KCB Assets Up 54%

Consolidation of DRC-based Trust Merchant Bank grew assets to KES 1.9T

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we continue our coverage of half-year results from banks and other companies.First off, enjoy a dose of our weekly business news in memes.

This week's newsletter is brought to you by:

Co-operative Bank of Kenya. Fuel up the convenient way with your Co-op Bank ATM card. No need to carry cash at the pump; just tap, pay and go. Make your trips smoother, faster, and cashless at NO extra cost.

Click below to see available card discounts.

KCB Total Assets Rise by 54%

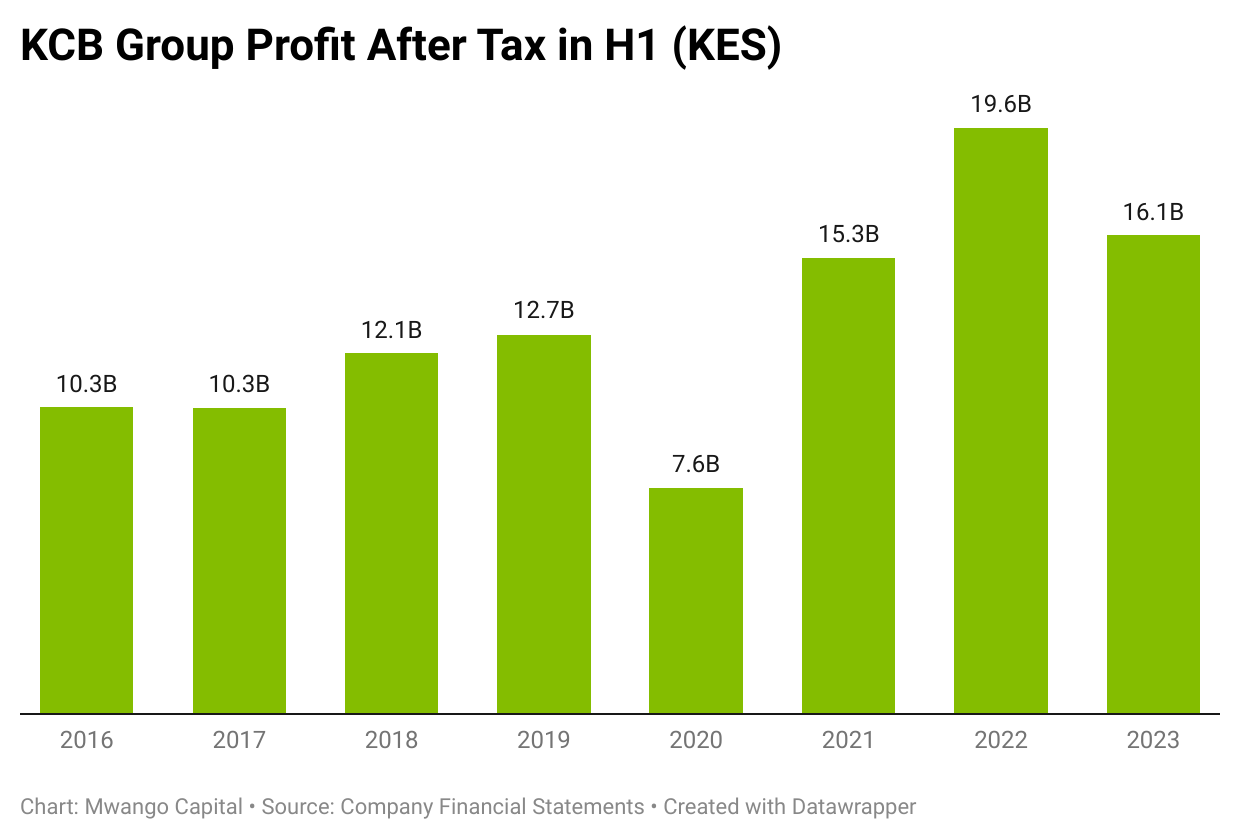

KCB Group reported an 18.3% decline in profitability for the half year ended June 2023 to KES 16.1B as EPS closed at KES 9.71 (-20.1% y/y). Group total assets closed at KES 1.9T (+54.1% y/y). No interim dividend was declared.

