Yields Dip Slightly

IMF's disbursement approval provides relief for Kenya's Eurobond yields

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover Eurobond yields, AfDB's funding, and the domestic debt markets.

First off, enjoy our weekly business news in memes brought to you by EABX Group:

Eurobond Yields Fall Slightly

Loan-rally: The International Monetary Fund last week completed the Third Review under the 38-month $2.34B program approved in April 2021, bringing the total withdrawals from the program to $1.2082B. As a result of this news, yields on Kenya Eurobonds fell from their all-time highs recorded in the week ended July 15. For instance, yields on the 2024 Eurobond, which had spiked to an all-time high of 21.67% on July 14, retraced to 18.08% last week.

Don’t pop the champagne yet: IC Asset Managers Economist, Churchill Ogutu, had this to say:

“This rally was not country-specific, but a number of African Eurobonds also had a decent run in the week. The benchmark 10-year (2032 maturities) across five African names (Kenya, Egypt, Nigeria, Ghana, and South Africa) returned an average of 6.3% w/w. We think the IMF progress gave KENINTs some legs in the week. The IMF Executive Board, finally, approved the disbursement of around $236M this week following the staff mission that completed its work 3months back. This positive development could have given some positive sentiment for KENINTs in the week. But the fact that the positive perf was not isolated to KENINTs, should offer some cautionary tale: investors were broadly risk-on on emerging markets/frontier markets (EM/FM) names against the backdrop of increasingly recessionary fears. Plus, the current setup is the perfect calm before the storm. This coming week, the US Federal Reserve is expected to hike the Fed fund rate by at least 75bps (100bps is becoming the baseline, in light of the hot inflation print) and that by itself should invite some risk-off sentiment on EM/FM names.”

More from the IMF: The IMF has also highlighted a number of developments in Kenya’s macro and fiscal landscape (The report can be found here)

Debt Relief: Kenya was granted relief under the Debt Service Suspension Initiative amounting to $423.5M (KES 46.5B) in H2 2020/21 and $80.3M (KES 8.8B) in H1 2021/22. In total, the relief amounted to $503.8M (KES 55.3B).

Banks Loans vs Eurobonds: The planned FY 2021/22 EUR 1B Eurobond issuance has been replaced by $1.1B in bank loans due to unfavorable market conditions. The syndicated bank loan is assumed to be refinanced by a Eurobond issuance in 2025.

State-Owned Enterprises: The extraordinary cumulative support to SOEs in FY 2021/22 and FY 2022/23 is projected at KES 68.98B or 0.5% of FY 2021/22 GDP:

Kenya Airways: The government is set to implement a restructuring plan which will involve clearing the airline’s debt totaling $868.7M (KES 102.8B) as of March 2022. Over the coming years, the government will novate $485M of KQ’s guaranteed debt.

KPLC: As of June 30, 2021, the power utility had a negative working capital position of KES 69B and is staring at a new liquidity gap of KES 26.3B annually, occasioned by the 15% tariff cut.

AfDB Approves Funding

Highway Loan: The African Development Bank Group (AfDB) has approved $150M funding for the Nairobi-Nakuru-Mau Summit Highway project. The facility will see the transformation of the 175KM A8 Rironi- Mau Summit road into a four-lane carriageway and the maintenance of the two-lane 57.8KM Rironi-Naivasha road.

“One major plus is that this project will improve the extremely poor safety record of the highway which has been identified as one of the most accident-prone in Kenya. In addition, direct development outcomes expected from the project include increased productivity, commercial efficiencies, and time and cost savings. Ultimately this should support economic growth and increase the quality of life of the people.”

AfDB Director General for East Africa Region, Nnenna Nwabufo

Emergency Facility: The bank has also extended a $64.34M loan to Kenya for boosting cereals and oil seeds production by over 1.5MT over the next 2 years. The loan is part of the bank’s $1.5B initiative to avert a looming food crisis exacerbated by the war in Ukraine.

“We are pleased to present the Kenya African Emergency Food Production Facility. Successful implementation of the Facility will see some 650,000 farmer direct beneficiaries, resulting in the production of 1.5 million tonnes of cereals and oil seeds. In all, the Facility will positively impact some 2.8 million people.”

