IMF To The Rescue!

IMF reaches a staff-level agreement with Kenyan authorities

👋 Welcome to The Mwango Weekly by Mwango Capital, a newsletter that brings you a succinct summary of key capital markets and business news items from East Africa.This week, we cover IMF-Kenya staff level agreement and more Q1 2023 Kenyan Banks' earnings.First off, enjoy a dose of our weekly business news in memes.

IMF To The Rescue!

Fifth Reviews: The IMF this week announced that it has reached a staff-level agreement with Kenyan authorities on economic policies to conclude the Fifth review of Kenya’s Extended Fund Facility (EFF) and Extended Credit Facility (ECF) arrangements. Further, under consideration was also Kenya’s request for access under the IMF’s Resilience and Sustainability Facility (RSF) to bolster the EFF/ECF arrangements.

Financing: In July, the IMF management and Executive Board are set to consider and approve the agreement, upon whose completion would see Kenya have immediate access to SDR 306.7M/US $410M, to bring the gross IMF Support under the EFF and ECF arrangements to SDR1.509B/US $2.017B. On a consolidated basis, the EFF, ECF arrangements and the RSF support will bring the total commitment under these arrangements to SDR2.633B [US $3.52B].

“The agreement is subject to IMF management approval and consideration by the Executive Board, which are expected in July. Upon completion of the fifth reviews by the IMF Executive Board, Kenya would have immediate access to SDR 306.7 million (about US$410 million), including from the augmentation of access under the ECF/EFF.”

“I think therefore we have found ourselves in a situation where we are having to pay KES 900 billion per annum just to pay the interest, and we’ve hit a brick wall, essentially, we’ve not hit it today but we're gonna hit it at some point and not in the distant future. What I think this administration has done, which is interesting, is its political pivot away from China and back towards the West. If you just look, there was one week, if I’m not mistaken, when the head of the IMF was in town, when Olaf Scholz was in town, and you had a whole string of people. So, I think politically speaking that was a sensible decision in the context of the fact China is trying to rein in its African loan book, its not giving new money and we are leaning more on IMF, World Bank multilateral support and hopefully more support from the West, and I think in the context of particularly the Ukraine war, you compare comments and responses in South Africa for example, we have taken a more conciliatory approach to the G7 line on that war, and I think when you take all of that from geo economically, geopolitically, speaking; Kenya is reasonably well positioned to get support. Now the question is, how much support do we require and if you take the bullet payment coming up next year June, $2B, unless there is some kind of quasi-guarantee from the IMF or the World Bank, I think it's going to be very difficult for us to raise that money. I estimate that we need $6 - $7B between now and that bullet repayment. From what I can see, I feel there is about half of that which has been promised if you look at the recent IMF programme, if you look at what the World Bank is proposing, you factor in bilateral support out of Europe and maybe the US, but there is still a shortfall.”

Financial Markets Analyst, Aly-Khan Satchu

Ghana, as like Kenya, they do need a lot of money, I think $6B is a reasonable figure. I think part of that’s already been raised or promised is in the pipeline from the World Bank, the IMF. “The IMF there was around $1B additional funds just announced, which was earlier this week, and could be a little bit more coming. You have the World Bank money coming, but I think there is more needed. My interpretation is there is a bit, because Ruto has been seen as more switching from China back to the West, but I would not be surprised if he would be flying out to Beijing within the next months. The question is what would be the price for that. I think there is potential for renewed financing but I know China is in general cutting back exposure to frontier markets including African markets but they are preparing to put more money into Tanzania, Uganda. My interpretation is they are more bullish on East Africa, more keen on remaining engaged in East Africa and other regions of Africa. So I think, would this money be coming in, I would doubt whether there will be large amounts of bilateral funds coming from Europe. We will see. My concern is less with Kenya and itself, I think they could remain on track for the fiscal consolidation and I think that the funds will be there, but what would be the market reaction around Kenya if there was a default in Egypt or in Pakistan which I think it’s a high likelihood next year. So I mean my core scenario remains that even if there is more multilateral funding, possibly also some bilateral that will relieve in some form or the other, that you will need a policy-based guarantee or multilateral guarantee to refinance the 2024 Eurobond and there is not much talk of guarantee. I mean AfDB guaranteed part of the Egyptian Panda Bond issue and also a guarantee for Benin and I think something similar would come for Kenya. It's just a question of what size it is. I think a partial guarantee is quite likely and it is just a question of what will be sufficient for Kenya to issue at reasonable rates. I think it is mostly a solvency issue in Kenya. The 5% of GDP interest cost of the government is among the highest in Africa.”