Balance Sheet Grows 54%: The consolidation of the DRC-based Trust Merchant Bank acquired in December 2022 and a 61.9% rise in customer deposits to KES 1.5T grew total assets to KES 1.9T (+54.1% y/y). The group’s loan book also grew 32.1% y/y to close at KES 964.8B while Kenya government securities holdings grew 27.1% y/y closing at KES 320.3B.

Digital Channels Spur NFI: Group total operating income closed at KES 73.1B (+22.2% y/y) as non-interest income and net interest income grew 43.4% y/y and 12.1% y/y respectively to KES 27.6B and KES 45.6B. Non-interest income was largely propelled by fees & commissions income from digital transactions which grew twofold to KES 12.3B. In contrast, FX trading income grew 19.8% y/y to KES 5.9B while fees & commissions income from loans grew by only 5% y/y to KES 5.6B. Net interest income on the other hand was driven by interest income from loans and government securities - which grew 33.4% y/y and 14.2% y/y respectively.

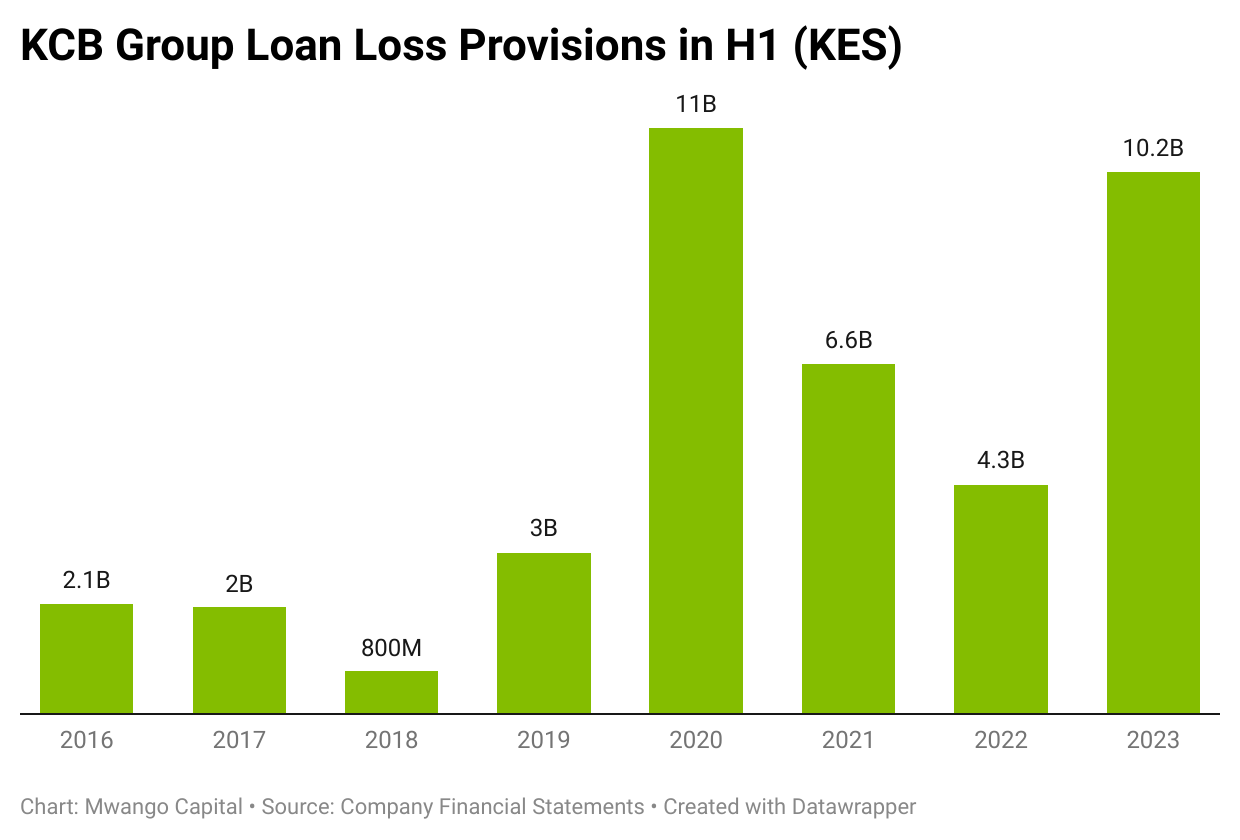

Increased Provisioning: Group profit after tax was down 18.3% to KES 16.1B on the back of a more than two-fold increase in loan loss provisions to KES 10.2B. Profit after tax of the Kenyan subsidiary was also down 15.6% y/y to close at KES 13.9B.

“Profit after tax was greatly impacted by aggressive provisioning on facilities in KCB Kenya, inherited legal claims in National Bank of Kenya (NBK) and staff restructuring costs incurred in KCBK and NBK being an investment to right-size the organisations. The Group also prudently raised its loan loss provisions on foreign currency denominated credit facilities on account of a challenging operating environment.”