AfDB Vice President for Agriculture, Human and Social Development, Dr. Beth Dunford

Domestic Debt Markets

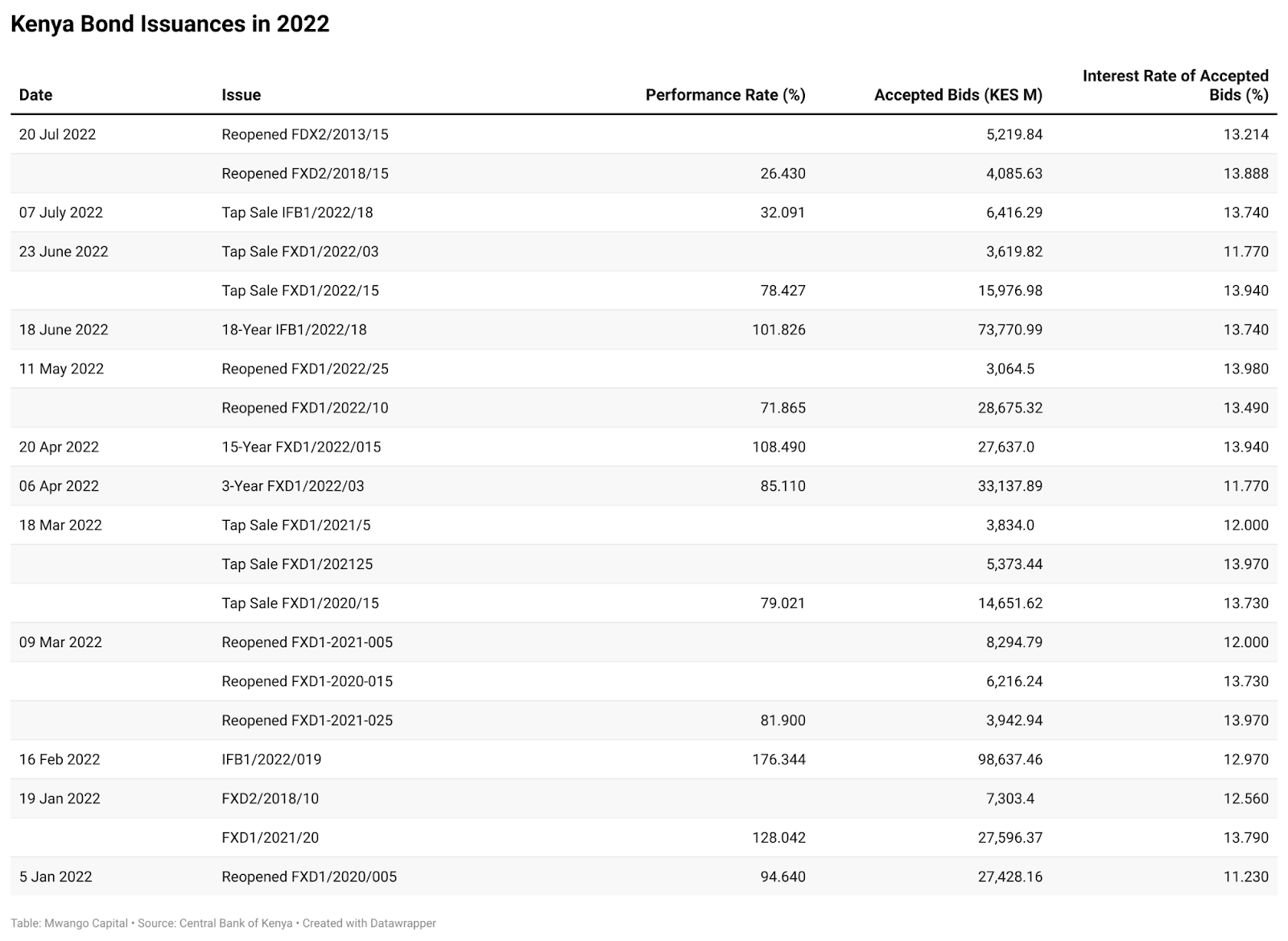

Bond Under-Subscription: In the recent issues of Treasury bonds by the Central Bank, the performance rate for re-opened fifteen-year Treasury bonds FXD2/2013/15 and FXD2/2018/15 came in at 26.43%, with investors placing bids worth KES 10.5B against a KES 40B advertised amount. As confirmed by the slumping performance rates in the auctions, the investor posture towards treasury bonds is weak. Earlier this month, a tap sale on an infrastructure bond, IFB1/2022/18, registered a 32.091% performance rate.

T-Bill Oversubscription: In the gilts market last week, investors piled in on the 91-day and the 182-day papers, with accepted bids coming in at KES 13.4B and KES 14.5B out of an offer of KES 4B and KES 10B, respectively.

Accepted bids on the 364-day paper were KES 2.8B out of KES 10B target. Investors have recently been keeping off longer-dated papers in favour of short-term securities.

The 91-day yield curve rose the most across the 3 papers compared to the last auction, underscoring the shift in time preferences for investors in the domestic public debt markets in the recent issues.

Earnings RoundUp

Earnings Results: 3 companies reported their latest results this past week. These are:

Fahari I-REIT: For H1 2022, rented and related income was up 25.6% year-on-year to KES 171.6M driven by a new anchor tenant at Greenspan Mall. Operating expenses were down 5.8%. Property expenses fell by 8% as they secured withholding tax exemptions for the REIT subsidiaries in Q2 2022. These actions combined pushed net profit up 104.1% to KES 86.1M. Notably, the company is looking to dispose off non-core assets in its KES 3.3B property portfolio, did not make any interim distributions (wait for the full year) and is making an operational restructuring of the REIT.