REDD Intelligence Senior Analyst, Mark Bohlund

“At least for Kenya, prior to the current program, we had a precautionary facility, like an insurance cover. In 2020 when COVID came we had Rapid Financing where most of the countries tapped into the IMF lending because of what happened during COVID. And after that we had 2021 we entered into the current program, the 38 -month program. But I think it is been morphing, by the time, because by the time we were entering into this program the amount that we were to receive in terms of the Special Drawing Rights was close to $1.66B which was equivalent to $2.3M, but again, remember these disbursements are done after every 6 or so months after a review has been finalized, so I suspect because of the SDR-Dollar rate has moved higher from the time we entered into this program, and also the fact that the Kenya Shilling-Dollar rate has trended to where it is, then in Kenya Shillings terms, the amount of money we will receive will be higher than what was envisaged in the start of the program. The other thing is that with the Fourth Review which was concluded in December, there was what was called an augmentation, so basically because of the fact that some of the measures that had been put in place, things like the fiscal consolidation, issues around monetary policy, issues around State Owned Entities, at least there was a semblance of some progress, so that sort of necessitated the augmentation which we received with the Fourth Review which will be included in the remainder of the program and the other thing touches on the RSF, the Resilience and Sustainability Facility (RSF).”

IC Asset Managers Economist, Churchill Ogutu

Focus Areas: The IMF has pointed out some observations about the country’s fiscal and economic affairs and below are some key takeaways.

SOE Reform: The IMF has highlighted that it would be important for the country to explore reforms around the country’s State-Owned Enterprises (SOEs) including Kenya Airways and Kenya Power and Lighting Company to stop the drain on budget resources accruing from the support to these SOEs.

Government Spending: The Fund has highlighted the prudence in spending in the current FY 2023/2024, underscoring the consistency of spending with available resources in the fiscal year. Parliament is currently targeting to reduce the fiscal deficit to 4.1% of GDP from 5.7%.

Interbank FX Market: The IMF has lauded Kenya’s move to revive the interbank market for foreign exchange. The Kenyan Shilling has been on a depreciating trend in the year and has lost 12% of its value so far. This is greater than the losses recorded in 2022, which stood at 9%.

“The functioning of the foreign exchange is gradually improving. Further actions to bring back liquidity to the interbank market for foreign exchange and support exchange rate flexibility is instrumental to secure effective market functioning and backstop the external position.”

Across the Region: The IMF Executive Board this week completed the first reviews of Rwanda’s Coordination Instrument and Program under the Resilience and Sustainability Facility, allowing for an immediate disbursement of SDR 73.95M ($98.6M). Rwanda becomes the first country to receive financing under the RSF, and Churchill Ogutu shared a few highlights on the RSF on #MwangoSpaces.

“So let me take you back to around August 2021, whereby the IMF now had to allocate some additional SDR to all the countries but now depending on their quota on an IMF basis. So some of the developed world had outsized allocation in SDR which they did not need. So last year, the IMF came up with this particular Fund, the RSF, at least to ensure that those developed countries that do not need this additional SDR, as a way to now more, less distribute it to the low-income countries. That is where the RSF is coming in. I think so far 15 countries have wired some funds to particular countries. As at last month, 5 countries had already tapped into the RSF program. Rwanda next door I think is the first country to tap into that RSF Fund. Kenya also, based on the review, is also entitled to some additional funding. So, potentially, the (Kenya’s) program, at the point of initiation, which was around $2.3B, is shooting up to close to even over $3.5B if you factor in the RSF.”

IC Asset Managers Economist, Churchill Ogutu

You can find a link to the entire press release to the IMF-Kenya Staff-Level Agreement here and Rwanda’s here.

