Ethiopia's Macroeconomic Reform Program

A $10.7 billion financial package from international partners to support the reforms

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a summary of key capital markets and business news items from East Africa.This week, we cover the major macroeconomic reforms program announced by Ethiopia, BAT Kenya's half-year 2024 results, and President William Ruto’s second batch of nominations to the Cabinet.This week's newsletter is brought to you by The Kenya Mortgage Refinance Company.

First-time homebuyer? Confused about repayments? KMRC can help! Get the info you need to navigate homeownership finances with confidence. Learn more: KMRC website.

Ethiopia Announces Major Market Reforms

Market Reforms: Ahead of today’s IMF meeting on Ethiopia’s request for financial support, the country’s Prime Minister Abiy Ahmed has announced the implementation, with immediate effect, of a much-welcome comprehensive macroeconomic reform program designed to stabilize and propel its economy towards sustainable growth. Key measures include adopting a market-based foreign exchange rate system to address FX distortions, modernizing monetary policy with an interest rate-based framework to control inflation, and enhancing fiscal policies to improve government revenue and manage public debt.

“This macroeconomic reform endeavor which is within the framework of our Home-Grown Economic Reform program and Mid-term Investment and Development Plan (MDIP) is supported by the International Monetary Fund, the World Bank, and other critical development partners…Regarding the key measures and anticipated national benefits and outcomes of the macroeconomic reforms, our economic reform program, supported by the International Monetary Fund, the World Bank, and other significant development partners, is projected to deliver substantial benefits and outcomes to our economy.”

More Details: Supporting these transformative reforms is a $10.7 billion financial package (equivalent to 7% of GDP) from Ethiopia’s international partners, marking the largest coordinated effort of its kind with substantial contributions from the IMF, World Bank, and other multilateral institutions. Here are some of the changes being implemented with immediate effect as noted by the National Bank of Ethiopia.

🌐 Banks will now buy and sell foreign currencies freely with limited intervention from the National Bank of Ethiopia (NBE).

💼 Exporters and commercial banks can retain their foreign exchange earnings, ending the previous surrender requirements to the NBE.

🚫 The foreign exchange market is being liberalized with the removal of import restrictions on 38 product categories, enhancing market accessibility.

🏦 Residents can now open foreign currency accounts for various purposes, including remittance inflows and rental income.

💳 Interest rate caps on borrowing from abroad are removed, encouraging investment by private sector companies or banks.

📈 Foreign investors can now access Ethiopia’s securities market under specified terms and conditions.

🌍 Companies within Special Economic Zones are granted special foreign exchange privileges, including the ability to retain 100% of their foreign exchange earnings.

🧳 The rules on the amount of foreign currency cash notes travelers may carry are relaxed, allowing for more flexibility when traveling in and out of Ethiopia.

🏭 There is significant support for industries that substitute imports, enabling them to scale operations and capture market share.

💸 Ethiopia's attractiveness to foreign investors is improved, enhancing foreign direct investment (FDI) and aligning with international peers to boost economic growth.

🕰️ New policies are being implemented to correct long-standing business practices that caused economic distortions.

Mitigating the Impact: Given the anticipated short-term pain in the economy, the government has introduced temporary subsidies on essential imports and additional financial support for those affected by high inflation. Debt service relief measures are also in place to preserve budgetary allocations for social and capital spending. These sweeping changes mark a pivotal moment in Ethiopia’s economic journey with the government expecting that the successful implementation of these reforms will accelerate economic growth, reduce inflation, and create a more inclusive and prosperous future for all Ethiopians. The crucial question now is what this means for companies like Safaricom that operate in Ethiopia.

BAT’s Revenues and Profits Drop

High-Level Highlights: For the six months ended June 2024, BAT Kenya recorded KES 19.6B in gross revenue, representing a decline of 6.5% year-on-year. Excise duty and value-added tax (VAT) increased by a marginal 0.6% to reach KES 7.9B. Net revenues for the half-year period totaled KES 11.7B, down 10.7%.