KCB

Asset Quality Remains a Concern: The group’s stock of non-performing loans (NPLs) rose 4.9% y/y to close at KES 182.0B, translating to an NPL ratio of 17.4% - against the June 2023 industry average of 14.5%. NPL ratios for KCB Kenya and National Bank of Kenya remain elevated at 19.6% y/y and 24.5% y/y respectively. The bank has also revised its NPL ratio targeting between 14% and 16%.

NCBA Profit Rises by 20%, Cuts Dividend

NCBA reported a 20.3% y/y rise in profitability for the half year ended June 2023 to KES 9.3B as EPS closed at KES 5.67 (+20.1%). An interim dividend of KES 1.75 has been declared with book closure and payment slated for 14 September 2023 and 28 September 2023 respectively.

Balance Sheet Grows by Single Digit: Group total assets were up 9.3% y/y on the back of a 16.7% y/y rise in the loan book to 292.4B as Kenya government securities holdings were cut by 0.5% y/y to close at KES 202.3B. Customer deposits were also up 10.3% to close at KES 516.6B as borrowed funds declined by 15.9%.

NFI Slumps: Total operating income closed at KES 31.0B (+7.0 y/y) as non-interest income declined by 2.6% y/y to close at KES 13.8B. FX trading income was notably down 18.4% y/y even as the revenue line remains a sweet spot for other banking peers. Fees and Commissions on loans also grew marginally by 2.9% y/y while other Fees and Commissions grew by 30.4% y/y.

