Surprise Supplementary Budget

The budget increased total spending by KES 25.03B to KES 4.032T

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a summary of key capital markets and business news items from East Africa.This week, we cover Kenya’s surprise Supplementary Budget III and its rising fiscal deficit risks, as well as Credit Bank’s planned USP listing.Supplementary Budget Raises Eyebrows

Parliament Expands Budget: Last week, Kenya’s Treasury tabled Supplementary Budget No. 3 for FY2024/25, just 11 days before the end of the fiscal year, a move that raises serious concerns around planning, cash flow management, and fiscal oversight. The budget increased total spending by KES 25.03 billion to KES 4.032 trillion, while projected ordinary revenue was revised downwards from KES 2.581 trillion to KES 2.496 trillion. The changes reflect a notable shift toward social and operational spending priorities:

Gainers: The State Department for Social Protection saw the largest increase, up KES 12.46 billion [+35.3%] to fund Inua Jamii cash transfers, while State House received a 44.2% boost [+KES 3.7 billion] to cover operational shortfalls. Crop Development gained KES 9.39 billion, Water and Sanitation KES 3.45 billion, and ICT and Digital Economy KES 2.19 billion.

Losers: Conversely, spending cuts hit Economic Planning (-KES 12.03 billion), Roads (-KES 8.79 billion), Defence (-KES 3.28 billion), and Medical Services (-KES 1.57 billion).

Legislative Sprint: Parliament passed the Finance Bill 2025 by acclamation on June 19, lowering the expected revenue from new tax measures to KES 24 billion, down from the initially proposed KES 30 billion. Lawmakers also fast-tracked the Appropriation Bill, which cleared the committee stage and now awaits presidential assent. These actions cement the fiscal framework for FY2025/26, anchored on a KES 4.291 trillion budget, tighter borrowing conditions, and sustained pressure to boost tax collections. The Finance Bill, Appropriation Bill, and Supplementary Budget III must all be signed into law by June 30, 2025, to meet the constitutional deadline. A good summary of all the happenings last week can be found here. Both Churchill Ogutu and Julians Amboko flag a widening FY2025/26 deficit, driven by weaker revenue outturns and late-stage spending escalations, raising concerns over Kenya’s fiscal credibility:

“Looking at all 3 documents (Finance Bill 2025, Appropriations Bill 2025 & the Mediated Division of Revenue Bill 2025, what's clear is that the numbers are not balancing & 2025/26 will have a notable deficit problem. It's the first time ever that we have seen the Chairpersons of the Budget & Appropriations & that one of the Finance & Planning Committees exchange on the floor of the House over amendments to the Finance Bill & the accompanying revenue trade-off. This is quite telling & begs the question whether we even had the much-touted zero-based budgeting to begin with. Already at KES 933.0B (4.85% of GDP), I expect the 2025/26 deficit to close north of KES 1.0 trillion.”

Business Redefined Host at Nation Media Group, Julians Amboko

“From our assessment, it looks like the FY26 revenue yield may be much lower than the KES 30.0B guidance when the Bill was tabled. Also, the week saw the breakthrough in the counties' equitable revenue share being agreed at KES 415.0B, from the KES 405.1B and KES 465.0B initially backed by the National Assembly and the Senate, respectively. Given the higher counties' allocation, the fiscal deficit is likely to balloon from the KES 923B baseline, compounded by the expected lower revenue yield from the Finance Bill 2025. This week is also packed, ahead of the National Assembly breaking for a short recess after Thursday's session. Most of the heavy lifting has been done around the FY 25/26 spending plan, and the approval of the Appropriations Bill 2025 will be the icing on the cake. We don't expect fireworks along the process. What was surprising (or rather not) was the tabling of FY 24/25 Supplementary estimates last Wednesday, effectively taking FY25 fiscal deficit to KES 997.5B area (5.7% deficit) as signaled by CS Mbadi in the Budget Statement. As usual, the National Assembly will short-circuit this long process into the 4 sitting sessions this week, assuming no major unrest on Wednesday. Nevertheless, the credibility of Kenya's budgeting process keeps being tested with these numerous budget revisions, some introduced with less than two weeks to the end of a fiscal year.”