The total cost of operations fell by 13.9% to KES 7.9B, bringing the operating profit to KES 3.8B, down 2.9%. The operating margin for the period under review stood at 32.2% [H1 2023: 29.6%]. In the operating period, the Kenya Shilling appreciated by 22% against the US Dollar, which resulted in the firm accruing significant foreign exchange losses that impacted the bottom line.

“The operating landscape was characterised by geo-political disruptions, inflationary pressures and currency volatility. During the period, the Kenya Shilling recorded a significant appreciation (approximately 22%) against the United States Dollar (our exports trading currency) which resulted in substantial foreign exchange losses.”

Net Profit Down 24%: The net result for the year stood at KES 2.1B, down 24.3% year-on-year, bringing the net profit margin to 18.2% [H1 2023: 21.5%]. Per Share Earnings stood at KES 21.36 [H1 2023: KES 28.22]. Finance costs were KES 720M in the period, compared to KES 145M in finance income in H1 2023, and the costs incurred in this period pushed pre-tax profits lower to reach KES 3.1B as compared to KES 4B in H1 2023, a 24.3% decline.

Despite this profit decline, the Board of Directors declared an interim dividend of KES 5.00, unchanged from H1 2023. The interim dividend is payable around 27th September 2024 in line with the shareholders on record as of 30th August 2024.

Find our analysis here and the results here.

Mergers, Deals, and Acquisitions

Bamburi Acknowledges Amsons Offer: Bamburi Cement Plc has received a takeover offer from Amsons Industries (K) Ltd., proposing to acquire 100% of its ordinary shares at KES 65 per share. The total consideration for the takeover is approximately KES 23.6B. This offer represents a premium of up to 85.71% over recent trading prices of Bamburi shares and is subject to regulatory approvals.

According to the offeror’s statement, KCB Investment Bank Ltd, being the transaction advisor and sponsoring stockbroker of Amsons has confirmed that Amsons has sufficient financial resources at its disposal to satisfy the consideration payable for all shares in Bamburi pursuant to a full acceptance of the offer.

KAA-Adani Proposal: Kenya Airports Authority (KAA) has confirmed receipt of an investment proposal from Adani Airport Holdings Limited to upgrade Jomo Kenyatta International Airport (JKIA). The proposal includes constructing a new passenger terminal, a second runway, and refurbishing existing facilities. The proposal will undergo technical, financial, and legal reviews, including stakeholder engagement, National Treasury approval, Attorney General clearance, and Cabinet endorsement.

Faulu Launches MMF: Faulu Microfinance Bank has launched a new money market fund (MMF) to broaden its investment options for customers. The MMF invests in money-market instruments including short-term Government securities, bank deposits, and high-grade corporate securities. The fund comes after the bank recently received a KES 900M capital injection from Old Mutual Group. The Faulu MMF, with an annual yield of 16.32% as of July 18, 2024, allows investments starting from KES 1,000.

Markets Wrap

NSE: In Week 30 of 2024, EA Portland led the market, rising 36.2% to KES 7.30, while Home Afrika was the worst performer, dropping 8.6% to KES 0.32. The NSE 20 fell by 1.6% to 1,674.1 points, while both the NSE 25 and NASI indices dropped by 3.1% and 4.0%, closing at 2,798.5 and 104.2 points, respectively. Equity turnover rose by 27.4% to KES 1.6B, while bond turnover dropped to KES 28.3B from KES 35B the previous week.

Treasury Bills and Bonds: The weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day were 16.00%, 16.85%, and 16.92% respectively. The total amount on offer was KES 24B with the CBK accepting KES 22.9B of the KES 31.65B bids received, to bring the aggregate performance rate to 131.86%. The 91-day and 364-day instruments recorded 645.26% and 16.88% performance rates, respectively.

Government reopens IFBs: The Kenyan government has reopened infrastructure bonds IFB1/2023/6.5 and IFB1/2023/17 to raise KES 50B. Applications are due by August 14, 2024, at 9 a.m. The IFB1/2023/6.5 bond offers a 5.8-year tenor with a 17.9327% annual coupon, paying interest in May and November. The IFB1/2023/17 bond has a 15.7-year tenor with a 14.3990% annual coupon, with interest paid in March and August. Both bonds, available at discounted, par, or premium prices, will have a value date of August 19, 2024, and a minimum investment of KES 50K.

“The reopened bonds are expected to generate significant interest from the market due to recent developments and the attractiveness of infrastructure bonds. I especially foresee higher interest in the IFB1/2023/6.5, which ranks as the third-best bond by returns among all existing bonds. Additionally, given the current interest environment where rates appear to be on an upward trajectory, investors are likely to push for higher yields. Furthermore, higher funding needs than previously anticipated due to the withdrawal of the Finance Bill will likely exert additional pressure on the yields. Consequently, I expect the government to accept bids at a discount, particularly for IFB1/2023/17, which was issued when interest rates were moderate.”

Standard Investment Bank Research Analyst, Stellar Swakei

Eurobonds: In the week, yields were mixed week-on-week across the 5 outstanding papers with KENINT 2028 rising the most, up 11.00 bps to 10.359%, followed by KENINT 2027 at 10.20 bps to 9.029%. KENINT 2031 and KENINT 2048 rose by 4.40bps and 3.50bps to 10.665% and 10.938%, respectively, while KENINT 2032 and KENINT 2034 recorded declines of 1.30 bps and 0.80 bps to 10.450% and 10.525%, respectively. The average week-on-week change stood at 4.50bps.

Market Gleanings

👨🏿💼|Cabinet Nominations | On Wednesday, President William Ruto released his final list of Cabinet nominees following the recent dismissal of his entire Cabinet, except for Prime Cabinet Secretary Musalia Mudavadi. Notably, the President has appointed four members from the Orange Democratic Movement to the new Cabinet, one of whom John Mbadi is the new man at the helm of Treasury.

📉| Kenyan Banks Downgraded | Moody's has downgraded the long-term deposit ratings of KCB Bank Kenya Limited, Equity Bank (Kenya) Limited, and Co-operative Bank of Kenya Limited to Caa1 from B3 primarily driven by the recent downgrade of Kenya's sovereign rating to Caa1. The banks' Baseline Credit Assessments (BCAs) have also been reduced to caa1 from b3, with a negative outlook on their ratings.

“The banks' high sovereign exposure, mainly in the form of government debt securities held as part of their liquid assets, renders the banks' capital, profitability and liquidity vulnerable to a sovereign stress event. In view of these links between sovereign and bank credit risk, these banks' standalone credit profiles and deposit ratings are constrained by the Caa1 rating of the government”

💲| Kenya’s New IMF Program | Kenya is preparing to seek new financing from the International Monetary Fund (IMF) following economic disruptions caused by recent protests that led President William Ruto to reconsider proposed tax increases. Treasury PS Chris Kiptoo announced discussions on a potential new IMF program during a presentation of revised budget estimates, while also engaging with the World Bank for additional development policy financing. The current IMF program, valued at USD 3.6B, is set to conclude in April, with the IMF board expected to approve a disbursement at their August meeting.

Meanwhile, on July 25th, 2024, the National Assembly of Kenya voted to reject the Finance Bill, 2024, following the President’s reservations after the House agreed with the President’s recommendation to delete all the Bill's clauses, leading to its complete rejection. Consequently, there is no Bill for the Speaker to present for presidential assent. Parliament has also adopted the Report of the Budget and Appropriations Committee on its consideration of the Supplementary Estimates I FY 24/25.

💰| Safaricom’s AGM | Safaricom PLC last week held its virtual Annual General Meeting (AGM), where shareholders approved a final dividend of KES 0.65 per share, totaling KES 26.04B for the financial year ending March 2024. Combined with an interim dividend of KES 0.55 per share paid earlier in the year, the total dividend payout reached KES 1.20 per share, equivalent to KES 48.08B.

📄| ILAM Fahari I-REIT H1 2024 Results | For the six months ended June 30, 2024, ILAM Fahari I-REIT reported a 21.3% decline in revenue to KES 140M year-on-year. Other income increased by 50.8% to KES 24.9M, while operating expenses decreased by 0.1% to KES 109.8M. The net profit dropped by 37.4% to KES 53.8M, leading to earnings per share of KES 0.30, down from KES 0.48 in 2023.

💲| Kenya’s Diaspora Remittances | In June 2024, diaspora remittances were USD 371.6M, up 7.4% year-on-year from USD 345.9M recorded in June 2023. Month-on-month, the remittances were down 8.1% from USD 404.4M in May 2024, and for the 12 months to June 2024, the cumulative inflows were up 12.9% year-on-year to USD 4.535B as compared to USD 4.017B in 2023.

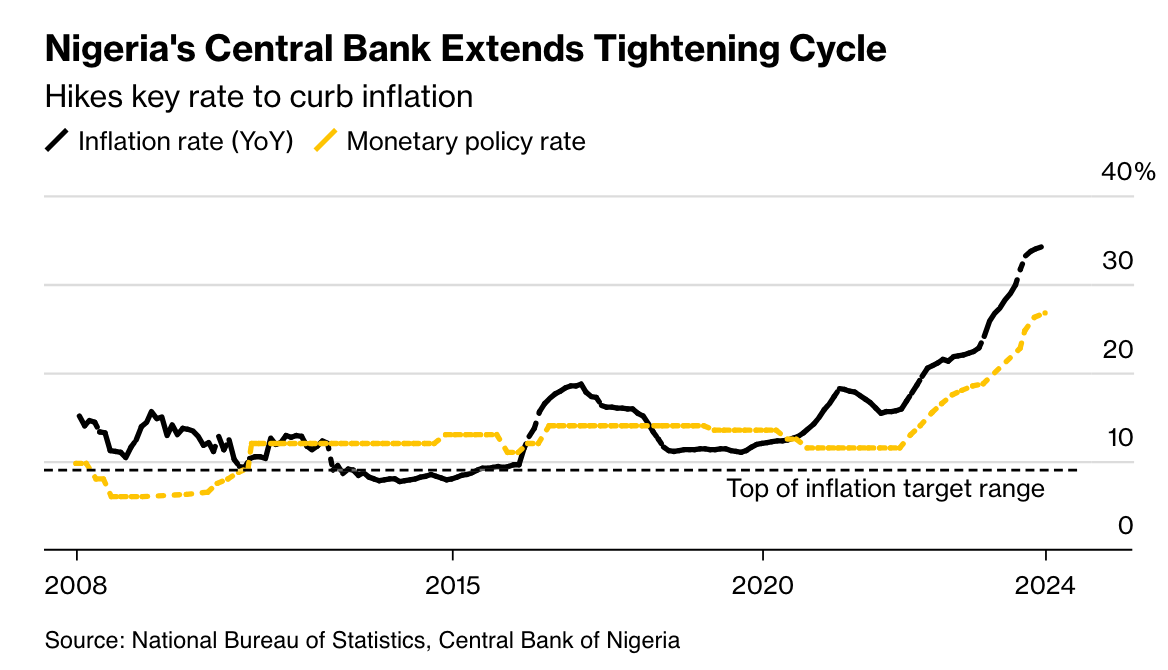

🇳🇬| Nigeria Hikes Policy Rate | Nigeria's central bank has raised its benchmark interest rate to 26.75%, marking the fourth hike this year. Central Bank Governor, Olayemi Cardoso, stated that the increase, up from 26.25%, is crucial to combat inflation, which surged to a 28-year high of 34.19% in June.

Meanwhile, Nigerian lawmakers approved an increase in the tax rate on forex gains for banks to 70%, above the 50% proposed by President Bola Tinubu.

“Today’s downside surprise to the headline policy rate decision comes as the Naira has depreciated considerably in recent months, reversing the appreciation from around 1600 at the first hikes in the beginning of the year to 1100 in end-April. That said, the effective tightening that amounts from today’s decision — given the corridor adjustments — may amount to a significant hawkish surprise to market expectations, if it transmits to upcoming bill auctions”

—Goldman Sachs Analysts

💸| Cameroon Raises USD 550M in Eurobonds | Cameroon has raised USD 550M in Eurobonds, capitalizing on favorable interest rates and heightened demand for African debt. The seven-year Eurobonds were issued on July 23, 2024, at an interest rate of 10.75% through a private placement, facilitated by Citigroup Global Markets Ltd and Cygnum Capital Middle East. This brings to $5.4B the total amounts raised by African countries in the Eurobond markets in 2024 so far.

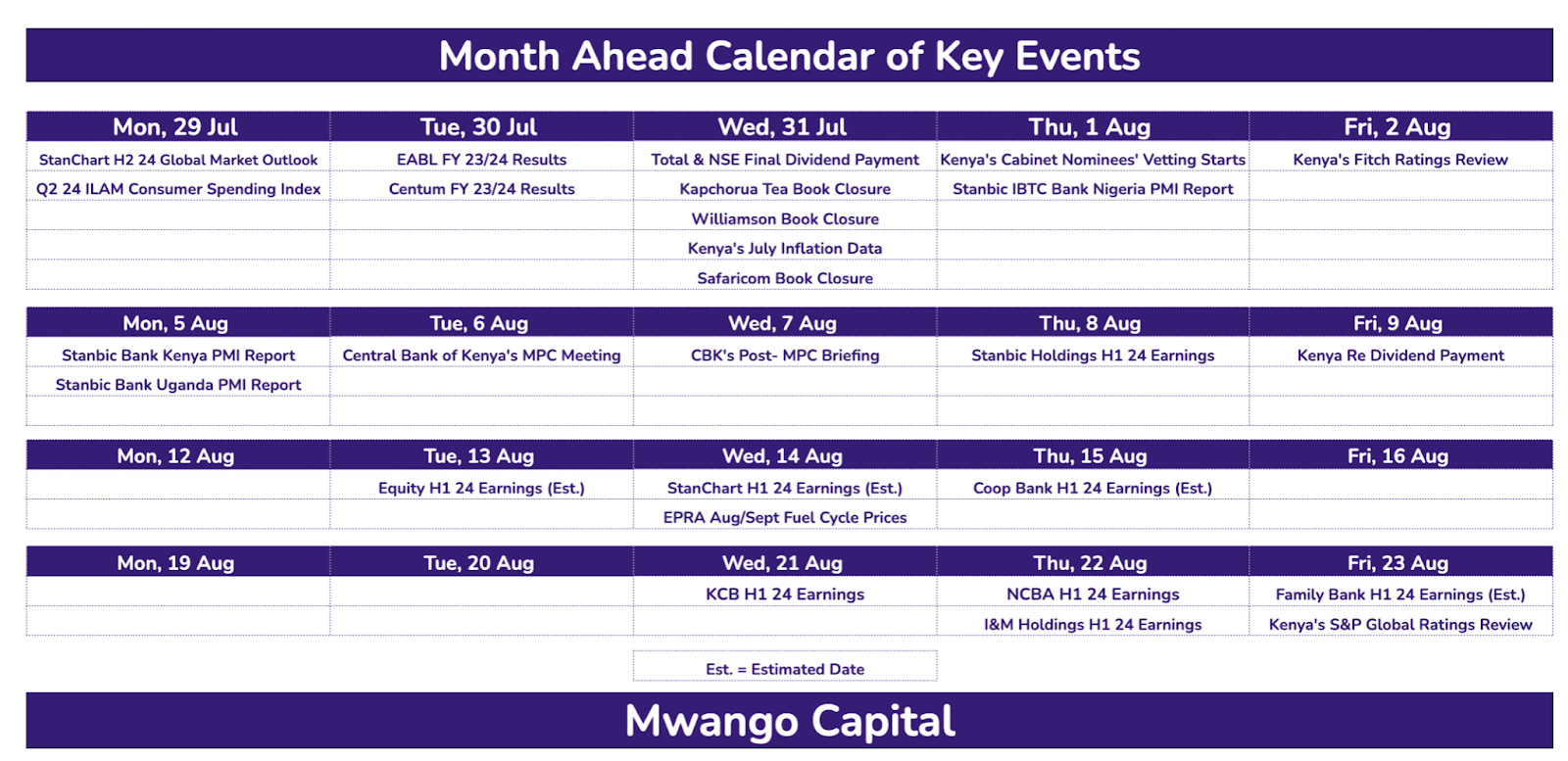

Month Ahead Key Events

Charts of the Week