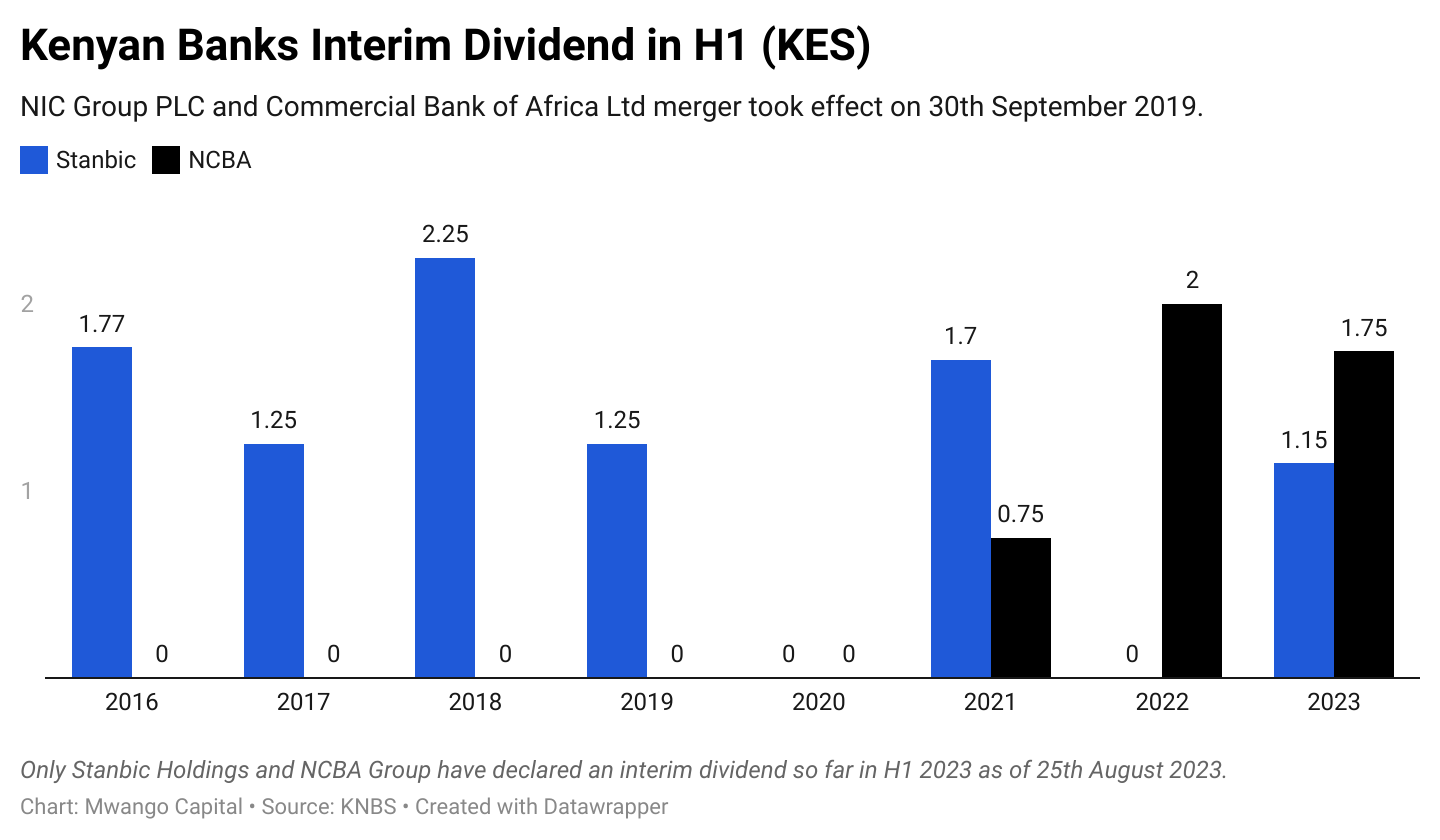

Bucking the Trend: The group cut its loan loss provisions by 21.0% y/y to close at KES 4.4B even as the industry faces high non-performing loans owing to the tough business environment. Stanbic Holdings and NCBA Group are the only two lenders thus far that have reported reduced provisioning in H1 2023 results.

Dividend Cut: The group has declared an interim dividend of KES 1.75, however 12.5% lower than the KES 2.00 payout the prior year. Only Stanbic Holdings and NCBA Group thus far have declared interim dividends for the half year ended 30th June 2023.

Subsidiaries Lift PBT: Tanzania, Rwanda and Uganda collectively contributed KES 1.4B to the group’s profit before tax from KES 178M contributed prior year.

The week also saw Standard Chartered Bank Kenya, Diamond Trust Bank Kenya and I&M Group report their half-year results. We await results from Absa Bank Kenya reporting on 29th August 2023.