IC Group Economist, Churchill Ogutu

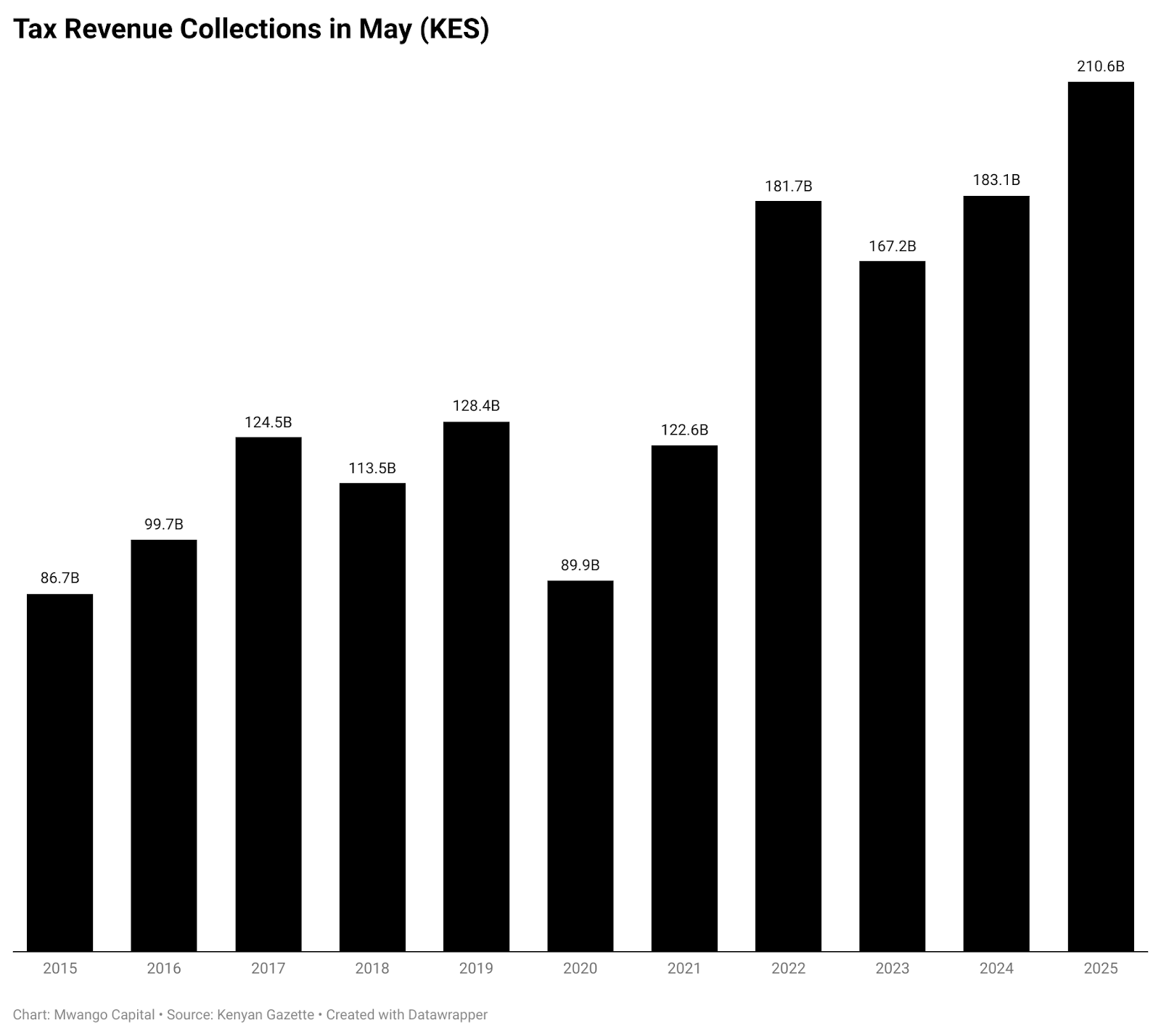

KRA Faces Steep June 2025 Target: Meanwhile, the Kenya Revenue Authority (KRA) collected KES 210.62 billion in May 2025, marking a 15.06% year-on-year increase and bringing total collections for the first 11 months of FY2024/25 to KES 2.01 trillion. To hit the full-year target of KES 2.4 trillion, KRA must raise an additional KES 389.28 billion in June 2025. For context, tax revenue in June 2024 stood at KES 232.2 billion, reflecting a 4.8% year-on-year increase at the time.

This week's newsletter is brought to you by Arvocap Asset Managers, a licensed and trusted investment partner committed to your financial growth. The Almasi Fixed Income Accumulation Fund has recorded a 27.06% cumulative return since inception, driven by strategic investments in government and corporate fixed-income securities. Learn more at www.arvocap.com.