Below is a link to the Twitter Space we had in the week on the IMF deals in Ghana and Kenya:

#MwangoSpaces: The IMF Deals in Ghana and Kenya

Kenyan Banks Q1 2023 Results

Both NCBA Group and KCB Group released their Q1 2023 results this week. Below are our key takeaways:

Loan Book: Across the banks that have reported so far, KCB Group had the largest year-on-year change in aggregate lending, with the loan book expanding by 31.7% to KES 928.8B, accounting for 57% of the asset base[2022: 60%]. Equity Group registered a 21% growth in loans to KES 756.3B, or 49% of the asset base, unchanged from 2022. Cooperative Bank had the sector’s third largest loan book at KES 360B, representing 57.1% of gross assets, up from 54.4% in 2022.

NCBA’s loan book was up 17.7% to KES 287.2B, or 45.7% of the balance sheet [2022: 41.5%]. For StanChart, loans grew by 7% to KES 137B, accounting for 35.3% of the asset base, down from 37.6% in 2022.

Government Securities: KCB Group held an aggregate pile totalling KES 252.1B in government securities in the operating period, up marginally by 0.4%, representing 15.5% of the balance sheet [2022: 21.5%]. NCBA had KES 207.1B in government securities, up 6.4% to account for 33% of the balance sheet, unchanged from 2022. For StanChart, KES 95B had been deployed in government securities, down 6.21% to represent 24.5% of the asset base, a 5-year low. Cooperative Bank’s pile of government securities fell by 2.3% to KES 179B while Equity Group’s fell by 7.7% to KES 216B, to account for 25.5% of its gross assets.

Asset Base: KCB Group posted an increase of 40% in its asset base to KES 1.63T to be the largest lender by asset size, eclipsing Equity Group, whose balance sheet edged higher by 21.1% to total KES 1.54T. Cooperative’s balance sheet stood at KES 631.1B, an expansion of 5.7% to KES 631.1B, while that of NCBA was KES 628.8B, a growth of 7.1%. StanChart had an asset base of KES 388B, representing a growth of 14% from 2022.

Interest Income Mapping: Equity Group posted the largest growth in Net Interest Income at 12.1% to KES 21.7B, while Non-Interest Income edged higher by 54.3% to KES 18.4B, bringing the NII and NFI contribution mix to Gross Operating Income to 54:46. KCB’s NII was up 11.8% to KES 22.1B, while its NFI edged higher by 59.2% to KES 14.8B to contribute 40% to operating income. Cooperative’s NII rose by 4% to KES 10.8B, to account for 60.2% of total operating revenue, while its NFI was up by 10.8% to KES 7.1B. For NCBA, the NII expanded by 18% to KES 8.4B, while the NFI rose by 18.5% to KES 7.2B, accounting for 46.2% of operating income. StanChart reported KES 6.9B in NII, an increase of 40.2%, and KES 3.9B in NFI, up 55.5%, bringing the contribution to operating revenue to 64:36.

Loan Loss Provisions: KCB’s provisions through the income statement were up by a whopping 98.4% to reach KES 4.1B - the largest in absolute terms across banks that have reported so far. Equity’s provisions stood at KES 3.5B, up by 92.5% accounting for 15% of gross operating expenses [2022: 11.3%]. Cooperative had an aggregate of KES 1.5B in provisioning, down marginally by 0.7%, while for NCBA, the provisions edged lower by 22.6% to reach KES 1.95B, the lowest reported since the merger. StanChart reported KES 790.9M in provisions in the operating period [2022: KES -86M]. Here is what KCB Group CFO had to say about the jump in provisions in the operating period:

“So it's actually two main things. One, there is the impact of FX. With the depreciation of the shilling, we’ve had to take additional provisions just purely because you are translating a dollar facility that was 100 in December and has gone to 120 in Q1. And the corresponding collateral has not increased by that much, so we haven’t done valuations of collaterals. Some are likely to improve but others not as much so just the gap created by the depreciation of the shilling necessitated additional provisioning. That’s one. And then the second one is largely driven by the Kenya business, what we call scheme loans. You have read about all these funding issues for universities. We have a lot of universities on our book and because they are not receiving funding from the government, then we’ve seen that as an increase in risk rating. So, the staging from an IFRS standpoint has moved from either 1 to 2 or 2 to 3, which necessitates additional provisioning.”