Other H1 2023 Highlights

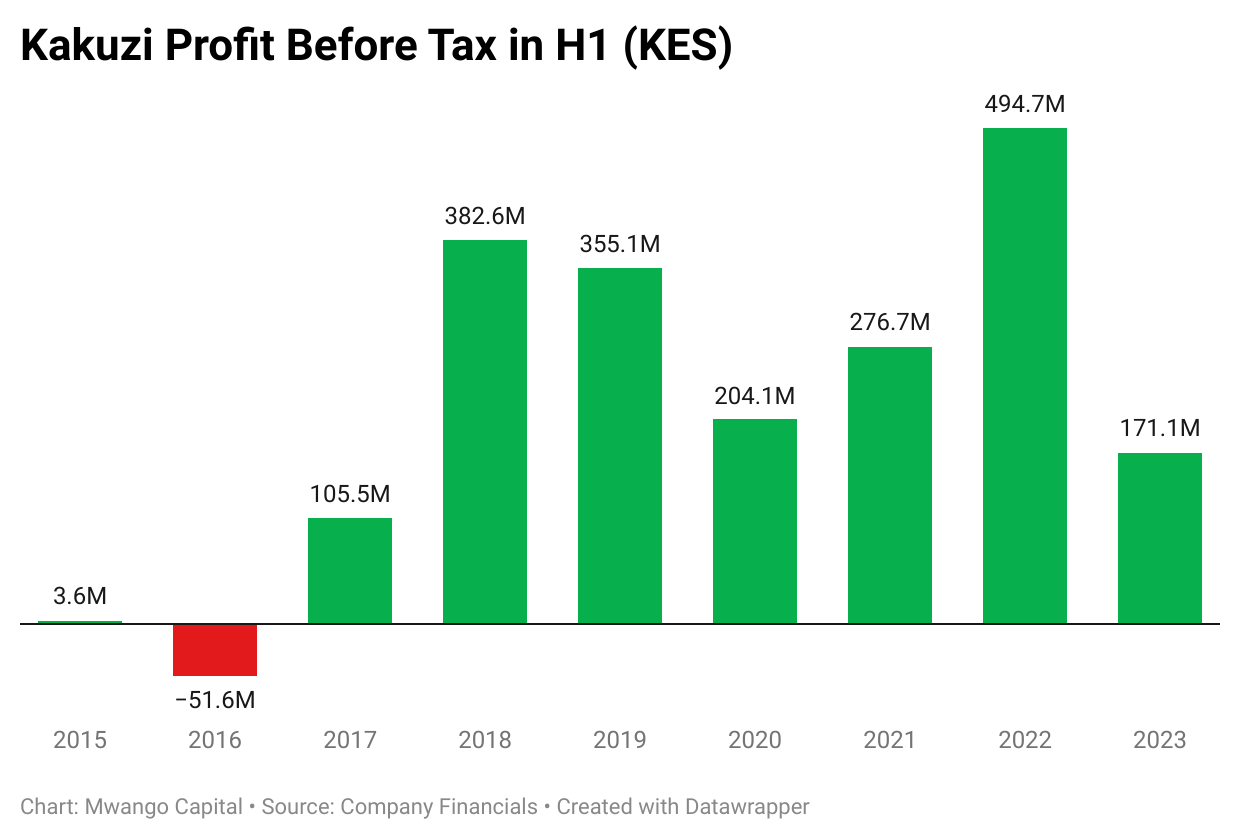

Macadamia Glut Hits Kakuzi: In H1 2023, profit before tax fell by 65.4% year-on-year to reach KES 117.1M on account of depressed performance in the macadamia segment. Due to the global macadamia glut in the operating period, the impact on the group was a KES 329.0M loss, effectively weighing down on pre-tax revenues. In comparison to H1 2022, the macadamia segment brought in profits totalling KES 339.0M. Find the results here.

“The global macadamia glut continues to affect all leading international exporters from Kenya, Australia and South Africa. To mitigate the losses, we have adopted a local marketing strategy geared at availing value added Macadamia products, including ready-to-eat nuts, macadamia flour and cold-pressed oil.”

Kakuzi PLC MD, Chris Flowers

Umeme’s Profit Declines: Despite a 19.9% increase in revenue attributable to an 8.3% increase in electricity sales, the resultant net income declined by 79.5% to KES 13.2B. An interim dividend of UGX 24.0 has been declared with book closure and payment slated for 9th February 2024 and 29th February 2024 respectively. Find the results here.

WPP ScanGroup Loss Widens: Gross profit increased by a marginal 1.9% year-on-year to close at KES 1.1B. Operating and administrative expenses stood at KES 1.5B, up 26.6% or KES 305.0M - out of which 58.2% was on account of a comprehensive restructuring programme undertaken in Q2 2023. FX gains tripled to KES 182.4M as a result of the depreciation of the functional currencies against the US Dollar. Loss for the period widened to KES 124.5M from KES 47.1M prior year. No interim dividend was declared. Find the results here.