In the Hands of Receivers

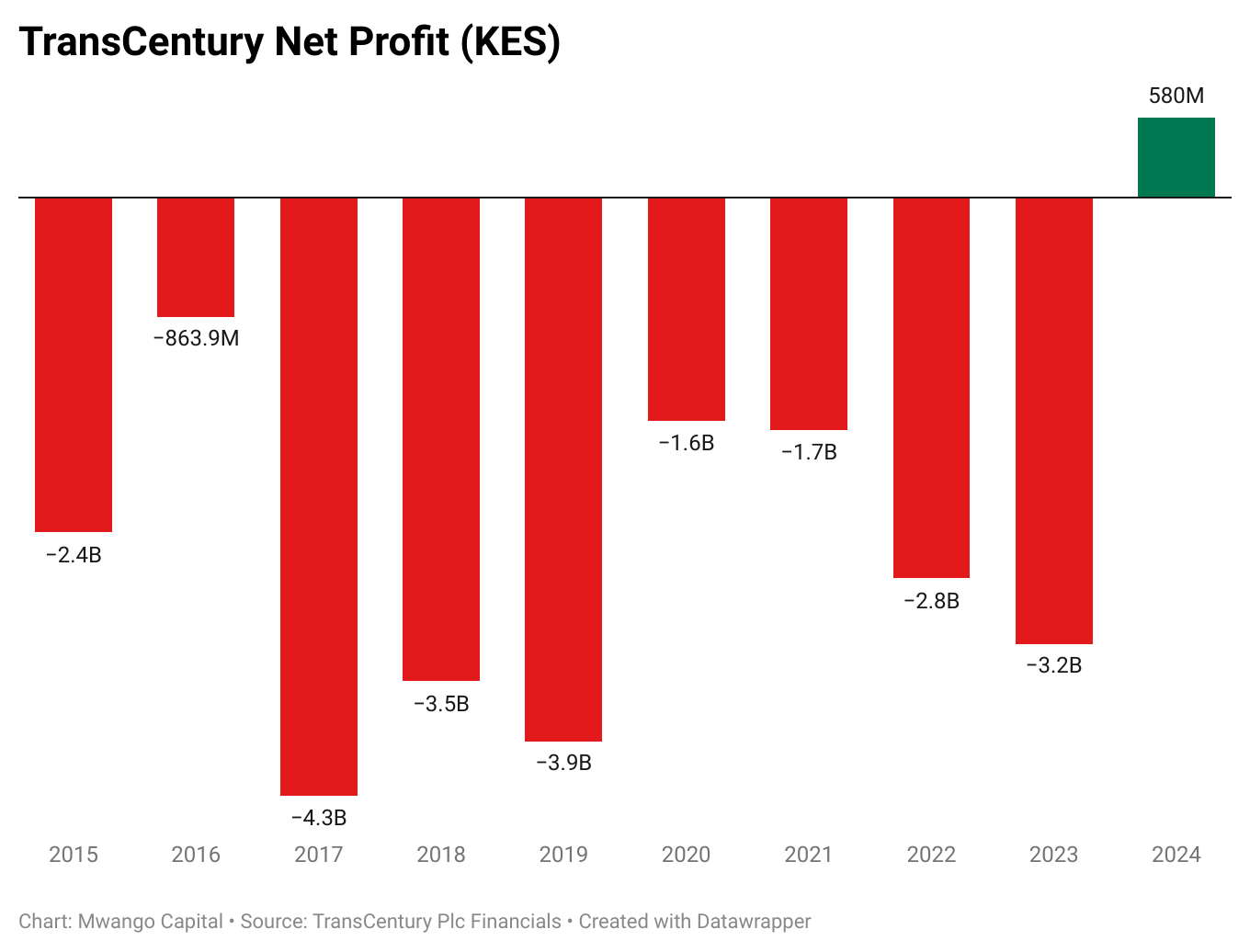

Receivers Take Control of TransCentury and East African Cables: Equity Bank has resumed enforcement action against listed companies TransCentury and East African Cables following the expiry of extended court protections on 18 June 2025. PwC’s Muniu Tihothi and George Weru have formally resumed their roles as Joint Receivers and Joint Administrators, respectively, assuming full control over the companies’ assets and operations. The directors of both firms are now legally barred from conducting any business or dealing with company property without express written consent from the insolvency practitioners.

Court Protections Lapse: The action follows a long-running dispute over a combined KES 4.7B debt, KES 2.8B owed by TransCentury and KES 1.95B by East African Cables. Court orders had paused recovery efforts for two years, giving the group time to restructure and seek investors, including a failed attempt to sell East African Cables Tanzania. With no payment made by the final 90-day extension deadline, the bank has now moved to enforce its rights through receivership and administration.

Stock Soars Despite Receivership: Ironically, TransCentury PLC was the best performing stock at the Nairobi Securities Exchange as of end-May 2025, up 212% year-to-date, while East African Cables had gained 37.96%. The rally followed a surprising return to profitability for TransCentury, which posted a KES 580M profit in FY2024, its first since 2013, on the back of improved gross margins and KES 1.2B in forex gains. The group’s financial rebound has not been enough to stave off creditor action.

Markets Wrap

NSE Week 25 Highlights: The NSE recorded a mixed performance in Week 25 (13–20 June 2025) with the All Share Index dipping 1.3% to 145.7, while market capitalization fell slightly to KES 2.327T. Equity turnover plunged 58.7% to KES 2.46B, with foreign investors accounting for 36.7% of trades. Bond turnover more than doubled to KES 71.3B (+134.4%), lifting the bond index to 1156.88. Express Kenya led gainers with a 30.2% rise, while Umeme slumped 17.6%. Corporate actions this week include multiple AGMs and final dividend payouts from DTB, Equity, and Crown Paints.

