Cash Rich EABL

EABL reports record profits for H1 2022

👋 Welcome to the Baobab Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover the EABL’s H1 2022 results and Tanzania’s banking sector Q4 2021 results. We also take a look at the FY 2021 results in Tanzania’s banking sector, and profit warnings at the NSE.Our newsletter this week is brought to you by:

Mwango Capital. Mwango Capital provides A+ quality analysis and research on the East African capital markets. Follow us on Twitter, join us on Telegram, check out our website.

If you want to sponsor our weekly newsletter, memes, or Twitter Spaces, reach us at hello@mwangocapital.com.

First off, our weekly business news in memes brought to you by The Shack:

🍻 EABL H1 2022

Kenya boosts sales: Group net sales were up 23% to KES 54.9B realised through strong organic growth across East Africa. Sales in Kenya, Uganda, and Tanzania grew 27%, 18%, and 15% respectively.

2x profit: The Group’s bottom line grew 131% to KES 8.7B driven by an increase in net sales and prudent cost management.

Cash-rich: The company finished the period with a solid KES 7.2B in cash and cash equivalents which was up 185%.

Contribution to Government revenue: Taxes in the form of excise duty and corporate income tax amounted to KES 45B across the region.

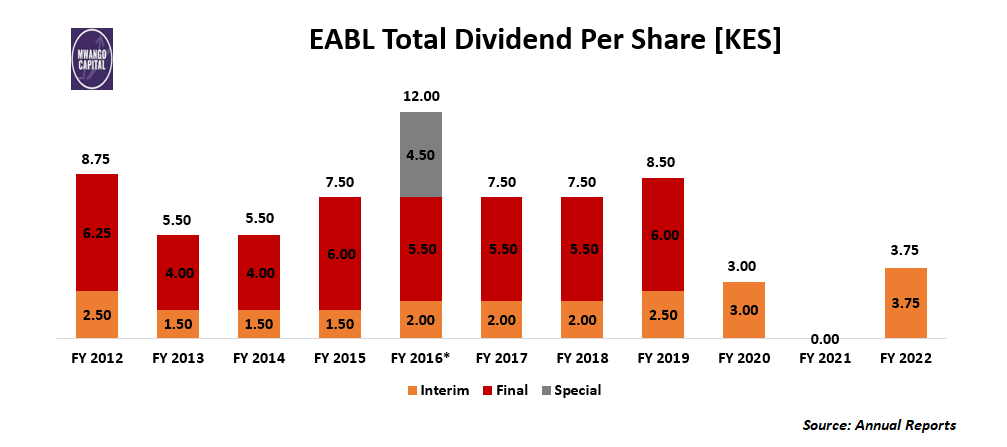

Return to dividend: Following a zero payout in FY 2021 in efforts to conserve cash in the wake of the pandemic, the directors have recommended an interim dividend totalling KES 2.96B (KES 3.75 per share) payable on 27 Apr 2022. Book closure is slated for 28 Feb 2022.

More: Business journalist Julians Amboko sat down with EABL CFO to unpack the earnings. Listen in here.

🏦 CRDB Bank vs NMB Bank (Q4 2021)