Kenya Re’s Premiums Decline: In H1 2023, gross written premiums fell by 10.1% year-on-year to reach KES 9.9B, while net earned premiums fell by 33.5% to KES 6.5B. Net claims and benefits declined by 35.9% to KES 6.5B to account for 64.2% of net earned premium [2022: 66.7%]. The net profit for the period rose by 8.7% to reach KES 904M. No interim dividend was declared. Find the results here.

Bamburi Cement’s Profit Decline: In H1 2023, Bamburi Cement had a number of changes in management, including changes to the Company Secretary and the CEO. In H1 2023 results released in the week, turnover was up 10.6% year-on-year to KES 22.3B. Operating costs grew at 10.5%, about the same growth in revenue, to reach KES 21.8B. Operating profits edged higher by 15.6% to KES 451M, translating to an operating margin of 2.1% [2022: 1.9%]. Net profit declined by 7.4% to KES 88M and the firm did not declare an interim dividend, unchanged from last year. Find the results here.

Boc Kenya Skips Dividend: Revenue in H1 2023 edged higher by 17% year-on-year to KES 589.9M. Earnings Before Finance Income and Taxes was KES 71M, up 35%. Net income rose by 28.9% to KES 50.4M to bring the net margin to 8.5% [2022: 7.7%]. For H2 2023, the firm has pointed out that key concerns include the higher electricity tariffs for industrial customers introduced in April 2023 coupled with the continued depreciation of the Kenya Shilling to the US Dollar. No interim dividend was declared [2022: KES 1.6]. Find the results here.

Standard Group’s Cost Rationalisation: Revenue for H1 2023 decelerated by 8.1% year-on-year to reach KES 1.26B. Operating costs fell by 21.9% on account of cost rationalisation to reach KES 1.3B, outstripping revenue by KES 78M. Net finance costs edged lower by 19.4% to KES 69M, and the net result for the year was an aggregate loss of KES 102.9M [2022: KES 300.2M]. Cash flow-wise, the Group accrued KES 85.1M from financing activities compared to a KES 47M loss in H1 2022. Find the results here.

“The Group has undertaken cost rationalisation measures on operating expenditure, key amongst them being staff costs. This saw total costs decrease by 22% compared to a similar period in 2022.”

Other half-year results during the week included; KMRC, CIC Group, East African Cables, Limuru Tea, and Kenya Orchards.

Markets Wrap

NSE: In Week34 of 2023, Home Afrika was the top-performing stock, up 9.7% to KES 0.34. Williamson Tea was the worst-performing stock, down 15.6% to KES 205.75. The NSE 20, NSE 25, and NASI indices were all down 0.7%, 2.1% and 1.9% to 1,522.5, 2,565.4 and 99.4 points, respectively. Equity turnover was down 72.7% to KES 460M while bond turnover fell by 41.4% to KES 7.7B.

Treasury Bills: The weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day closed at 13.7332%, 13.4911%, and 14.014% respectively. The total amount on offer was KES 24B with the CBK accepting KES 20.4B of the KES 22.9B bids received, to bring the aggregate performance rate to 95.80%. The 91-day and 364-day instruments recorded 455.44% and 21.99% performance rates, respectively.

Treasury Bonds: Across the tap sale issues of FXD1/2023/02 and re-opened 5-Year FXD1/2023/05, the total bids received at face value were KES 17.4B and KES 6.2B, respectively, against an offer of KES 20B. The CBK accepted KES 17.4B and KES 6.1B, bringing the weighted average rate of accepted bids to 16.9% and 17.9%, respectively. The aggregate performance rate was 118%.

Eurobonds: In the week, the yields fell across the 6 outstanding papers this week.

KENINT 2024 fell the most, down by 99.4 basis points (bps) to 12.568%, while KENINT 2048 fell the least, depreciating by 12.0 bps to 11.222%. The average week-on-week change stood at -31.1 bps.

Only KENINT 2024 fell on a Year-To-Date (YTD) basis, depreciating by 3.5 bps. KENINT 2028 led gains at 110.5 bps to 11.417%, while KENINT 2048 recorded the lowest gains at 39.8 bps.