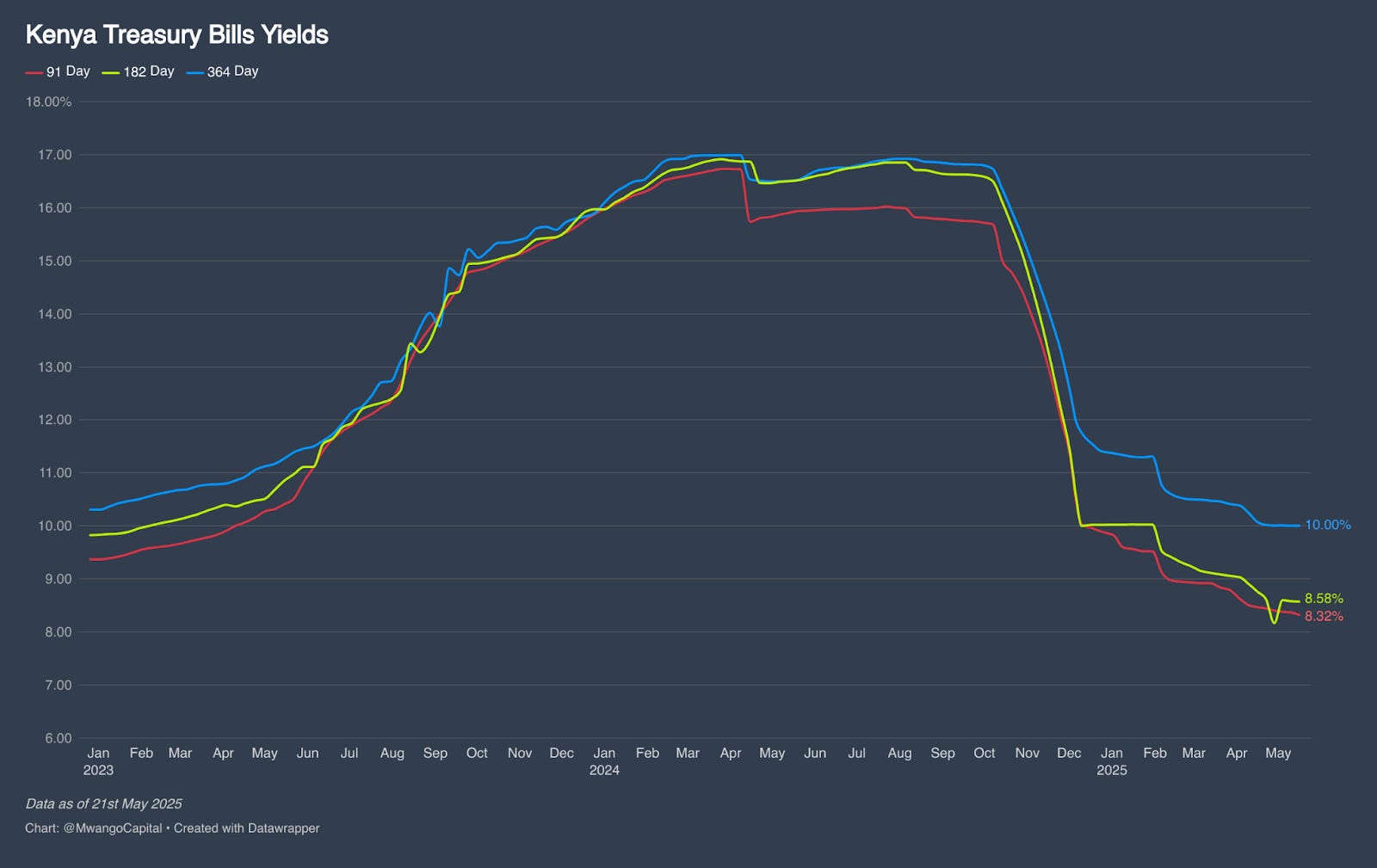

Treasury Bills: Treasury bills were oversubscribed last week, with a subscription rate of 114.15%, down from 237.4% the previous week. Investors submitted bids totaling KES 27.4B, and the Central Bank of Kenya (CBK) accepted KES 24.01B out of the KES 24B on offer. Yields on the 91-day, 182-day, and 364-day T-bills declined by 1.02, 1.87, and 1.12 basis points to 8.1687%, 8.4761%, and 9.7388%, respectively.

Treasury Bonds: The Central Bank of Kenya raised KES 71.64B in net repayments from the June 2025 reopening of two long-term Treasury bonds, FXD1/2020/015 (15-year) and SDB1/2011/030 (30-year). The auction, which sought KES 50B, attracted bids worth KES 101.36B, reflecting strong investor appetite with a bid-to-cover ratio of 1.41. The 15-year bond received KES 84.73B in bids, with KES 57.87B accepted at a 13.49% weighted average rate, while the 30-year bond secured KES 16.62B in bids, of which KES 13.77B was accepted at a 13.998% rate.

Eurobonds: Last week, yields on seven of Kenya’s outstanding Eurobonds increased, led by the KENINT 2034 bond, which rose by 30.60 basis points to 9.83%. The KENINT 2036 bond followed, with its yield up by 21.80 basis points to 10.689%. On average, Eurobond yields rose by 19.39 basis points week-on-week.