BAT: For H1 2022, costs rising faster than revenues have constrained operating margins growth. Costs of operations were up 15% year-on-year to KES 14B with gross revenues being up only 7.9% to KES 21.9B. As a result, net income was up 8.4% to KES 2.9B. The firm issued an interim dividend of KES 5 [2021: KES 3.5].

Centum RE: In line with the profit warning the firm issued earlier this month for FY 22, Centum RE reported a drop in profit in full-year earnings, registering a loss of KES 31.9M compared to KES 650M profit in the previous year. Notably, revenues from the sale of residential units tripled to KES 1.85B. Cost of sales jumped 354% to KES 1.5B while operating and administration expenses edged higher by 25%.

Upcoming Earnings: In the coming week, we expect Centum to report on Tuesday, with EABL expected to report soon also. CBK’s MPC meeting is scheduled for this week. Globally, tech companies including Microsoft, Apple, Google, and Spotify are reporting. Also, the Fed is meeting this week and is likely to raise rates.

What Else Happened This Week

⚖️ Suppliers to Sue: Suppliers to public entities are planning to file a class action suit over arrears owed, which constitute a significant share of the KES 574B total outstanding bills. The Association of Public Sector General Supplies (APSGS) has pointed out it will be going to court to seek a legal interpretation of the modalities around the payment of the bills in the context of the upcoming regime change.

“The biggest worry is that most of the new governments are afraid of paying the old bills when they come into the office. This is because of obvious fears like there might have been corruption and this creates a problem for them or if they pay, they may not have money for their own projects.”

APSGS Secretary-General, Simon Gichuki

💸 Food Subsidy: Last week, the government rolled out the 5th Stimulus Package focusing on food subsidies. The highlight was the reduction in the price of unga to KES 100 per 2KG packet from KES 205. To cover their losses from the price cut, traders affiliated with the Retail Trade Association of Kenya are seeking compensation in excess of KES 175M from millers.

🪓 Airtel Splits Money Business: In a maiden move in the sector, Airtel Networks Kenya Limited has separated its mobile money business into a separate unit - Airtel Money Kenya Limited. There has been growing clamor in the country for telecom firms including Safaricom to separate telecommunication and Mobile Money operations.

💰 Insurance Claims Settlement: Data by the Insurance Regulatory Authority shows that GA Life Assurance Limited, Capex Life Assurance, and UAP Life Assurance Company had the highest claim payment ratios in Q1 2022 at 99.4%, 97.5%, and 89.5%, respectively.

🏭 Eni Starts Production: Eni, through its subsidiary Eni Kenya, has begun production at its bio-refineries plant in Makueni. The plant, which was set up early this year, is set to have an installed and expected production capacity of 15K tons and 2.5K tons in 2022.

🏢 Tuskys Building Auction: In a bid to recover a KES 650M loan from Tuskys Supermarket, Equity Bank has put up for auction Tuskys’ five-story building in Nairobi‘s city centre for the second time now. An auctioneer involved in the discussions has placed the agreed amount for sale at KES 700M.

🧾 Gov’t FY 2021/22 Financials: As of June 30, 2022, actual receipts for tax revenue stood at KES 1.78T, with those for non-tax revenue at KES 78.44B. Domestic and external borrowing and grants grossed at KES 877.04B and KES 239.6B, respectively.

💸 Ghana Approves Borrowing: Lawmakers in Accra have approved a plan by the government to seek up to $750M in debt from the African Export-Import Bank for the 2022 budget. The government is looking for up to $1B in loans and plans to finance the $250M using a syndicated facility.

Interest Rates Watch

🇿🇦 South Africa: The Reserve Bank of South Africa hiked rates by 75 basis points to 5.5% - the highest increase in almost 2 decades. The Monetary Policy Committee (MPC) cited currency depreciation and rising inflation in their decision. Annual inflation reached 7.4% in June 2022, breaching the Central Bank’s target of 3% - 6%.

🇳🇬 Nigeria: The Central Bank of Nigeria delivered its second consecutive rate hike last week, increasing the key benchmark rate by 100 basis points to 14%. In its previous interest rate decision, the central bank hiked by 100 bps to 13%. Annual Inflation in June 2022 came in at 18.6%, double the Central Bank’s upper target of 9%.

🇰🇪 Kenya: The MPC of the Central Bank of Kenya is set to deliver its interest rate decision on July 27. The meeting comes against a backdrop of rising inflation that reached 7.9% in June 2022 and a depreciating local unit currently trading at all-time lows (USDKES = 118.71). The Central Bank Rate is currently at 7.5%.

Charts of the Week