All prices rose week-on-week, with KENINT 2034 rising the most at 1.2% to 73.068. KENINT 2028 rose the least at 0.6% to 85.654. YTD, only KENINT 2024 appreciated, by 3.4% to 95.67, while other papers recorded losses. KENINT 2034 led losses at 5.7% to 73.068 while KENINT 2027 fell the least at 0.7% to 89.301. The average price change week-on-week and YTD was 0.9% and -1.9%, respectively.

Market Gleanings

🍳 | Mama Pima Affordable Edible Oil | The government launched the Mama Pima edible oil dispensing machine initiative aimed at providing affordable cooking oil. The Kenya National Trading Corporation (KNTC) will spearhead the initiative by supplying the oil to vendors at KES 185 per litre, who will then on-sell to consumers at KES 210 - a 13.5% profit margin. Unit prices will be as low as KES 20, and the investment required to become a vendor is KES 185K inclusive of working capital.

👨💼 | Corporate Changes |

Humphrey Wattanga Mulongo has been appointed as the new KRA Commissioner General for a term of 3 years. Previously, he has served as Vice Chairperson of the Commission on Revenue Allocation.

On 23rd August 2023 Safaricom PLC announced the appointment of 2 new non-executive directors, Dr (Eng.) John Kipngetich Mosonik and Murielle Lorilloux to its Board. Dr. Mosonik previously served as the Chief Administrative Secretary in the Ministry of Petroleum and Mining. Lorilloux currently serves as the Chief Strategy Officer at Vodacom Group. The two appointments come after the resignation of Michael Joseph from the board, which took effect on 1st August.

🛑 | Steel Manufacturers Penalized | The Competition Authority of Kenya (CAK) fined 9 steel manufacturers a total of KES 338M for engaging in cartel conduct, including price fixing and output restriction. CAK found that the 9 companies colluded to artificially inflate steel product prices, impacting construction costs. The penalty is CAK’s highest and is meant to deter companies from anti-competitive practices. The CAK is also engaging five other steel firms in settlement negotiations to return effective competition to the sector.

🤝 | Moniepoint acquires Kopo Kopo | The CAK approved the acquisition of 100% shares in Kopo Kopo Inc. by Moniepoint Inc., unconditionally. Moniepoint is incorporated in the USA and doesn't have a Kenya footprint. Kopo Kopo’s 98 employees will retain their employment under the same terms.

🧾 | Twiga Foods Layoffs | Twiga Foods, a leading B2B e-commerce firm announced layoffs as part of a strategic restructuring effort. The firm announced the layoffs were necessary to ensure its organisational structure is fit for purpose in the current economic environment, where the purchasing power of consumers is declining. The company did not disclose the number of employees to be affected but insisted the layoffs were done in full compliance with applicable labour laws.

⚠️ | Uganda Clays Profit warning | Uganda Clays issued a profit warning for the half-year ending 30th June 2023, expecting a loss due to machinery breakdowns which have led to a product shortage. The firm also disclosed that unfavourable macroeconomic conditions, characterised by high inflation and depreciation of the Uganda shilling against the Euro also contributed to the loss. Shareholders and the general public are advised to exercise caution when dealing with the company’s securities.

📱 | Safaricom Ethiopia’s 5M subscribers | Safaricom Ethiopia, a subsidiary of Safaricom PLC has surpassed 5 million subscribers in less than a year since its entry into the Ethiopian market. Safaricom is competing with state-owned Ethio Telecom to dominate the vast market of 112 million people in Ethiopia. In its latest annual report, Ethio Telecom highlighted that it had reached 72 million subscribers.

💵 | Ghana Extends USD Domestic Debt Exchange | Ghana extended the deadline for its US Dollar domestic debt exchange program to August 25th 2023 to give eligible holders more time to secure internal approvals to participate in the program. As of 18th August 2023, eligible holders holding 91% of all eligible bonds had tendered their eligible bonds. The program was launched in a bid to exchange approximately USD 809M of Ghana’s dollar-denominated domestic notes and bonds for new ones.

Charts of the Week