Market Gleanings

✈️| KQ Worth More Alive Than Grounded | In an interesting interview this week, outgoing Kenya Airways chairman Michael Joseph voiced frustration over the government's lack of visible support for the national carrier. He argued that despite operational improvements, KQ remains financially constrained and strategically neglected, jeopardizing Nairobi’s role as Africa’s aviation and business hub.

“Kenya Airways is not just a business, it's a strategic asset for the country, but we don't get the support that we need to make sure that we could remain a strategic asset. If we lose this airline, it'll be a tremendous blow to Kenya, not to the shareholders. We are in danger of losing it to Kigali. We already lost it to Dubai to some extent. And if we lose our airline, we lose making this the business capital of Africa.”

Michael Joseph [Source Nation Media Group]

🏦| Credit Bank Seeking Listing | Credit Bank shareholders will vote on a proposal to list the bank’s shares on the Nairobi Securities Exchange’s Unquoted Securities Platform (USP) during its upcoming AGM on July 7, 2025. The move follows a 2023 resolution to demutualize the bank’s shares and is subject to regulatory approvals from the NSE and CMA. In other banking news:

Kenya’s Competition Authority has approved the proposed acquisition of control of Gulf African Bank by Soren Investment Company.

Access Bank Kenya will receive a USD 15 million (~KES 2 billion) capital injection from its parent, Access Bank, after securing regulatory clearance. The update follows Access Bank’s recent acquisition of National Bank of Kenya from KCB Group.

💰| Centum RE Secures Funding | Centum Real Estate has secured KES 2.6B (USD 20M) from the IFC to develop 1,940 affordable housing units at Nairobi’s Two Rivers development, targeting Kenya’s housing gap.

🟢| CBK Extends KEPSS Operating Hours | The Central Bank of Kenya will extend the operating hours of the Kenya Electronic Payment and Settlement System (KEPSS) from July 1, 2025, with transactions now running from 7:00 a.m. to 7:00 p.m. on business days. The move, aligned with the National Payments Strategy, is expected to ease payment processing for businesses and support Kenya’s shift toward a 24/7 digital economy. CBK says the longer hours will improve efficiency, reduce settlement risk, and bring the system closer to global standards in real-time payments.

📄| GCR Assigns Rating to Talanta Sports City Bond | GCR Ratings has assigned an indicative AA(KE)(IR) rating with a Stable Outlook to Linzi FinCo 003 Trust’s proposed KES 44.79B Infrastructure Asset-Backed Security. The 15-year notes, to be listed on the NSE, are backed by monthly receivables from the Sports, Arts and Social Development Fund and will finance the construction of Talanta Sports City. While the structure enjoys moderate government support and liquidity enhancement via a KCB standby facility, the absence of an explicit government guarantee places a ceiling on the rating.

💼| Key Leadership Changes |

Car & General (Kenya) Plc has appointed Nikhil Hira as an Independent Non-Executive Director, replacing Madabhushi Soundararajan, who retires after over 16 years on the board.

KCB Group CEO Paul Russo has been elected Chairperson of the Kenya Bankers Association, succeeding NCBA’s John Gachora. Credit Bank CEO Betty Korir was re-elected Vice Chairperson during the association’s annual general meeting.

🇸🇴| Somalia Sets Up First Securities Exchange | Somalia is set to roll out its first stock exchange, with trading in equities and sukuk bonds expected to begin in early 2026. The National Securities Exchange of Somalia (NSES) will focus on companies in key sectors like telecoms, banking, and agriculture, and aims to improve access to capital while linking Somalia to regional markets. Though privately run for now, the exchange is developing its regulatory framework in coordination with the government.

💸| Remittances Hit USD 440M in May | Kenya received USD 440.1M in remittances in May 2025, a 4.1% rise from April. Cumulative inflows for the 12 months to May reached USD 5.03B, marking an 11.6% year-on-year increase. The U.S. remained the dominant source, accounting for 57% of total inflows.

Chart of the Week