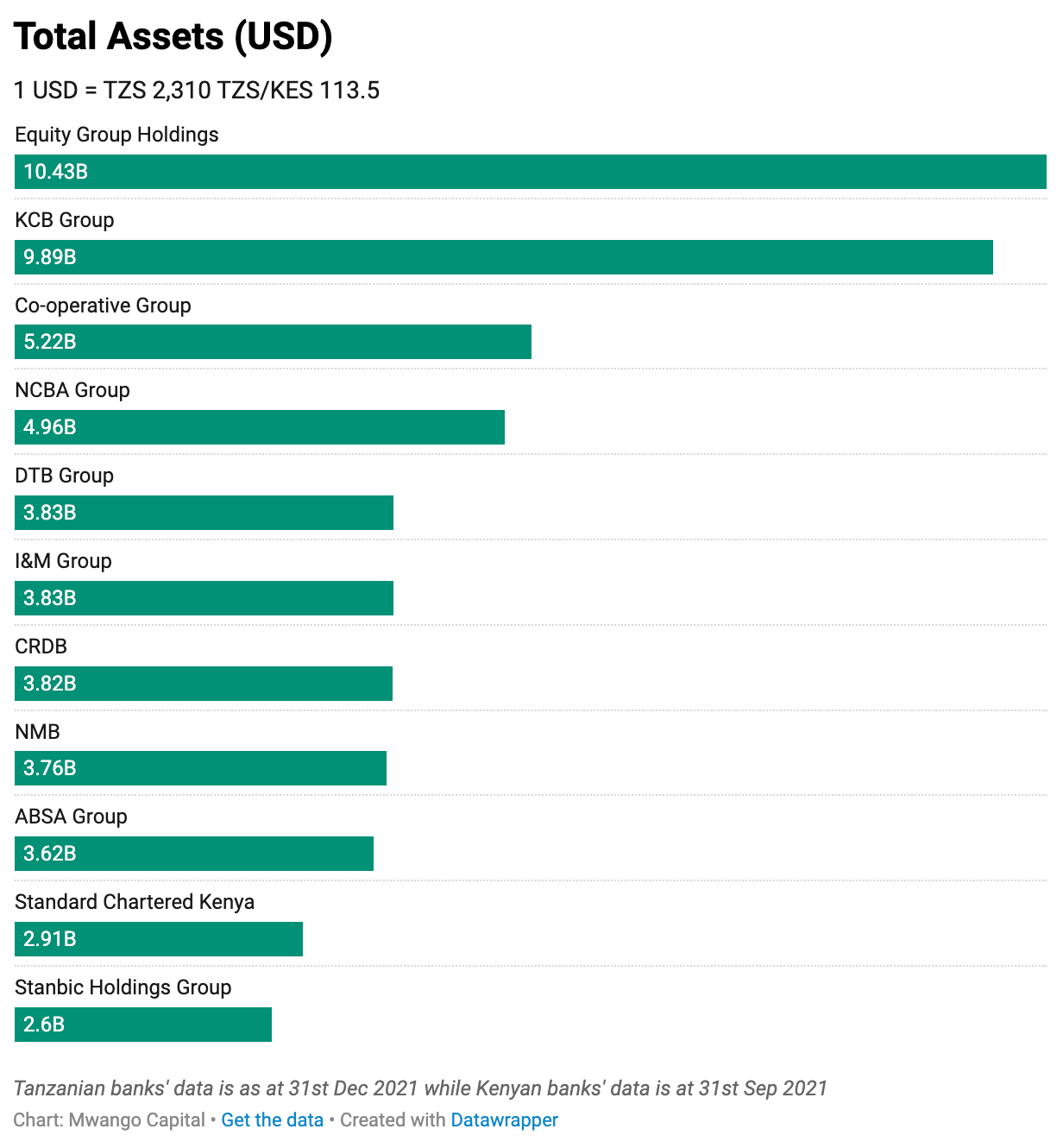

Neck and neck on total assets: CRDB is the largest bank in Tanzania with assets worth TZS 8.8T [USD 3.82B], an 8.5% increase from the previous quarter. NMB comes in at a close second at TZS 8.7T [USD 3.77B], having grown 6.2% in the same period.

How do the top two banks in Tanzania compare to the Kenyan banks?

Loans v deposits: NMB’s loan book grew 4.3% from the previous quarter to TZS 4.7T [USD 2.02B] compared to customer deposits which grew 6.5% to TZS 6.4T [USD 2.79B].

In contrast, CRDB posted a 10.8% growth in its loan book to TZS 5.0T [USD 2.18B] and a 9.2% growth in customer deposits to TZS 6.4T [USD 2.79B].

NMB earned more: NMB returned TZS 682.1B [USD 0.3B], a 19.4% growth in net interest income fr the previous year, compared to CRDB which returned TZS 632.9B [USD 0.27B], an 11.2% increase.

Sitting on cash: The two Tanzanian banks are cumulatively sitting on TZS 800B [USD 0.35B] cash at hand as at Dec 2021.

NMB was more profitable: NMB posted 37.2% growth from the previous year to TZS 288.6B [USD 0.13B] in profit after tax while CRDB returned TZS 267.6B [USD 0.12B], 62% growth.