KCB Group CFO, Lawrence Kimathi

KCB NPLs in Focus: In the operating period, gross Non-Performing Loans (NPLs) increased by 98% to reach KES 176.7B, equivalent to 19% of the loan book [2022: 18.59%]. NPLs were concentrated in the manufacturing sector, which accounted for 23.1% of gross NPLs against a contribution of 12.6% to the loan book. The decomposition of NPL ratios across subsidiaries puts NBK as the leading at 23.2%, followed by KCB Bank Kenya at 19.7% and TMB - the DRC unit, at 13.3%. Segment-wise, corporate had the highest NPL ratio at 33.5%, Mortgage at 19.7%, SME & Micro at 9.6% and Checkoff at 3%.

“We’ve got various strategies, rehabilitation, recovery, write-off, that we’re pursuing. Q1 we’ve had a mix of winning in those strategies but also because of the macro environment, we’ve had some facilities that were doing okay, were performing, that have tipped to non-performing purely because of the general macro environment, so it's about getting that balance right, making sure you don’t have items slipping over as you’re implementing your strategy on NPL recovery. We’ve got 4 or 5 big ones that are government-related. We have made some significant strides in getting them sorted out. We are just, I would say, the tail-end of getting those facilities getting restructured and getting back to performing, and those are sizable. We execute on those, and we should be very good on the way.”

KCB Group CFO, Lawrence Kimathi

Profitability: Albeit recording the largest absolute Profit Before Tax (PBT) at KES 16.9B, Equity Group recorded a paltry 10.5% increase, the lowest in three years [2022: 30.57%, 2021:67.13%, 2020: -20.7%]. KCB’s PBT was down 1.3% to KES 13.9B, compared to a growth of 54% recorded in 2022. Cooperative had a PBT of KES 8.1B in the period, a growth of 5.1%, while NCBA’s PBT rose the most by 31.9% to KES 5.1B, almost double the KES 2.8B reported in 2021. StanChart’s PBT was KES 5.6B, up 58.8% - the highest change across listed banks that have reported so far.

New KCB Board Chair: The Board of Directors of KCB Group has elected Dr. Joseph Kinuya - the immediate former head of Kenya’s Public Service as the new Chairman following the retirement of Mr. Andrew Kairu from the helm of the board after 5 years of service. Separately, the CEO Paul Russo marked a year in office since his appointment.

KBA Pushes for Unchanged CBR: Ahead of the CBK Monetary Policy Committee meeting slated for 29th May 2023 - the last for CBK Governor Dr. Patrick Njoroge; the Kenya Bankers Association (KBA) has released a Research Note in which it wants the MPC to keep the Central Bank Rate (CBR) unchanged. In its proposal, the KBA has cited easing inflation pressures, fragility in leading indicators in 2023, decelerating growth in private sector credit and external pressures in the current account.

“In view of the above developments, and the balance of risks on inflationary pressures and economic growth preservation, we argue that the sustenance of the current monetary policy stance - in keeping the CBR unchanged at 9.50% - would be appropriate.”

Across the Region: Tanzania’s Central Bank, the Bank of Tanzania, has transferred all the assets and liabilities of Yetu Microfinance Bank to NMB Bank - Tanzania’s second-largest bank by assets. This comes after Yetu was placed under administration effective 12th December 2022.

Here are links to the full results by Equity Group Holdings, Standard Chartered Bank Kenya, Co-operative Bank of Kenya, NCBA Group, and KCB Group.

We also had an interview with the KCB Group CFO which you can access below:

Episode 53: KCB Q1 2023 Results

Markets Wrap

The NSE: In Week 21 of 2023, Eveready PLC was the top-performing stock on the Nairobi Securities Exchange, unchanged from last week, appreciating by 44.4% to KES 1.56, while Stanbic Holdings was the worst-performing stock, falling 10.7% to KES 98.25. The NSE 20 index rose by 1.4% to 1,488.2 points while the NSE 25 index fell by 1.2% to 2,540.1 points. The NSE All Share Index (NASI) was down by 0.6% to 97.9 points, closing the third consecutive week below 100 points. Equity turnover was down 14.3% to KES 1.4B while bonds turnover fell by 21.4% to KES 14.B.

