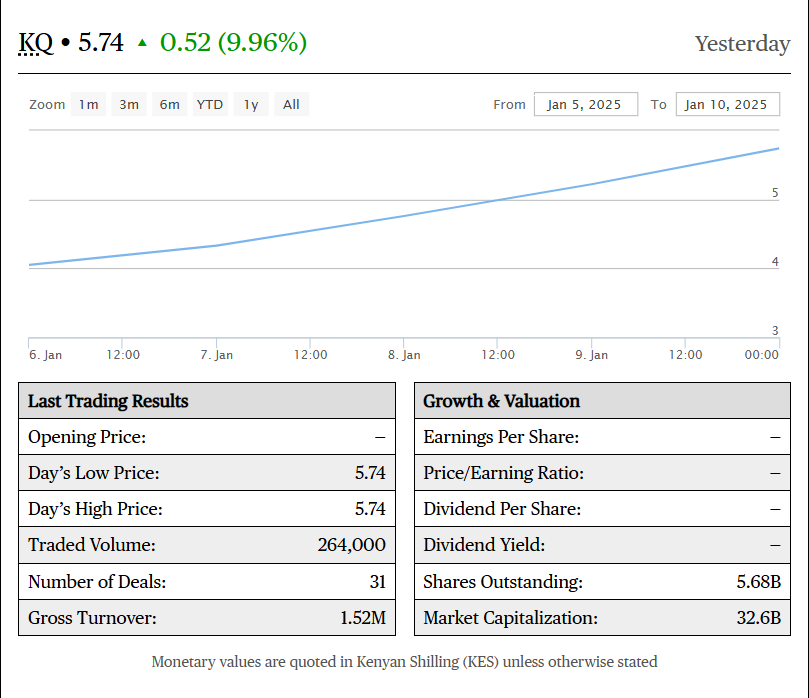

Kenya Airways (KQ) has resumed trading on the Nairobi Securities Exchange (NSE) after a four-and-a-half-year pause, following the Capital Markets Authority’s (CMA) decision not to renew the latest year-long suspension. The markets regulator cited the airline’s improved financial performance and the National Aviation Management Bill 2020 withdrawal, which proposed nationalizing the carrier. This decision follows KQ's return to profitability in H1 2024, posting a net profit of KES 513M, marking its first profit in a decade.

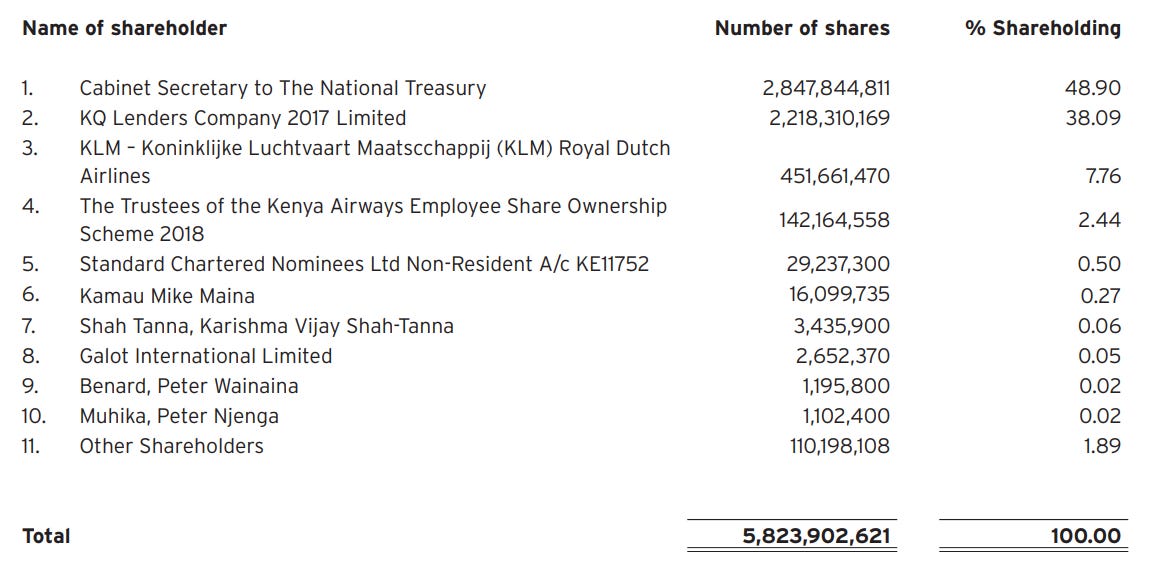

KQ Shareholding: The Kenyan government remains the largest shareholder in Kenya Airways with a 48.9% stake, followed by KQ Lenders 2017 Ltd., a banking consortium, holding 38.09%. Dutch airline KLM owns 7.8%, while about 75,000 retail investors collectively control 2.8%. The airline’s recovery has been driven by restructuring, including the government’s conversion of KES 88B in foreign currency debt into long-term local currency loans. Additionally, KQ issued a 6.5-year KES 19.3B bond to KQ Lenders 2017 Ltd. as part of its financial turnaround efforts.

Share Price Performance: Kenya Airways shares last traded on the NSE at KES 3.83 per share in July 2020. Following the resumption of trading, the company ended the week as the top gainer, closing at KES 5.74, up 49.9%.

Markets Wrap

NSE This Week: In Week 2 of 2025, Kenya Airways led the top gainers, rising by 49.9% to close at KES 5.74, while EA Portland Cement was the worst performer, dropping 10.4% to close at KES 27.50. The NSE 20 rose by 2.7% to 2,145 points, while the NSE 25, NSE 10, and NASI indices gained by 0.8%, 0.2%, and 2.6%, closing at 3,511.3, 1,338.2, and 129.6 points, respectively. Equity turnover rose by 392.7%, totaling KES 2.7B, while bond turnover rose to KES 30B, up from KES 6.6B the previous week.

Treasury Bills: Treasury bills were oversubscribed in the week with an overall subscription rate of 138.10%, up from 65.4% the previous week. Investors placed bids worth KES 33.1B, out of which KES 24.5B was accepted, resulting in an acceptance rate of 73.8%. Yields on the three treasury bill tenors continued to decline, dropping by 23.2 basis points, 0.1 basis points, and 3.7 basis points, closing at 9.5935%,10.0253%, and 11.3342% for the 91-day, 182-day, 364-day bills.

Market Gleanings

🔺| Sasini PLC FY24 Results | Sasini PLC reported a 20.6% rise in revenue to KES 6.9B in FY24, driven by increased sales, though the cost of sales surged 45.1% to KES 6.3B, squeezing margins. The company recorded a net loss of KES 562.9M, reversing a profit of KES 542.6M in FY23, largely due to declines in coffee and avocado profitability amid global price volatility. Net finance income plunged by 97% to KES 6.3M However, total assets grew by 54.5% to KES 25.18B, with equity reserves benefiting from revaluation gains on leasehold land and other assets.

⚓| Mombasa Port Sees 14% Growth in 2024 | The Port of Mombasa processed 41.1 million tonnes of cargo in 2024, a 14.1% increase from 35.98 million tonnes in 2023. Uganda remained the top transit destination, handling 8.8 million tonnes, up 23.8%. Notably, transshipment traffic soared by 132.9%, with 491,666 TEUs processed. Container traffic surpassed two million TEUs for the first time in over a decade, rising 23.5% to 2.01 million TEUs. Overall, the port’s total cargo throughput reached 3.75 million tonnes in December 2024.

✔️| CAK Approves Buyout of KK Security | The Competition Authority of Kenya (CAK) has granted unconditional approval for Canadian entrepreneur Stephan Crétier's buyout of Doctor No Parent Limited. The company, operating in Kenya through GardaWorld Limited (trading as KK Security Limited), provides a range of security services including manned guarding, facilities management, canine security, VIP protection, and cash-in-transit.

📄| Kenya Ratifies OECD's Tax Evasion Convention | Kenya has ratified the Organization for Economic Cooperation and Development (OECD)'s multilateral convention on base erosion and profit shifting, aimed at combating international tax evasion. Set to take effect on May 1, the convention will update bilateral tax agreements, reduce opportunities for tax avoidance, and offer mechanisms for resolving tax disputes.

📊| SSA's Economic Growth Outlook | Sub-Saharan Africa's economy is expected to grow by 4.2% in 2025, up from 3.8% in 2024, driven by investments in energy, infrastructure, and services, according to Moody's. The region's credit outlook was upgraded to stable, as fiscal consolidation helps reduce debt, despite political and environmental risks. However, challenges like inflation and political instability could threaten stability.

💰| Nock Requests KES 1.5B to Begin Loan Repayment | The National Oil Corporation of Kenya (Nock) has formally requested KES 1.535B from the Ministry of Energy to start repaying its KCB loan of KES 7.53B. This loan, initially taken over a decade ago for expansion and operations, had increased due to penalties and interest from ongoing losses. Nock has allocated KES 1.215B of the amount for the first payment, the remaining KES 320M will go toward Nock’s recurrent budget for the fiscal year ending June 2025.

🇪🇹 | Ethiopia's Stock Market Debut| Last week, Ethiopia launched its first stock exchange with Wegagen Bank as the sole listing, but with no IPOs or brokers yet. This marks a milestone in economic reforms aimed at reviving growth after a two-year civil war. The exchange is part of broader efforts, including currency floating, opening the banking sector to foreign investors, and a planned 10% stake sale in Ethio Telecom.

📊| Stanbic Kenya PMI | Stanbic Bank Kenya's PMI fell slightly to 50.6 in December 2024 from 50.9 in November, marking a third consecutive month of private sector growth. The expansion was driven by increased output, new orders, and marginal employment growth, supported by improved customer purchasing power and effective advertising. Input costs rose at the fastest pace in 11 months due to currency weakness, higher taxes, and robust input demand, with agriculture and manufacturing sectors seeing the highest price inflation.

🔴| PCF Extends Xplico Insurance Oversight and Payment Moratorium | The Policyholders Compensation Fund (PCF) has extended the statutory management of Xplico Insurance Company to March 7, 2025, along with a three-month moratorium on payments to policyholders and creditors. Initially implemented in December 2023, these measures aim to safeguard stakeholder interests and enable restructuring under a High Court directive issued on December 10, 2024.

🛢️| S. Sudan Resumes Oil Exports | South Sudan has resumed oil production and export from Blocks 3 and 7 in Upper Nile State, targeting an initial output of 90,000 barrels per day. This follows the lifting of a year-long force majeure by Sudan, which had halted the transport of crude oil to the Red Sea due to ongoing conflict. Oil accounts for 90% of South Sudan’s GDP, and the suspension had disrupted its ability to access international markets for 11 months.

Chart of the Week