Other Tanzania banking sector Q4 2021 earnings reports were:

⚠️ More 2022 Profit Warnings

Liberty Kenya joins list: The insurer is the latest to issue a profit warning citing higher risk claims in 2021 occasioned by the impact of COVID-19. Kakuzi, Limuru Tea, and Sanlam Kenya are the other listed firms to have issued profit warnings this month.

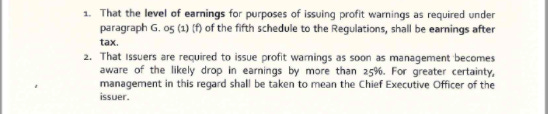

CMA speaks: In a circular to listed firms, the watchdog clarified that the likelihood of a more than 25% drop in earnings after tax shall be the level used for purposes of issuing profit warnings. Chief Executive Officers of listed firms shall be responsible for complying with the profit warning publications.

In 2021, KenGen failed to issue a profit warning even with its earnings for the FY ended 30 June 2021 dropping by 93.5%. The listed power producer cited a 7% rise in profit before tax and higher taxation that in its view did not necessitate issuing a profit warning.

📅 Feb 2022 Treasury Bond Sale

The Central Bank of Kenya (CBK) has announced the issue of a new 19-year, amortised infrastructure (tax-free) bond in the month of Feb 2022, with a stated target of raising KES 75B [Central Bank of Kenya].

Notes on the IFB from Sunil Sanger: The last infrastructure bond issue in Sept 2021 attracted a record subscription of KES 151B, of which the CBK accepted KES 106B. The current issue will most likely attract a good response from the market. The coupon rate on the bond will be market determined (based on the average rate of competitive bids accepted by CBK). The average yield on the bond is likely to be in the range of 12.25% - 12.50%. Investors have the option to submit “non-competitive” bids for amounts up to KES 20m. Investors submitting valid non-competitive bids are assured allotment in the auction at the average rate determined in the auction.

🗞 What Else Happened This Week?

📕 January MPC meeting: The Monetary Policy Committee of the Central Bank of Kenya met this week and retained the Central Bank Rate (CBR) unchanged at 7%. Find the press release and our highlights of the press briefing here.

🏦 KCB Bank: The Kenyan lender is scouting for new acquisition opportunities in the Tanzanian market after dropping its bid to acquire BancABC of Tanzania [Business Daily].

“We are always looking for opportunities. So in Tanzania definitely. We had a final conversation with BancABC in December. Our focus largely today is on other countries. Tanzania is something we will come back to perhaps in the second half of this year” - CEO Joshua Oigara

The bank’s Tanzanian subsidiary has performed quite well across board as per the Q4 2021 results released this week:

Total assets: Up to TZS 836.2B vs TZS 822.3B in Q3 2021

Deposits: Up to TZS 555.7B from TZS 537.5B in Q3 2021

Net interest income: Up to TZS 48.5B y/y from TZS 43.5B

Net income after tax: Up to TZS 15.6B y/y vs TZS 4.6B

NPLs: Down to 2.7% from 3.04% in Q3 2021

💡 “Exciting” opportunity at KPLC: The troubled utility firm is seeking to fill the position of Managing Director. Eng. Rosemary Oduor was appointed Acting Managing Director in August 2021 following the resignation of Mr Benard Ngugi [Mwango Capital].

Source: Simply Wall Street

📉 Car & General: The run seems to be over as the counter was this week’s worst performer. The share price was down 21.17% having hit highs of +31% in mid-January [Mwango Capital].

Source: Simply Wall Street

🌍 African Markets this Week

In Kenya, Kenya recorded a 2.20% decrease in the Nairobi Securities Exchange All Share Index, closing the week at 161.04, down from last week’s 164.66.

Across East Africa: Tanzania’s DSE ASI was up 1.36% to close at 1,922.69 up from last week’s 1,896.84, while Uganda’s USE ASI recorded a 0.68% decrease to close at 1,368.43 down from last week’s 1,377.77.

Across Africa: Zimbabwe’s ZSE ASI recorded the highest increase in returns this week, up 7.03% to close at 12,120.10.

📊 Chart of the Week

Top 20 firms in Africa by Market Cap (excluding JSE)

If you enjoyed our newsletter, share it with friends: