StanChart's Balance Sheet Grows

Loan book grew 8.6%

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover banking Q1 2022 results and the insurance industry.First off, enjoy our weekly business news in memes brought to you by DTB Kenya:

Lending Shores StanChart’s Balance Sheet

Highlights: The loan book grew 8.6% to KES 128B, while holdings of investment securities shrank 9.1% to KES 89.1B. Customer deposits marginally increased by 0.04% to KES 265.3M. The balance sheet expanded by 0.4% to KES 340.9B.

Revenue Mix: Total Interest Income edged up 1.8% to KES 5.6B while expenses were down 23.6% to KES 741M. Net Interest Income (NII) was up 7.2% to KES 4.9B - a 66.4% contribution; while Non Funded Income (NFI) marginally grew 0.08% to KES 2.4B - a 33.5% contribution.

Earnings: Total Operating Income edged up 4.7% to KES 7.4B. OPEX came in 5.4% lower due to deprovisioning and cost-cutting. Profit Before Tax was up 15.6% to KES 3.9B, while Net Income increased by 15.6% to KES 2.7B. EPS was 10.4% higher to KES 6.87 [Mar 2021: 6.22].

Find the results here.

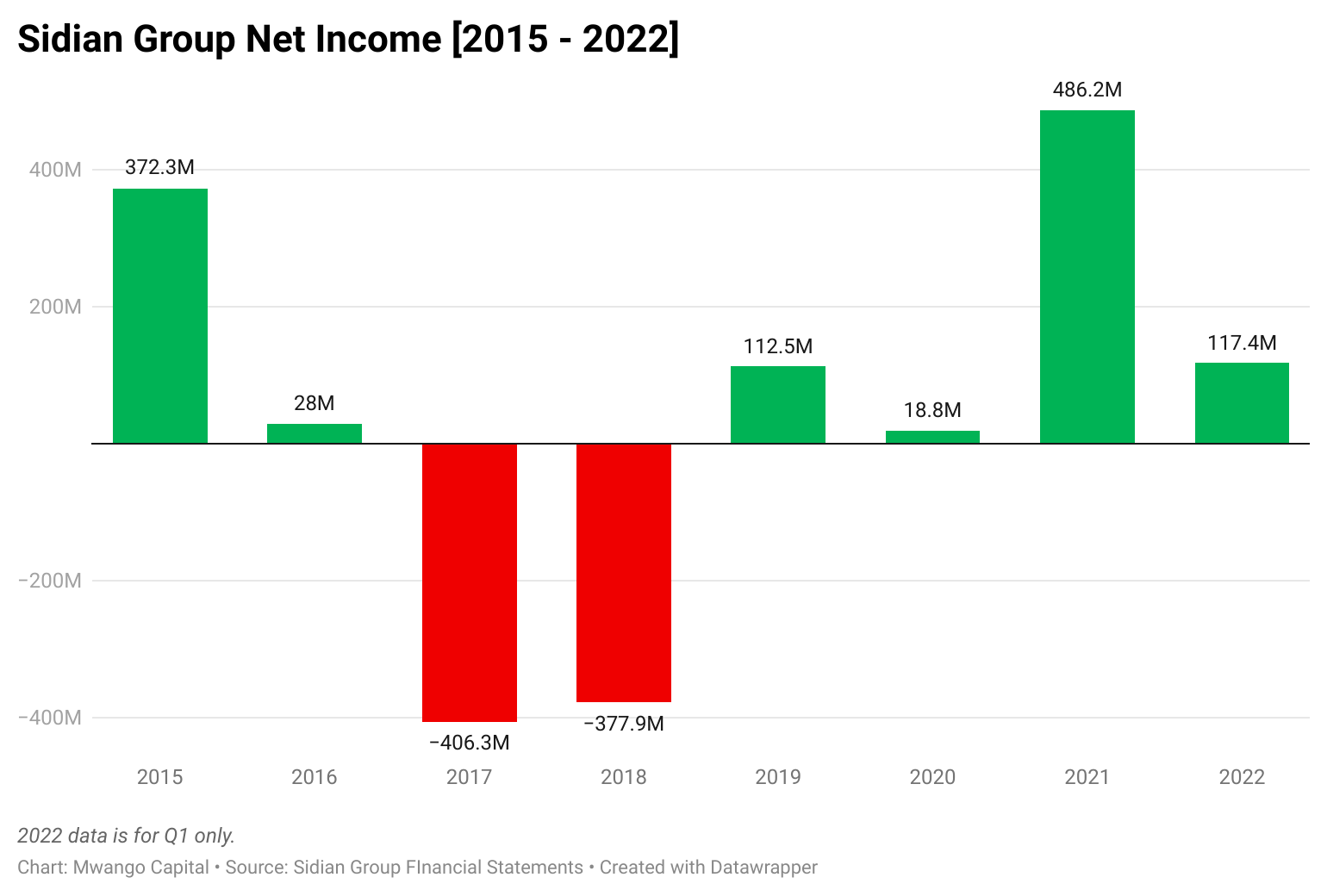

Sidian’s NFI Growth Double NII’s

Banking Business: The loan book grew 13.3% to KES 23.3B but was outpaced by the change in accumulation of government securities which came in 83.2% higher over the year. The Asset Base grew 29.1% to KES 43.1B.

P & L: Total interest income grew 26.3% YoY to come in at KES 970.9M. Net Interest Income grew 9.6% over the year to KES 366.8M to contribute 45.1% to operating income. Non-Funded Income grew by 18.2% YoY, contributing 54.8%.

Bottom-Line: Total operating income grew 14.2% to KES 812.1M, pushing Profit Before Tax higher by 2.9% to KES 176.6M. Net Income grew marginally by 2.9% to KES 117.3M.

Find the results here.

Other Financial Results

Car & General Half Year: Revenue rose 22.5% to KES 10B. EBITDA grew 21% to KES 1.1B to bring Profit Before Tax 14.6% higher to KES 698M. Net Profit edged up 36.6% to KES 629.3M. EPS came in 38.6% higher to KES 7.97, [Mar 2021: 5.75]. The Board of Directors did not recommend an interim dividend.

In Insurance

Allianz Continues Acquisitions: Allianz has completed the acquisition of a 51% stake in Jubilee Holdings Tanzania - its fourth in the region. The transaction adds to previous acquisitions of Jubilee Holdings insurance businesses in Kenya, Uganda, and Burundi.