Treasury Bills: In the short-term public debt markets, the weighted average interest rate of accepted bids for the 91-day, 182-day, and 364-day treasury bills were 10.832%, 11.113%, and 11.457% respectively. The total amount on offer was KES 24B with the CBK accepting KES 21B of the KES 22B bids received, to bring the aggregate performance rate to 91.87%. The 91-day and 364-day instruments recorded 356.06% and 37.64% performance rates, respectively.

Treasury Bonds: The second tap sale of FXD1/2023/03 recorded a performance rate of 135% attracting bids worth KES 27.2B against KES 20.0B sought, with the Central Bank of Kenya accepting KES 27.2B.

Eurobonds: Last week, the yields were mixed on a week-on-week basis across the 6 outstanding papers.

KENINT 2024 yield was the only one that rose in the week, appreciating by 128.3 basis points to 15.632%. The other yields all fell, with KENINT 2027 and KENINT 2034 falling by 8.5 bps to 11.749% and 11.0225, respectively.

All yields were up on a Year-To-Date (YTD) basis. KENINT 2024 led the gains at 302.9%, while KENINT 2048 appreciated the least, by 81 bps to 11.634%.

KENINT 2034 and KENINT 2048 led price gains week-on-week, rising by 0.6% in both cases to 70.810 and 72.658, respectively, while KENINT 2024 led price losses at 1.1% to 91.676 On a YTD basis, prices on all yields fell, with KENINT 2034 leading price losses at 8.6% while KENINT 2024 recorded the least losses at 0.9%.

Market Gleanings

💰 | Naivas’ KES 2B Profit in 9 Months | IBL Group last year acquired a 26.3% stake in Naivas (as part of a consortium that owns 40% of Naivas) IBL's share of income of Naivas for the 9 months ended 31st March is Mauritian Rupees 184M (KES 557M). Total profits for Naivas are estimated to be around KES 2.12 Billion for those 9 months.

⚡ | Revenues Up, Profits Down| Kenya Power's revenue increased by 1.3B in April, partly driven by the recent hike in power tariffs. The new tariffs were gazetted with the implementation starting on the 1st of April. Kenya Power's revenues in FY 2021/22 were KES 157.35B and are expected to rise to KES 177B boosted by recently authorized tariffs against an initial target of KES 195B in the firm's initial submission to EPRA. Separately, Kenya Power is set to spend KES 10B in the fiscal year starting July 2023 to construct new substations, power lines and to strengthen the electricity distribution network which currently covers 300K KM. The utility has also issued a profit warning, expecting its net earnings for the fiscal year ending June 2023 to be lower than the previous year by more than 25%.

📉| Car and General Net Profit Dips | In the first six months to March 2023, revenues increased by 5.4% to reach KES 10.6B, and the Gross Profit came in at KES 1.5B, down 3% to bring the Gross Margin to 13.8% [2022: 15%]. The net profit for the year fell by a whopping 85% to KES 96.7M on an 18% drop in sales at Kenya trading operations, high FX losses totalling KES 155M due to the continued devaluation of the Kenya Shilling and Q1 demurrage costs in Tanzania totalling KES 123M.

💵| Ethiopia’s Privatization Drive | The Ethiopian government has announced the issuance of a Request For proposal (RFP) for the privatisation of eight state-owned sugar enterprises which are Arjo, Dedessa, Kessem, Omo Kuraz 1, Omo Kuraz 2, Omo Kuraz 3, Omo Kuraz 5, Tana Beles and Tendaho. Separately, Ethiopia will launch a tender for a second international telecoms licence next month, whose fruition will see the country have a third mobile operator after Safaricom and the state monopoly Ethio Telecom.

📈 | Nation Media’s Share BuyBack | Nation Media Group has announced a share buyback scheme targeting up to 10% of its issued shares barely 14 months after the first share repurchase scheme. The 2021 share buyback programme to purchase 10% [20.7M] of its issued share capital ran between June and September 2021 and realised an uptake of 82.5% [17.1M] shares. Centum is running its 18-month share buyback programme, which started in February, targeting to buy back at least 66.5M shares.

👨💼 | Tinubu’s Inauguration | Bola Tinubu, the winner of Nigeria’s Presidential Election, is set to be inaugurated today as Nigeria’s new President. Tinubu was declared President in the elections held earlier in February this year, garnering 8.8M votes, or 35% of the total votes cast. Separately, Nigerian lawmakers raised the legal limit on government borrowing from the Central Bank in an emergency Senate sitting, weeks after Parliament approved outgoing President Muhammadu Buhari’s request to convert loans totalling $22.7T Naira/$49B owed to the Central Bank into a 40-year bond that pays a 9% interest rate.

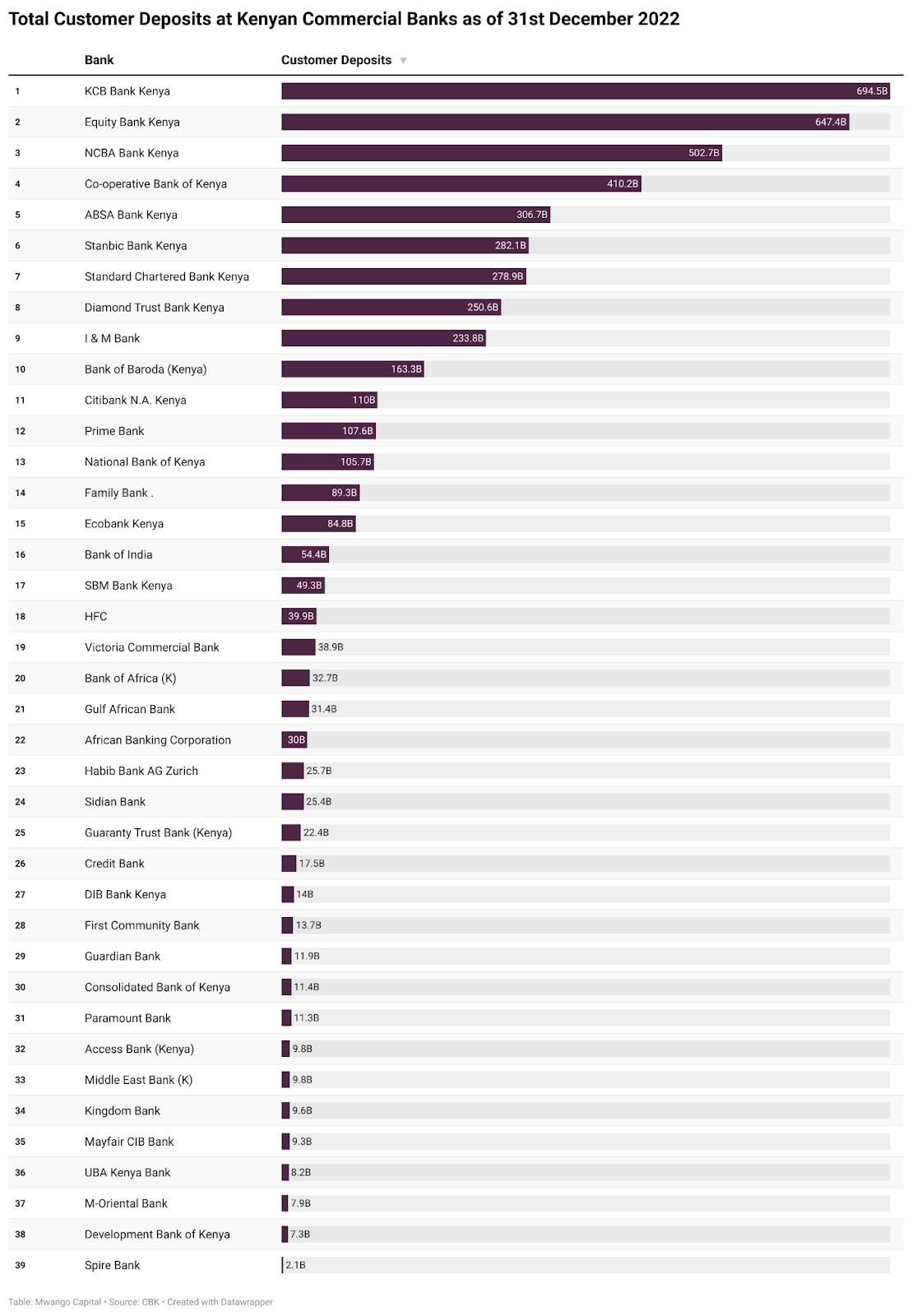

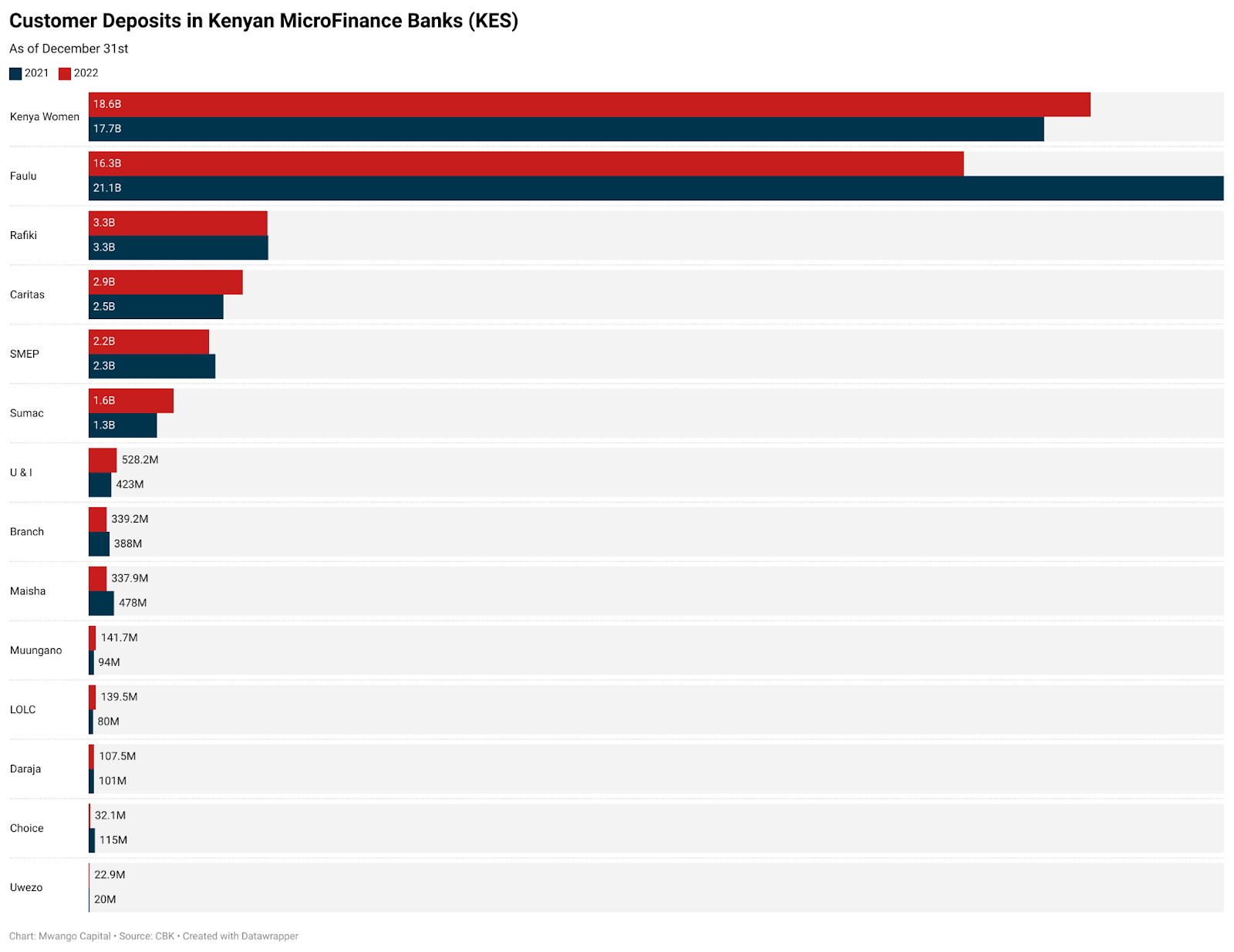

Charts of the Week