”The combined strengths of the two brands presents us with a perfect opportunity to further grow the insurance industry in the Tanzanian market. These synergies will go a long way in placing Tanzania on a higher pedestal in as far insurance penetration is concerned.”

Jubilee Holdings Chairman, Nizar Juma

Equity Insurance Line: Disclosures indicate that in 2021, Equity Group invested KES 400M in establishing Equity Group Insurance Holdings Limited - a subsidiary that will run its insurance business.

Madison Property Sale: Madison’s Life Assurance arm is in plans to sell properties valued at KES 8B and quit the annuity business in a move to restructure its balance sheet and boost capital. In FY 2021, its loss for the year widened by KES 352M to reach KES 1B.

What Else Happened This Week

🔙 CDSC Capitulates: The CDSC has dropped its plan to roll out a new KES 100 monthly maintenance fee on all investor accounts. In new delisting rules, companies delisting from the NSE will be required to buy out minority shareholders to prevent them from getting locked in the resultant private entities. [CDSC]

✍️ Tribunal Upholds Penalty: The Tribunal of the Competition Authority of Kenya upheld a determination made by the Authority in May 2020 to levy a KES 2.6M penalty against Royal Mabati Factory Limited on various violations including misleading customers on deliverables. [Business Daily]

💵 Liquidity Mop Up: The CBK was in the markets this week seeking to raise an additional KES 10B after a lackluster performance in the May KES 60B offer. The tap sale on FXD1/2022/10 and reopened FXD1/2021/25 saw CBK receive KES 17B bids, accepting KES 16.9B. [CBK]

📱 M-Pesa Moving Volumes: Total M-Pesa transaction value grew 29.2% to reach $324.6B. The M-Pesa Super App has on-boarded 28 mini-apps with 2.8M users. In Kenya, the ongoing bank-M-Pesa transactions waiver has seen daily transactions reach $15.2B in the previous year. [Vodacom Group]

🧾 Airtel Capitalizes: Airtel Kenya has paid KES 581M [Cumulative: KES 1.7B, Outstanding: KES 1.7B] to the Communications Authority of Kenya for its spectrum licence running from 2015 to 2025. In Uganda, Airtel Uganda has delayed its listing on the USE seeking more time for compliance. [Business Daily]

Interest Rates Watch

South Africa: South Africa's Reserve Bank Monetary Policy Committee increased the repurchase rate by 50 basis points to 4.75% on rising inflation expectations.

Zambia: Monetary authorities in Lusaka held rates steady at 9%.

Chart of the Week

Safaricom, Equity, and KenGen Index is down 25.2% YTD.